Copper closed 2025 with a 44% gain that few forecasters predicted and even fewer can fully explain. The metal now trades above $12,900 per tonne on the London Metal Exchange, pressing toward levels that the most aggressive sell-side targets only envisioned for late-decade scenarios. The rally has split the analytical community into two camps that talk past each other: structural bulls who see a decade of electrification-driven deficits, and sceptics who point to $30 billion in speculative inflows that have disconnected price from near-term physical reality.

This analysis attempts something different. Rather than declaring a verdict, we decompose the rally into its component parts - separating what is real from what is borrowed from future demand, quantifying the speculative premium, and identifying the catalyst that could snap the tension in either direction. The distinction matters because copper, at these levels, is simultaneously the most important industrial bet of the decade and one of the most crowded trades in commodities.

The Rally in Numbers: What $12,900 Actually Means

Context matters when prices breach multi-decade ceilings. Copper's current level represents a genuine purchasing-power increase, not just monetary inflation. When adjusted for CPI, the January 2026 price exceeds both the 2008 financial-crisis peak and the 2011 QE-era high - a distinction that previous rallies could not claim.

| Price Milestone | Nominal (US$/t) | Inflation-Adj (2026 $) | Market Context |

|---|---|---|---|

| 2008 Peak | $8,985 | $12,850 | Financial Crisis / China boom |

| 2011 Peak | $10,190 | $13,420 | QE Era / commodity supercycle |

| 2021 High | $10,747 | $12,180 | Post-COVID recovery |

| Jan 2026 | $12,900 | $12,900 | Electrification + supply crisis |

The S&P Global study published earlier this month frames the longer arc: global copper demand is projected to increase by 50% by 2040, reaching 42 million metric tonnes. Without new mines or technological breakthroughs, production peaks around 2030, leaving the world short roughly 10 million tonnes by 2040. As Carlos Pascual, Senior Vice President at S&P Global Energy, put it: "Copper is the connective artery linking physical machinery, digital intelligence, mobility, infrastructure, communication and security systems."

Several countries have now designated copper a "critical metal" - including the United States in 2025 - a policy signal that historically precedes stockpiling behaviour and export restrictions. The question is not whether long-term demand exists. The question is whether today's price already discounts years of that demand. Answering it requires pulling the rally apart at the seams.

Decomposing the Rally: Fundamental vs. Speculative

Market analysis from GEM Mining Consulting and corroborated by multiple independent assessments suggests that approximately 50–70% of recent price appreciation stems from structural supply-demand factors, while the remainder reflects financial positioning, currency effects, and speculative momentum. This composition matters enormously for durability: a rally anchored primarily in fundamentals corrects less violently than one built on leverage.

The speculative component, while the minority, is what makes this rally vulnerable. Trading activity in Chinese metals markets has surged to record levels, with investors piling into futures contracts. Prices have advanced even as inventories increased - a divergence that typically signals narrative-driven buying rather than physical tightness. Globally, expectations of easier monetary policy and a softer dollar have attracted capital into commodities as a broad asset class. Trend-following strategies and reflation-oriented positioning have created feedback loops where rising prices invite additional inflows.

History warns clearly about what happens when positioning becomes crowded. In 2011, copper peaked at $4.60/lb with similarly extreme positioning, then declined 35% over nine months as China growth slowed and speculators unwound. The current setup shares several characteristics with that episode. Goldman Sachs has quantified this risk more precisely than most - and their reasoning deserves careful examination before any long-term structural case can be evaluated with clear eyes.

The Goldman Correction Thesis

Goldman Sachs has emerged as the most prominent voice cautioning against near-term complacency. Their analysts argue that near-term fundamentals do not yet justify the magnitude of the rally, noting that global supply remains sufficient to meet current demand - even if it cannot meet projected future demand.

Goldman's base case calls for a correction from approximately $13,000 to $11,000 per tonne - an 18% decline - as roughly $30 billion in speculative capital exits copper futures. The thesis rests on three pillars: the market currently sits in an estimated surplus of 300,000 tonnes when adjusted for off-exchange stocks; EV copper intensity is declining as manufacturers optimise battery architectures; and Chinese demand growth is moderating as the property sector remains structurally impaired.

- Goldman Sachs Commodities ResearchThis caution does not undermine copper's longer-term structural appeal. What it highlights is the distinction between investing in a commodity because the decade ahead demands more of it, and trading a commodity because momentum has been rewarding longs. The former can tolerate a 15–20% drawdown; the latter cannot.

The Goldman view also introduces a crucial nuance often lost in the bull-case narrative: surplus versus deficit depends entirely on the time horizon. Near-term (2026), the market may print a modest surplus as new mine capacity ramps. Medium-term (2028–2030), deficits become increasingly likely. Long-term (2030–2040), the S&P shortfall of 10 million tonnes per year looks genuinely alarming. Price should reflect a blend of these horizons - but at $12,900, it appears to be pricing primarily the long-term scenario. The raw warehouse data makes this time-horizon problem concrete.

The Inventory Paradox: Reading the Warehouse Data

Exchange-visible copper inventories represent only 60–70% of total available stocks, with the rest hidden in private warehouses, bonded storage facilities, and government strategic reserves. This opacity creates information asymmetry that amplifies price moves - participants cannot confidently assess true supply adequacy, so they buy defensively.

LME (London)

SHFE (Shanghai)

COMEX (New York)

Total exchange inventories of 255,000 tonnes translate to roughly 11–16 days of global consumption - approaching the historical lows experienced during previous supply-constrained periods. When inventories fall below 20 days, markets typically experience elevated price volatility and heightened sensitivity to disruptions.

The geographic concentration is equally telling: low inventories outside the United States mean that production disruptions in South America or processing delays in Asia trigger disproportionate price movements. Chinese off-exchange inventories may exceed 500,000 tonnes, but official data remains unavailable for verification, and Beijing's strategic-reserve accumulation strategy adds another layer of opacity.

This is the inventory paradox in action: visible stocks look tight enough to justify elevated prices, but hidden stocks may be sufficient to cushion a speculative correction. The uncertainty itself becomes a price driver, as both bulls and bears can construct plausible narratives from incomplete data. What neither side can dispute is the supply-side arithmetic that underpins the structural case regardless of how the inventory question resolves.

The Investment Gap That Won't Close

Whatever one thinks about near-term speculation, the supply-side mathematics are unforgiving. Major mining companies allocated approximately $15 billion globally to copper project development in 2025 - well below the estimated $25–30 billion annually required to maintain current production levels as existing mines deplete. The gap is not closing.

Annual Copper Capex: Actual vs. Required to Maintain Output

Average copper ore grades have declined from approximately 1.6% in 1990 to below 0.8% currently, effectively doubling the mining intensity required per unit of refined copper production. This is not a problem that can be solved by higher prices alone - it requires new discoveries, new mines, and new processing capacity, all of which operate on timelines measured in decades, not quarters.

| Development Stage | Timeline | Capital (US$B) | Success Rate |

|---|---|---|---|

| Exploration to Resource | 5–8 years | $0.1–0.5 | 15% |

| Feasibility to Permitting | 3–5 years | $0.5–1.0 | 60% |

| Construction to Production | 4–7 years | $2.0–8.0 | 85% |

| Total: Discovery to Production | 12–20 years | $2.6–9.5 | ~8% |

An overall success rate of roughly 8% from discovery to production, spanning 12–20 years, explains why high copper prices alone cannot rapidly bring on new supply. Environmental regulatory frameworks have extended permitting timelines by 2–4 years compared to historical averages. The supply response to price signals in copper is measured not in months, like oil, or in seasons, like agriculture, but in decades. This is the structural argument that underpins the bull case even through a potential correction. But supply constraints only justify elevated prices if the demand projections that depend on them are themselves credible - and that claim warrants its own honest scrutiny.

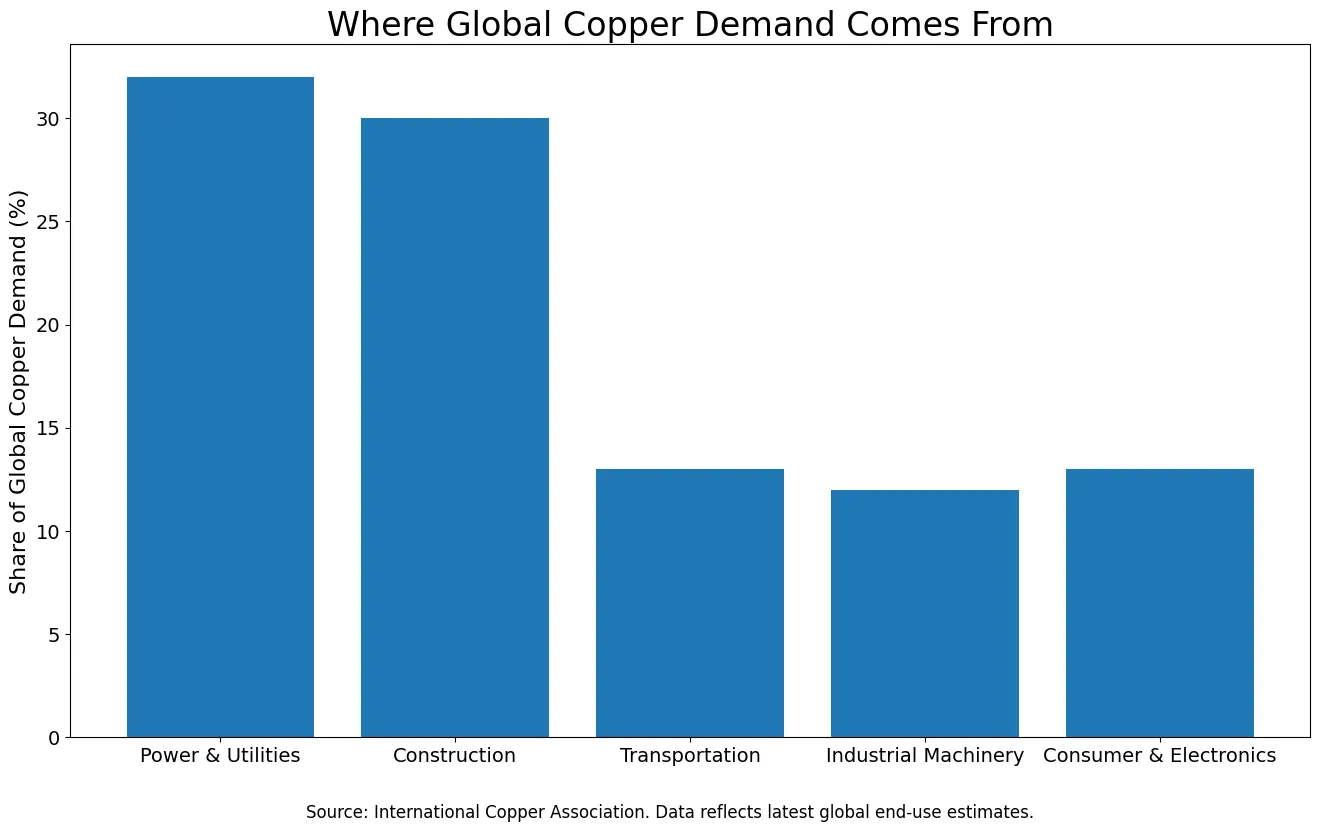

The Demand Thesis: Where It Holds and Where It Stretches

The bullish demand narrative rests on four pillars. Each has genuine substance, but each also faces nuances that the most enthusiastic forecasts tend to gloss over. Understanding where the demand case is airtight versus where it is aspirational is critical for assessing whether $12,900 is justified or borrowed from a future that may arrive more slowly.

EVs & Charging

80–100 kg per battery EV vs. 20–25 kg for ICE. With 14M annual EV sales, that's 1,100–1,400 kt of demand. But copper intensity is declining as manufacturers optimise.

Renewables & Grid

Wind: 3–4 t/MW. Solar: 4–5 t/MW including transmission. Grid modernisation increases copper intensity 40–60% vs. legacy infrastructure.

Data Centres & AI

200–300 kg per server rack for power distribution and cooling. Hyperscale buildout is the emerging demand category traditional models underestimate.

Defence & Strategic

Nations designating copper "critical" drives precautionary accumulation. "Governments are afraid that without enough copper, their economies won't remain competitive," says José Torres, Interactive Brokers.

S&P Global's forecast of 42 million metric tonnes by 2040 - a 50% increase from current levels - leans heavily on all four pillars delivering simultaneously. If EV adoption follows the more moderate trajectory that Goldman expects (with declining copper intensity per vehicle), or if grid modernisation timelines slip due to permitting and NIMBYism, the deficit arrives later and shallower than advertised. The demand is real, but the pace is debatable.

"A significant part of the incremental demand is tied to electrification, grid build, data centres/AI and defence, where copper's conductivity and reliability makes substitution harder in critical applications."

- Rita Adiani, CEO, Titan Mining CorporationThe structural demand case is genuine and, on a decade-long view, compelling. But "genuine" and "correctly priced" are not the same thing. At $12,900 per tonne, the market is not waiting patiently for long-term deficits to arrive - it has already front-run them, financed partly by speculative positioning that deserves its own accounting.

When Euphoria Meets Gravity

The speculative dynamics deserve close attention because they determine the trajectory of the next 6–12 months, even if the structural story defines the next decade. Several warning signs have emerged:

Chinese futures volumes at records. Trading activity in Shanghai copper futures surged to levels that market veterans describe as detached from physical delivery intentions. Open interest has climbed even as inventories on the SHFE remained stable - a pattern consistent with financial speculation rather than hedging by industrial users.

Price advancing despite rising inventories. This is perhaps the most telling divergence. In a fundamentally driven market, rising inventories should moderate prices. The fact that copper prices have continued climbing while exchange-visible stocks increased suggests that macro narratives (Fed cuts, dollar weakness, China stimulus hopes) are doing more work than physical tightness.

The $30 billion overhang. Goldman estimates that approximately $30 billion in speculative capital has entered copper markets above equilibrium levels. When positioning is this crowded, the exit door becomes narrow. Any catalyst that challenges the narrative - a stronger dollar, disappointing China data, a major mine restart - could trigger cascading selling as trend-followers rush to cut losses.

The projected supply deficit for 2026 sits at 150,000–330,000 tonnes, representing approximately 0.8–1.5% of global consumption. While genuine, this deficit is modest enough that a shift in macro sentiment, a resolution at suspended operations, or an uptick in scrap recycling could quickly narrow it. The risk is asymmetric at current prices: the downside from speculative unwinding (15–20%) exceeds the upside from deficit widening (5–10%) in most probability-weighted scenarios.

- PolyMarkets Investment, Research DeskWith the warning signs identified, the question becomes how to assign probabilities to the outcomes they signal. Scenario analysis imposes discipline on that process - forcing explicit assumptions about which forces resolve first and in which direction.

Three Scenarios for the Next Twelve Months

Rather than declare a single price target, we map the probability-weighted paths that copper may follow as the tension between structural demand and speculative positioning resolves.

Bear Case - 25%

Speculative unwind meets China disappointment. $30B in positioning exits rapidly. Dollar strengthens on delayed Fed cuts. Global manufacturing PMIs deteriorate. 20–25% correction over 4–8 months, echoing 2011.

Base Case - 55%

Orderly repricing as speculative froth bleeds off. Physical demand growth of 2–3% provides a floor. Goldman's $11,000 target reached over 3–6 months. Volatility elevated but not disorderly.

Bull Case - 20%

Major supply disruption or China mega-stimulus. Fresh record above $14,500 as short covering compounds momentum. Deficit widening beyond 330,000 tonnes. Structural repricing validated.

The probability weighting assigns an 80% chance of prices being lower 6 months from now than the current $12,900 level. This does not mean the long-term bull case is wrong - it means that markets have a tendency to front-run fundamentals, pricing in years of demand growth in months, then correcting as reality catches up with narrative. The distinction between a good investment and a good entry point is everything in commodities. The junior mining project pipeline offers a useful ground-truth check on how the supply side is actually evolving beneath the macro noise.

Emerging Supply: What the Juniors Signal

When institutional analysts debate copper's macro trajectory, junior miners offer a ground-truth check on how the supply pipeline is actually evolving. Two names illustrate the current landscape:

Marimaca Copper (TSX: MARI) is advancing the Marimaca oxide project in Chile with economics that would have been unthinkable at $8,000 copper: an all-in sustaining cost of $2.29/lb, net present value of $709 million, IRR of 31%, against initial capex of $587 million. These are tier-one economics for a development-stage asset. The project's viability at well below current prices suggests that high copper prices are indeed incentivising new supply - but on timelines measured in years, not quarters.

Fitzroy Minerals (TSXV: FTZ) is exploring the Caballos copper-gold project through a joint venture with Pucobre, one of Chile's established mid-tier producers. Earlier-stage and smaller in scale, Caballos represents the kind of grassroots exploration that the industry needs to replenish its depleted project pipeline - but it also underscores how long the journey from discovery to production actually is.

Both projects reinforce the central tension: the supply response is happening, but it operates on geological time, not market time. High prices today fund the exploration and development that will deliver tonnes in 2030–2035. They do not solve the 2026 deficit, which is why the structural bull case and the speculative correction thesis can both be correct simultaneously. Layered on top of both are macro forces that amplify price in either direction, and that operate on entirely different timescales again.

Macro Amplifiers: Currency, Rates, and Geopolitics

Copper prices do not trade in a fundamental vacuum. Three macro forces are amplifying - and in some cases distorting - the underlying supply-demand signal:

USD weakness. The dollar and copper share a strong negative correlation (−0.7 to −0.8 during trending periods). Fed rate-cut expectations have softened the greenback, providing a tailwind that accounts for an estimated 10–15% of copper's appreciation. If the dollar strengthens - say, because cuts are delayed or the ECB cuts faster - this tailwind reverses into a headwind.

Interest rate environment. When real interest rates fall below 2%, institutional investors historically increase commodity allocations as inflation hedges. The current rate environment has made copper compete favourably with fixed-income alternatives for portfolio allocation. This creates "tourist" capital - money that is in copper for the macro trade, not the fundamental thesis, and that will exit at the first sign of trouble.

Geopolitical risk premiums. Trade policy uncertainty has encouraged defensive stockpiling across regions, tightening visible inventories and creating artificial scarcity signals. Resource nationalism trends, particularly in Latin America and Central Africa, add risk premiums that persist independently of immediate supply disruptions. Companies and countries increasingly prioritise supply security over cost optimisation, adding structural demand that operates independently of consumption needs.

Separating the Signal from the Positioning

Strip away the speculative overlay and what remains is a commodity with a genuinely compelling structural case - but one that does not, on its own, justify today's price. The 50-70% fundamental component of the rally corresponds to a durable repricing driven by capex underinvestment, declining ore grades, and real electrification demand. Mapped against pre-rally price levels and the cost curves of marginal producers, the structural fundamentals alone likely support a copper price in the range of $9,500 to $10,500 per tonne - which is, not coincidentally, where the base and bear scenarios converge. The premium above that range, currently around $2,400 to $3,400 per tonne, is the speculative and macro layer: $30 billion in financial inflows, trend-following momentum, and currency tailwinds that can reverse faster than any mine can open or close.

Understanding this distinction changes how an investor approaches the position. The structural case is not fragile - it will still be true after a 15% correction. What is fragile is the timing assumption baked into $12,900: that the decade-long deficit is already here, that speculative flows will remain patient, and that the dollar stays soft. None of those conditions is guaranteed, and Goldman's data suggests that the market is not being compensated for the risk that any one of them fails.

The single data point most worth tracking as conditions evolve is not the LME price itself - it is the ratio between exchange-visible inventories and open interest in copper futures. When open interest rises faster than inventories decline, speculation is outrunning physical tightness and the premium is widening. When inventories fall sharply while open interest holds steady, the deficit is becoming physical rather than financial - and the price move that follows tends to be durable. That divergence is the clearest signal available in real time that the balance between fundamental and speculative is shifting.

Analytical Assessment

"The copper market appears to be pricing the 2030–2040 supply crisis at 2026 prices. While the long-term deficit is genuine and potentially severe, the near-term risk–reward calculus at $12,900 per tonne favours patience over aggression."

- PolyMarkets Investment, Research TeamKey Analytical Takeaways

- Rally decomposition: 50–70% fundamental (supply deficits, electrification), 20–35% speculative ($30B inflows, Chinese futures surge), 10–15% macro (USD, rates). The fundamental core is solid; the speculative layer is fragile.

- Inventory paradox: Exchange-visible stocks at 255,000 tonnes (12–16 days) look tight, but off-exchange holdings of 500,000+ tonnes create uncertainty that both bulls and bears can exploit.

- Supply gap is real but slow-moving: $15B annual capex vs. $25–30B needed. Ore grades halved since 1990. New mines take 12–20 years. But near-term surplus of ~300,000 tonnes possible as existing projects ramp.

- Goldman correction thesis is credible: $13,000 → $11,000 (−15%) as speculative premium unwinds. 80% probability of lower prices within 6 months based on scenario analysis.

- Long-term bull case intact: S&P's 42Mt demand by 2040, critical-metal designations, and AI/data-centre demand create a structural floor. Any significant correction may offer historically attractive entry points for multi-year positioning.

- Time horizon determines the trade: Structural investors can ride through a correction. Speculative longs face asymmetric downside. The distinction between a good investment and a good entry point is everything.

Important Disclaimer

This article is for educational and informational purposes only and does not constitute financial advice. Commodity markets are highly volatile. Copper prices are influenced by global economic conditions, currency fluctuations, supply disruptions, and speculative positioning. The scenarios and price ranges presented are analytical estimates based on available data and may not materialise.

Past performance does not guarantee future results. Always conduct your own due diligence and consult a qualified financial advisor before making investment decisions. Consider your risk tolerance, investment objectives, and time horizon.

Research Desk, PolyMarkets Investment, January 18, 2026

Back to Articles