1 The $33 Trillion Question

Five years ago, stablecoins were a parking lot for crypto traders who didn't want to get wrecked overnight. That's it. Nobody at Visa headquarters lost sleep over them. Fast forward to March 2026, and I'm writing an analysis that involves Visa, Mastercard, SoFi, Stripe, the U.S. Congress, the European Central Bank, and $33 trillion in annual transaction volume. The shift happened faster than almost anyone in traditional finance expected - and most of them are still catching up.

On-chain stablecoin transfer volume hit $1.8 trillion in the thirty days ending March 10, 2026. That's not a typo. The previous record of $1.5 trillion was set just two months earlier. Annualized, you're looking at roughly $21.6 trillion flowing through stablecoin rails - which puts them in the same neighborhood as Visa ($14 trillion annual) and Mastercard ($8 trillion). Now, these aren't apples-to-apples comparisons. Different transaction types, different counting methods. But the raw scale? That argument is over.

What caught my attention isn't the headline figure, though. It's the velocity underneath it. In 2025, transaction volumes grew 105% while circulating supply grew just 48%. The same digital dollars cycling faster and faster through the system. Monthly transfers jumped from 755 million in January to 1.55 billion by December. And what was all that money doing? Payroll. Merchant settlements. Cross-border invoices. The boring stuff. The stuff Visa built a $600 billion market cap on.

So the question isn't whether stablecoins matter. That debate ended somewhere around the $10 trillion mark. The real question - the one I spent three weeks with 22 different research sources trying to answer - is what happens to the companies that move money today, the ones building new rails underneath them, and (most practically) where the investment opportunity actually sits.

2 From Parking Lot to Payment Rail

The origin story is simple. Crypto traders needed somewhere to park cash between bets. Bitcoin could drop 15% while you slept, so someone built tokens pegged one-for-one to the dollar. One USDT equals one USD. Done. It was a convenience layer for exchange trading and nothing more.

Then regulators did something interesting. The U.S. and EU started requiring issuers of fiat-pegged stablecoins to hold actual high-quality reserves - Treasuries, cash, repos - backing every token in circulation. That single change, as Bottomline's Colin Swain put it, turned certain stablecoins into "a real, trusted alternative to Swift, Bacs, ACH, and other payment methods we have today."

Think about what that actually means. Before regulation, holding a stablecoin meant trusting some opaque offshore entity. (Tether's early days were... not reassuring.) After regulation, holding USDC meant holding a claim on a pool of U.S. Treasury bills audited by Deloitte. Same product name, completely different asset. A digital bearer instrument backed by the safest collateral on earth.

"True market adoption of stablecoins begins when users no longer treat them as temporary parking lots for capital, but as primary instruments for saving, spending, and settling value globally."

- Chiara Munaretto, Managing Partner, Stablecoin InsiderAnd the data backs this up. Orbital's Q4 2025 Retail Payments Index documented what they called "a decisive shift from holding to usage." Small-value transactions - the $1 to $10,000 range, the ones that look like actual commerce - grew tenfold. From 316 million to 3.2 billion in a single year. USDT processed 6.72 billion transactions worth $19.1 trillion over 2025, commanding 73% of retail flows. But USDC told a different story: transaction count up 631% between Q1 and Q4, average size $557 - roughly half of USDT's. That pattern screams programmatic B2B settlement and payroll, not speculation. Two stablecoins serving two completely different economic functions. Both exploding.

3 Signal vs. Noise: What the Volume Numbers Actually Mean

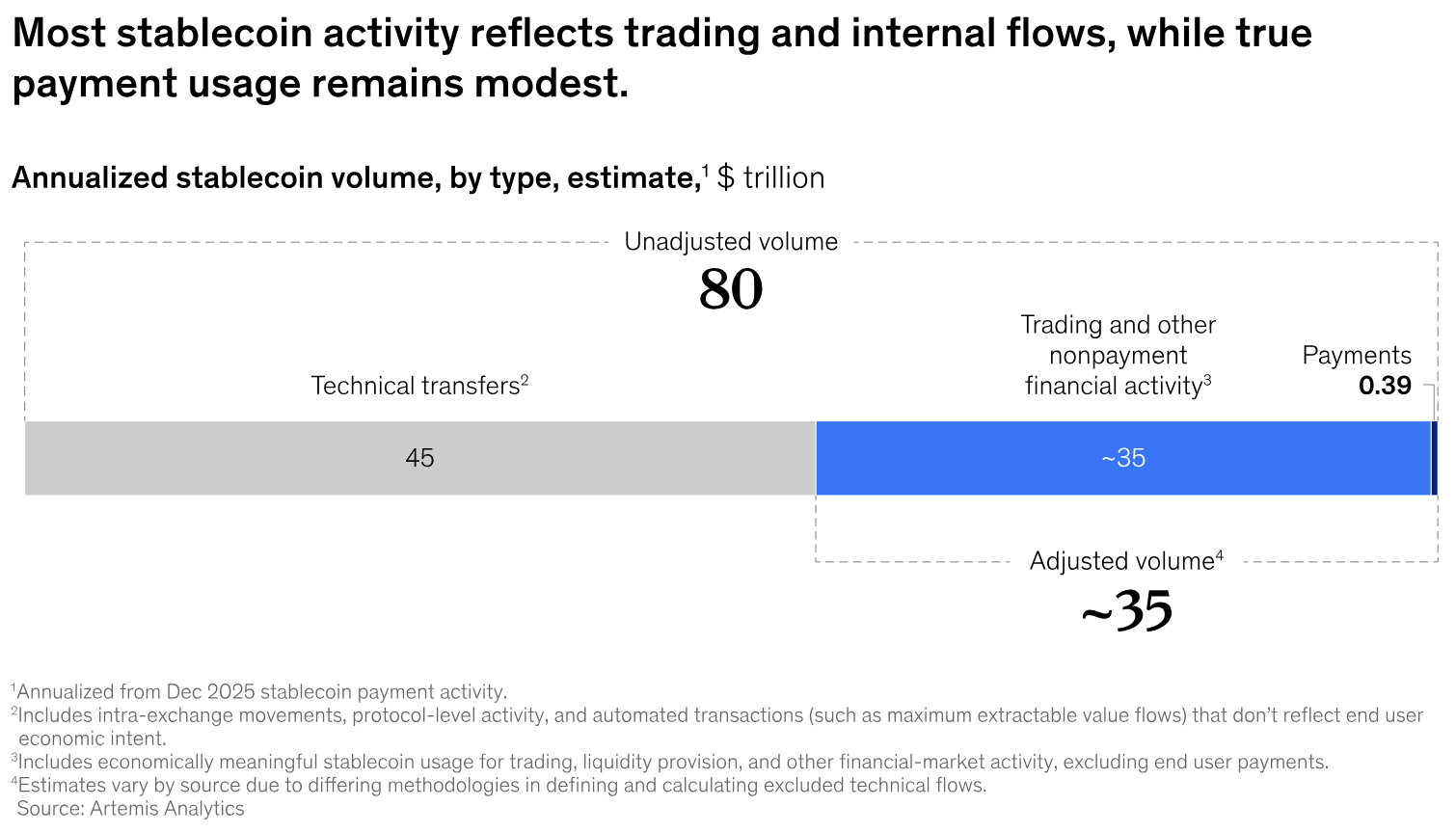

I need to be honest about something. That $33 trillion headline? It's misleading. And if we're going to do serious analysis, we need to strip it down to what's real. Fortunately, McKinsey did exactly that.

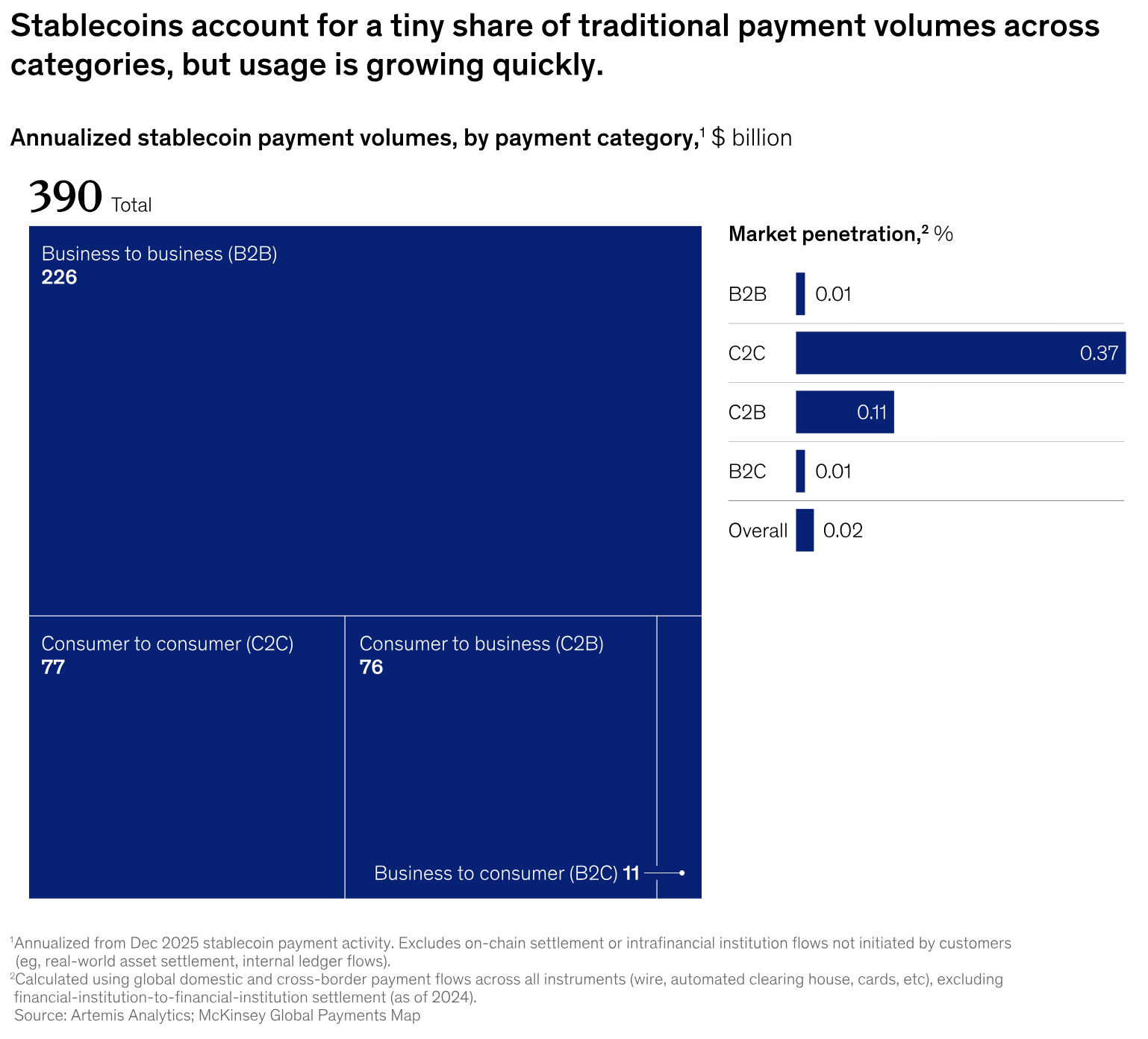

In a joint study with Artemis Analytics published March 2026, McKinsey broke on-chain stablecoin activity into three buckets: technical transfers (intra-exchange movements, smart contract loops, protocol plumbing), trading and financial activity (arbitrage, DeFi, liquidity shuffling), and actual payments. Of roughly $80 trillion in unadjusted annual volume, about $45 trillion was technical noise, $35 trillion was trading-related, and only $390 billion was genuine end-user payments. Payroll. Remittances. B2B settlements. Merchant transactions. The stuff that actually matters.

$390 billion. Not $33 trillion. A 99% haircut. That's the kind of number that separates actual research from crypto Twitter boosterism.

But here's what the bears get wrong: that $390 billion more than doubled from 2024. And the composition is where it gets interesting. B2B payments accounted for roughly $226 billion - about 60% of genuine stablecoin payment volume - growing 733% year-over-year. Consumer-to-consumer remittances hit $77 billion. C2B payments contributed $76 billion. Business-to-consumer flows (payroll, disbursements) added $11 billion. That 733% B2B growth rate is the number I keep coming back to. It tells you where this market is actually headed.

Why This Distinction Matters

Anyone quoting raw stablecoin volumes without this decomposition is either uninformed or selling something. The McKinsey framework is the clearest lens we have for seeing where real commercial activity is growing. And $390 billion - modest against the $200+ trillion global payments market - is genuine economic activity flowing through programmable, borderless dollar infrastructure. Growing faster than any payment rail in modern history. That's what matters.

The geography tells you something too. Asia-originated payments dominate at $245 billion - 60% of the total. North America contributes $95 billion, Europe $50 billion. And here's the pattern: the volume concentration maps almost perfectly onto where regulatory clarity arrived first. Singapore, Hong Kong, Japan. Meanwhile, Latin America and Africa - the places where stablecoins would arguably be most useful (currency stability, dollar access, cheaper remittances) - each sit below $1 billion. That's not a ceiling. That's a runway.

4 The Legacy Giants Respond: Visa, Mastercard, and the Integration Imperative

February 24, 2026. Citrini Research publishes a thought experiment - not a prediction, the authors were careful to say - imagining a world where AI agents route payments through stablecoins instead of card rails. The market's reaction was anything but theoretical. Mastercard fell 5.8% in a single session. Visa dropped 4.5%. Amex lost 7.2%. Capital One sank 8.8%. Over the trailing year through March, Mastercard is down 4.4% and Visa is down 7.3%, against an S&P 500 that's up 20%.

A speculative paper shouldn't move $50+ billion in market cap. But it did - because investors are quietly pricing in something uncomfortable: the 2-3% interchange fee structure that powers a combined $800+ billion market cap might not survive this decade intact.

What happened after the selloff is the part most people missed. Both networks didn't retreat. They accelerated. The pace of stablecoin announcements in the following two weeks suggested years of internal planning being compressed into days.

Visa (V)

Stablecoin settlement hit a $4.5B annualized run rate by January 2026, up 460% year-over-year. Partnered with Stripe's Bridge platform to bring stablecoin-linked cards to 100+ countries. Live in 18 countries already with on-chain settlement through Lead Bank pilot.

Key quote: "Expanding our work with Bridge gives us one more way to bring the speed, transparency, and programmability of stablecoins directly into the settlement process." - Cuy Sheffield, Head of Crypto, Visa

Mastercard (MA)

Agreed to acquire BVNK for up to $1.8B (including $300M contingent). Launched crypto partner program with 85 partners. Partnered with SoFi for stablecoin settlement across its global network. Building AgentPay framework for AI-driven transactions.

Key quote: "For us, stablecoins and agentic commerce are emerging opportunities, ones where Mastercard has a natural role to play." - CEO Michael Miebach, January 2026

Coinbase (COIN)

Stablecoin revenue hit $332.5M in Q4, up 38% YoY. USDC reserve interest shared 50/50 with Circle. Three 2026 priorities: Everything Exchange, scaling stablecoin payments, bringing the world on-chain via DeFi.

Key quote: "We're seeing AI agents adopt stablecoins for payment. I believe stablecoins will be the default payment method for AI agents." - CEO Brian Armstrong, Q4 earnings call

The strategic math is pretty simple, even if the execution is painful. If stablecoin rails are going to carry meaningful payment volume - and the growth curve says they will - Visa and Mastercard have exactly two options. Build the bridge between old rails and new ones, accepting a smaller cut on a much bigger pie. Or watch fintechs and crypto-native players build that bridge without them. That's it. There isn't a third option where blockchain goes away.

Both chose option one. And Mastercard's BVNK acquisition tells you how serious they are: $1.8 billion for a stablecoin infrastructure company processing roughly $12 billion in annualized volume. That's not a hedge. It's a bet. As Mastercard's chief product officer Jorn Lambert said on the deal call: "Adding on-chain rails to our network will support speed and programmability for virtually every type of transaction."

5 The Stablecoin Sandwich: A New Payments Architecture

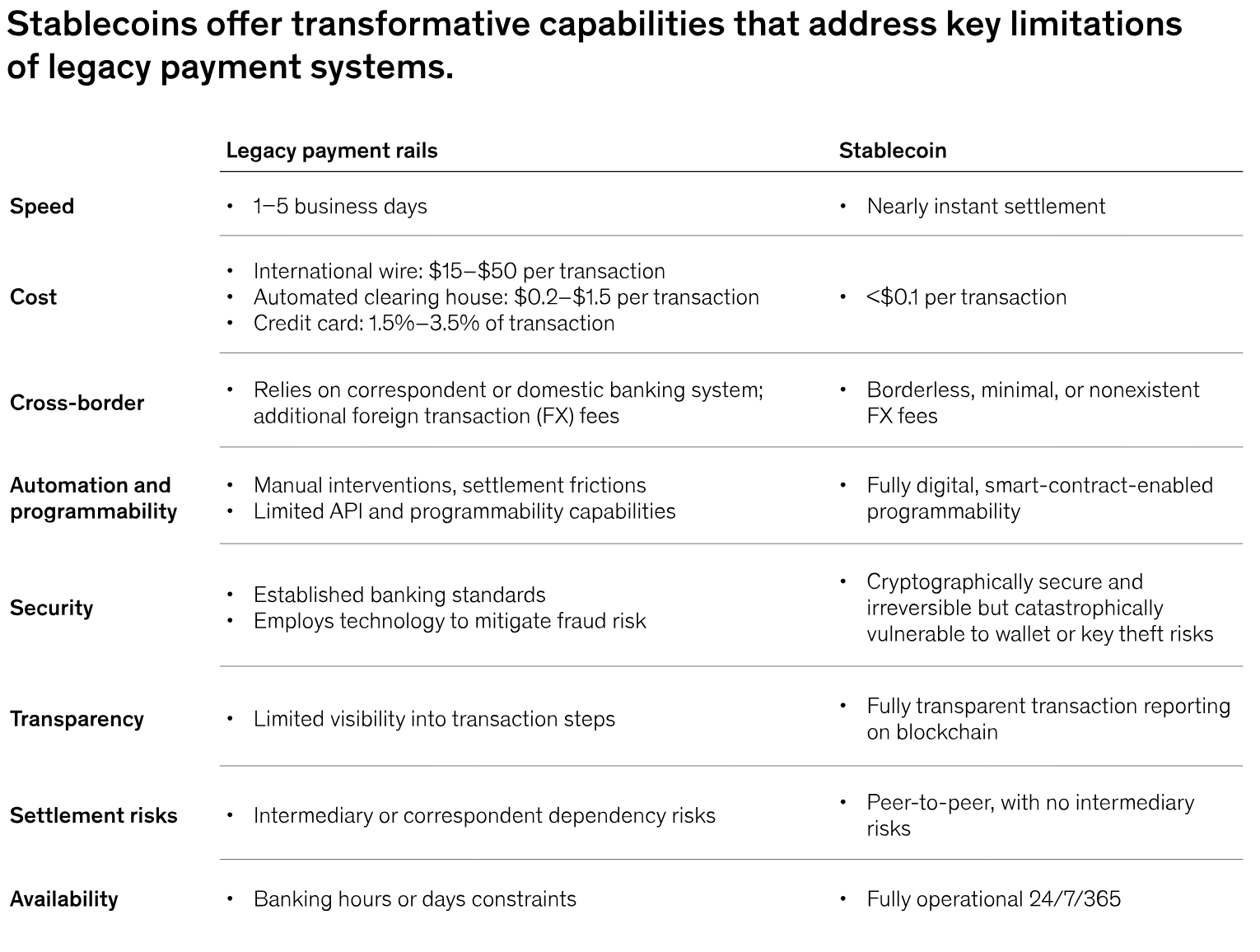

There's a new term making the rounds in payments circles: "The Stablecoin Sandwich." Sounds silly. The concept isn't. Instead of money crawling through a chain of correspondent banks - your bank to a local correspondent to an international correspondent to the recipient's local correspondent to the recipient's bank, burning 2-5 business days along the way - the new flow looks like this:

The Stablecoin Sandwich Model

Step 1: Sender pays in local fiat currency

Step 2: On-ramp partner converts to stablecoins (e.g., USDC)

Step 3: Settlement occurs on blockchain in minutes

Step 4: Off-ramp partner converts to recipient's local currency

Step 5: Recipient receives funds - faster and often cheaper

Same endpoints. Completely different rails. The blockchain becomes the invisible settlement layer - the user may never know their money traveled on-chain.

Here's a real example. A U.K. fintech needs to pay someone in Jordan. Traditional route: the payment hops from a local bank to a U.K. correspondent, then Paris, then Turkey, and after days of compliance holds, maybe it reaches Amman. Every hop takes a fee. Every delay is working capital stuck in limbo. The corporate treasurer watches the money vanish into what Bottomline's Swain calls "this ether of a world," hoping it shows up eventually.

Stablecoin route: convert to USDC at the source, settle on-chain in seconds, convert back to Jordanian dinar at the destination. Minutes. Sub-cent gas fees plus the on-ramp/off-ramp spread. The entire correspondent banking chain - all 3-7% in accumulated fees - replaced by two currency conversions and one blockchain transaction.

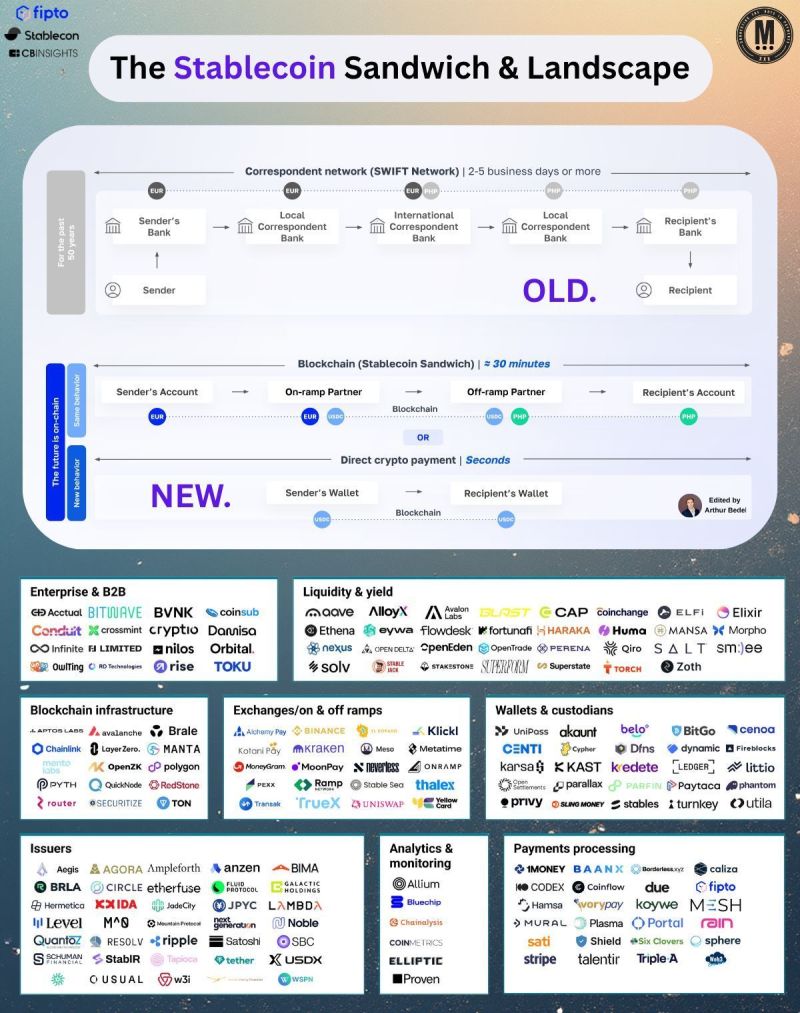

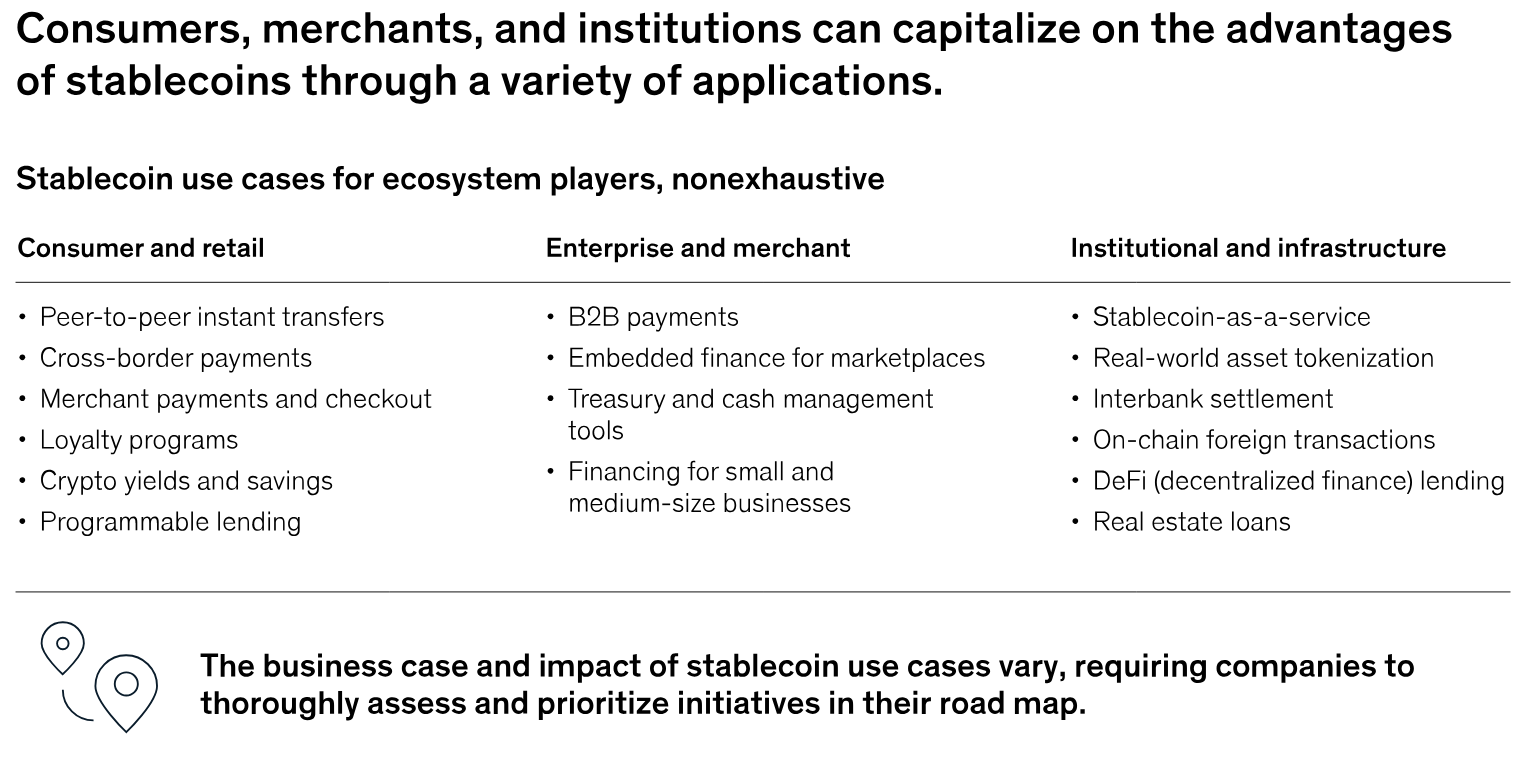

And the ecosystem building around this model is moving fast. Polygon Labs processed over $2 billion in application payment volumes in January 2026 alone. Chainlink handles oracle and cross-chain infrastructure. BitGo and Fireblocks do custody. BVNK (now Mastercard) and Fipto process the actual payments. But the most complete stack probably belongs to Stripe, which paid $1.1 billion for Bridge and now offers a single API covering on-ramps, off-ramps, cross-chain transfers, and wallet custody. SpaceX already uses Bridge to collect Starlink payments in countries where traditional banking barely works.

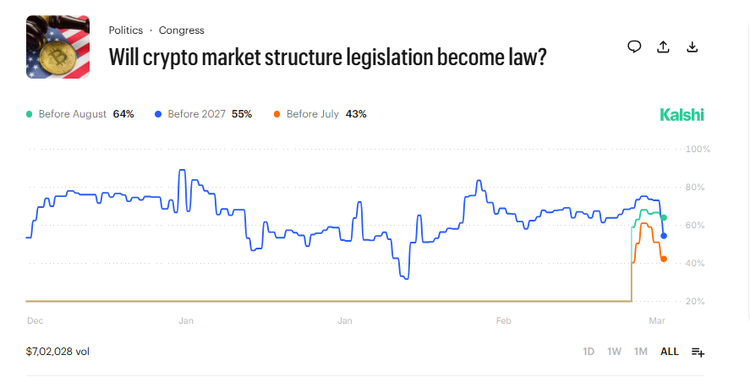

6 The Regulatory Unlock: GENIUS Act, MiCA, and the Yield War

None of what I've described above happens without regulation. And for most of stablecoins' existence, there was no regulation worth the name. That changed - and changed fast.

Why does the GENIUS Act matter more than all the rest combined? One number: 99.9% of stablecoin volume is denominated in U.S. dollars. Every mint-and-redemption cycle runs through U.S. banking infrastructure. As Orbital's Luke Wingfield Digby put it: "U.S. banks are really the lifeblood of the success of stablecoins. Regulatory clarity enables banks to participate more directly and more compliantly." No U.S. framework, no institutional adoption. Simple as that.

The Banks' Position

Jamie Dimon's argument: if stablecoin companies offer yield, they should be treated like banks and follow the same capital, liquidity, and compliance standards. Banks worry about massive deposit drawdowns if stablecoins can offer interest on balances - reducing their ability to lend.

The ECB echoed this in a March 2026 working paper: widespread stablecoin adoption "could weaken monetary policy transmission and potentially erode monetary sovereignty."

The Crypto Firms' Position

Brian Armstrong (Coinbase): "If we were prohibited from [paying yield], it would ironically just make us more profitable" - because Coinbase would keep the full Circle revenue share instead of passing it to customers.

The compromise emerging in the Clarity Act: allow rewards on users' stablecoin activities, but not balances. Loyalty-style programs permitted; bank-deposit-style interest prohibited.

This isn't some abstract policy debate, by the way. Real money is at stake - a lot of it. Coinbase earned $332.5 million from stablecoins in Q4 2025 alone, up 38% year-over-year. The USDC reserve interest, split 50/50 with Circle, drives the vast majority of that figure. Bloomberg Intelligence analysts project that stablecoin revenue (19% of Coinbase's 2025 total) could expand two to seven times under the GENIUS Act framework. Seven-fold requires a favorable Clarity Act outcome, but even the base case has stablecoin revenue becoming Coinbase's single largest business line within two years. Think about that for a second. An exchange whose identity was built on trading fees, about to make more money from stablecoins than from trading.

7 SoFi Breaks the Mold: The First Bank-Issued Stablecoin

March 18, 2026. SoFi Technologies does something that would have sounded absurd three years ago. SoFi Bank - nationally chartered, FDIC-insured, about as traditional as a digital bank gets - announces SoFiUSD. The first stablecoin issued by an insured U.S. bank on a public, permissionless blockchain.

I want to sit with that for a second. For years, stablecoins were issued by crypto-native entities. Tether, operating offshore and unbanked for much of its history. Circle, a venture-backed fintech. Now an FDIC-insured bank is minting stablecoins, with BitGo providing infrastructure through its Stablecoin-as-a-Service platform and Mastercard enabling settlement across its global network. The line between "crypto" and "banking" didn't just blur. It disappeared.

Why SoFiUSD Matters

1:1 USD backing with third-party auditor attestations. Settlement enabled across Mastercard's multi-token network. SoFi Bank will settle its own credit and debit transactions in SoFiUSD. The Galileo technology platform will offer issuing banks the choice to settle in the stablecoin.

"With SoFi-USD as a settlement currency across Mastercard's network, card issuers and acquirers can more easily enable the millions of businesses they serve around the globe to instantly settle transactions, 24 hours a day, 7 days a week." - SoFi CEO Anthony Noto

This is what convergence actually looks like in practice. Not a crypto company pretending to be a bank. A bank deciding that stablecoin rails do something its existing infrastructure can't - instant, 24/7, programmable settlement. And the fact that Mastercard integrated SoFiUSD across its network immediately? That tells you the card networks see bank-issued stablecoins as the path of least regulatory resistance to blockchain settlement. Smart. Probably right.

8 The Invisible Revolution: Stablecoin APIs and the End of Blockchain Complexity

Here's the development most people outside of fintech engineering are sleeping on: blockchain complexity has been completely abstracted away. A new generation of APIs from Stripe, Circle, Fireblocks, Paxos, Zero Hash, and BVNK lets any developer integrate stablecoin payments using the exact same REST semantics, JSON payloads, and webhook callbacks they'd use for card payments. No Solidity. No gas estimation. No wallet management headaches. The blockchain became invisible.

A Circle transfer call sends a JSON body with a source wallet, destination, amount, and idempotency key. The chain? A simple string parameter - "chain": "ETH" or "chain": "SOL". Blockchain finality shows up as familiar status values: pending, confirmed, complete, failed. Not raw block confirmations. If you've ever built an accounting API integration, this looks... normal. That's the point.

| Provider | Core Role | Key Differentiator | Notable Metric |

|---|---|---|---|

| Stripe (via Bridge) | Highest abstraction layer | Zero crypto complexity; 1.5% fee covers all blockchain costs | $1.1B Bridge acquisition; 101-country stablecoin accounts |

| Circle | Issuer-native (USDC) | CCTP V2 cross-chain burns/mints across 17 blockchains | $77B USDC market cap; $110B+ cumulative CCTP volume |

| Fireblocks | Institutional custody | MPC key management; 100+ blockchain support | $200B+/month stablecoin volume; $10T+ total secured |

| Paxos | Regulatory depth | OCC charter; powers PayPal's PYUSD, Robinhood's USDG | Market cap grew from $1B to $7.6B during 2025 |

| Zero Hash | Embeddable infra | 51 U.S. jurisdiction licenses; 2 NYDFS BitLicenses | Reportedly acquired by Mastercard for ~$2B (Oct 2025) |

| BVNK (Mastercard) | PSP/cross-border | API-first for payment service providers | $12B annualized stablecoin payment volume |

And the cost advantage isn't theoretical anymore. Sending $200 from the U.S. to Colombia: less than $0.01 via stablecoins, $12.13 through traditional channels. Sub-cent fees on Solana, sub-$0.03 on Base, near-instant finality. These are the numbers that corporate treasurers care about. Speed, cost, transparency. Stablecoin rails win on all three.

For enterprise buyers in 2026, the decision tree looks like this: Stripe if you want zero crypto complexity and seamless checkout integration. Circle for USDC-native products, especially cross-chain. Fireblocks for institutional custody with policy engines. Paxos or Bridge's Open Issuance for white-labeling your own stablecoin. Notice what's missing from that list? The question "should we integrate stablecoins?" That one's been answered.

9 The AI Agent Convergence

Brian Armstrong called stablecoins "the default payment method for AI agents" on Coinbase's Q4 earnings call. Circle CEO Jeremy Allaire said almost the exact same thing a month earlier. When two competitors independently arrive at the same conclusion, you should pay attention. They're looking at the same technical constraint.

AI agents can't open bank accounts. Can't sign credit card applications. Can't pass KYC checks designed for humans with faces and Social Security numbers. But they can hold a crypto wallet and execute stablecoin payments programmatically. Stripe and OpenAI released the Agentic Commerce Protocol in November 2025. Circle launched x402 protocol integration shortly after. The mechanics work like this: an AI agent hits an API, gets a 402 Payment Required response, and autonomously completes a USDC micropayment to proceed. No human in the loop.

This is what the Citrini paper that crashed payment stocks was actually about. Not stablecoins replacing your credit card at Starbucks - that's the naive disruption narrative. The real threat is subtler and, frankly, scarier for payment incumbents: AI agents routing billions of micro-transactions through whatever rail is cheapest, gradually bleeding volume from 2-3% interchange toward sub-cent blockchain settlement. Citrini modeled a hypothetical where Mastercard's Q1 2027 earnings showed "agent-led price optimization" and "pressure in discretionary categories." Speculative? Sure. But the mechanism is sound.

The Agentic Commerce Risk

Mastercard isn't sitting still. Their AgentPay framework integrates identity verification, trust mechanisms, and consumer protections into AI-driven transactions. The logic: if agents are going to route payments, be the trust layer they route through. But the fundamental tension doesn't go away. Agents optimize for cost. Blockchain rails are orders of magnitude cheaper than interchange. You can build all the trust layers you want - the cost differential remains.

Citrini framed their paper as a "pre-mortem" - "What if our AI bullishness continues to be right... and what if that is actually bearish?" If you own payment network stocks, that question should bother you. It's bothering the market.

10 The Central Bank Counterargument

Not everyone's excited. The European Central Bank dropped a working paper in March 2026 that reads less like academic research and more like a warning shot. The core finding: broad stablecoin adoption could "weaken monetary policy transmission and potentially erode monetary sovereignty." Heavy words from Frankfurt.

The mechanism they describe makes sense, though. Banks transmit interest rate changes to the real economy. If deposits migrate from banks to stablecoins at scale, banks end up more dependent on expensive wholesale funding, lend less, and the credit transmission mechanism weakens. The ECB warned these effects are "nonlinear" - there's a tipping point where the damage accelerates fast. They didn't specify where that tipping point sits. Nobody knows.

But the third finding is the one that should worry anyone holding European bank stocks: dollar-denominated stablecoins adopted widely in Europe would effectively import American monetary conditions into the eurozone. The ECB's own words: this "would weaken the central bank's control over financial conditions, reduce the effectiveness of traditional monetary policy instruments, and make it harder to stabilize inflation and economic activity." Dollarization through the back door. And the ECB knows it.

This isn't crypto skepticism. It's a sophisticated monetary policy argument, and it explains why MiCA is so much more restrictive than the GENIUS Act. It also explains the digital euro push - the ECB wants a public alternative that preserves sovereignty while not looking like it's anti-innovation.

For investors, the ECB paper previews a specific kind of risk: regulatory friction in non-dollar economies. Euro-pegged stablecoins remain tiny - $500 million market cap in mid-2025, though EURC transactions grew tenfold. If Europe successfully ring-fences its financial system from dollar stablecoins, Citi's $1.9 trillion base case may prove optimistic for the eurozone portion. The dollar-denominated market? Different story entirely.

11 The B2B Killer App: Cross-Border Payments

If I had to pick one use case that defines where stablecoins are going, it's not consumer payments. It's not DeFi. Not trading. It's B2B cross-border settlement. And the numbers aren't even close.

Sending $200 internationally through traditional channels costs 6.5% on average (BIS, Q1 2025). Only 35% of retail cross-border payments land within one hour - against a G20 target of 75% that nobody seems to be hitting. B2B is worse: each intermediary bank in a SWIFT chain deducts fees and adds delays. Total cost typically runs 3-7% of payment value once you fold in FX spreads, intermediary charges, and compliance overhead. On a $1 million corporate payment, that's $30,000 to $70,000 in friction.

Stablecoins collapse that structure entirely. B2B stablecoin payments went from under $100 million monthly in early 2023 to over $6 billion by mid-2025. That growth curve doesn't look like speculation. It looks like companies discovering they can save 90% on cross-border settlement and telling their CFOs about it. BVNK (now Mastercard) processed $30 billion annualized in 2025, up 2.3x year-over-year, with a third from the U.S. market alone. Deel and Remote offer stablecoin payroll across 120+ countries. This isn't experimental anymore.

The Cross-Border Advantage in Practice

Speed: Settlement in minutes vs. 2-5 business days. In specific corridors, stablecoins settle transactions 500x faster than traditional systems.

Cost: Sending $200 from the U.S. to Colombia costs less than $0.01 via stablecoins vs. $12.13 through traditional channels.

Transparency: End-to-end traceability on blockchain - no more watching money disappear into "the ether of a world."

FX management: Corporate treasurers can hold dollar-pegged stablecoin balances as working capital without traditional foreign currency account structures.

Emerging market relevance: An estimated 66% of global stablecoin supply is held by individuals in emerging markets, where stablecoins mitigate currency instability and limited dollar access (Goldman Sachs Global Institute).

South Asia alone saw stablecoin-driven crypto volumes rise 80% to $300 billion between January and July 2025. Industry projections put stablecoins at 5-10% of all cross-border payments by 2030 - $2.1 to $4.2 trillion annually. For some perspective, that's larger than the GDP of most G20 nations.

12 Where the Volume Lives: Chain Economics and the USDC Flip

Something interesting happened in February 2026 that most people missed. USDC overtook USDT in transfer volume for the first time. Ever. USDC processed approximately $1.26 trillion - 70% of all stablecoin transaction activity during the month. USDT recorded $514 billion. Now, USDT still has the bigger market cap ($184 billion vs. USDC's $77 billion), but the usage data has diverged sharply from the supply data. More supply doesn't mean more usage. This distinction matters more than most analysts appreciate.

The volume distribution across blockchains tells you which chains are doing what:

| Network | Monthly Volume | Share | Avg. Tx Size | Primary Use |

|---|---|---|---|---|

| Ethereum | $620B | 34% | ~$68,000 | Institutional transfers, OTC, DeFi |

| Solana | $580B | 32% | ~$5,200 | Payments, remittances, high-frequency |

| Tron | $310B | 17% | - | Asian payment corridors, P2P |

| L2s (Arbitrum, Base, OP) | $180B | 10% | - | Low-cost payments, DeFi overflow |

| Other (BNB, Avalanche) | $110B | 7% | - | Regional, application-specific |

Look at the average transaction sizes. Ethereum at $68,000 - that's institutional money. OTC trades, large-value settlements, DeFi protocol interactions. Solana at $5,200 with sub-cent fees and sub-second finality - that's payments. This isn't a chain war. It's natural market segmentation. Ethereum is SWIFT. Solana is ACH. Different tools for different jobs, and both are growing.

13 The $1.9 Trillion Question: Market Size Forecasts

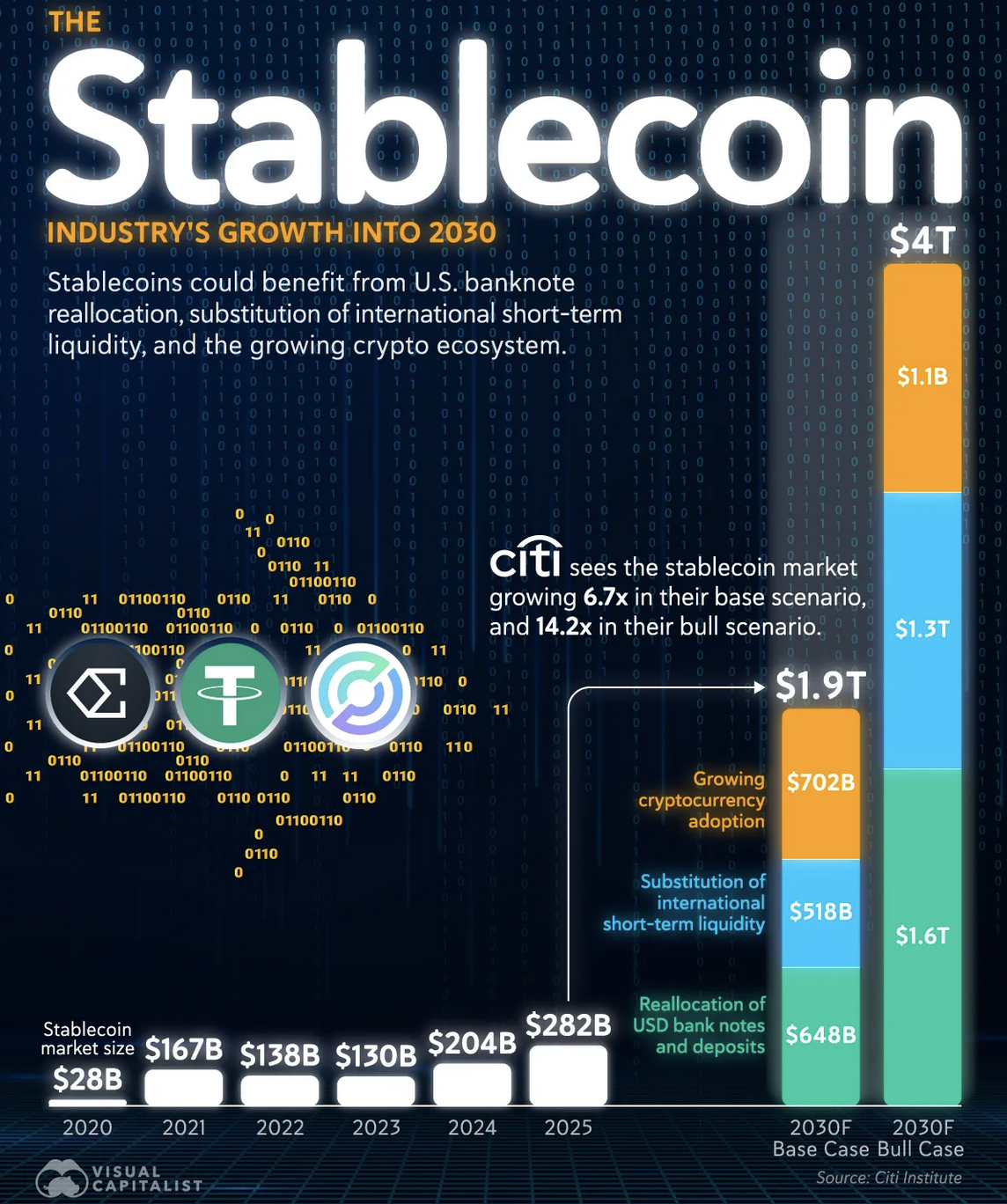

From $28 billion in 2020 to $282 billion in 2025. Tenfold in five years. And the people projecting what comes next aren't crypto influencers with laser-eye profile pictures. Citi's base case: $1.9 trillion by 2030. Bull case: $4 trillion. U.S. Treasury Secretary Scott Bessent has publicly stated $3 trillion. These are the most conservative forecasters in finance, and they're all pointing in the same direction.

Citi breaks their base case into three pillars: $648 billion from people and institutions swapping physical dollars and bank deposits into digital tokens, $518 billion from stablecoins replacing international short-term liquidity instruments (think: corporate treasury management, cross-border working capital), and $702 billion from continued crypto ecosystem adoption. The bull case roughly doubles each bucket.

The near-term marker to watch: stablecoin circulation is projected to cross $1 trillion by late 2026. If that happens, we're on the Citi base-case trajectory. Monthly on-chain volume could hit $3 trillion by year-end, up from $1.8 trillion in February. And here's a detail that doesn't get enough attention: stablecoin issuers already hold about $155 billion in U.S. Treasury bills collectively. That makes them one of the largest holders of U.S. government debt on the planet. Think about the incentive structure that creates. Washington has a direct financial interest in stablecoin growth. Every new USDC minted means more Treasury demand.

14 What Could Go Wrong: The Honest Bear Case

I've spent most of this piece building the bull case. Time to be honest about what could go wrong. Any analysis that only shows you the upside is advertising, not research. Here's what keeps me up at night:

Risk Register

Counterparty and compliance risk: "It is very easy to send stablecoin to a wallet that you have got no idea who owns," warns Bottomline's Swain. Trust in the asset is not the same as trust in the counterparty. Approximately two-thirds of consumer-to-merchant stablecoin payments still originate from exchange accounts. Three exchanges (Binance, OKX, Bybit) account for roughly 75% of those flows. The plumbing is being built, but it remains exchange-dependent.

Irrecoverability: Immediate finality removes settlement risk but also removes recall options. In traditional systems, fraudulent payments may still be recoverable. On blockchain rails, money sent to a wrong address is typically gone forever.

Monetary sovereignty erosion: The ECB's warning is real. Dollar-denominated stablecoins adopted widely in non-dollar economies effectively dollarize those economies by the back door. This is why MiCA is restrictive, and why more developing nations may follow suit.

Regulatory whiplash: The Clarity Act could still stall. Circle (CRCL) dropped 18% in a single day when reports indicated the latest draft narrowly limits stablecoin rewards. Coinbase and Circle are both down 24-26% year-to-date. The legislative path, while probable, is not certain.

The "Supply Stagnation Paradox": In Q4 2025, total stablecoin supply sat at $311 billion and barely moved, growing just 1.3% after a 16% surge in Q3. Daily active users plateaued near four million. Without fresh regulatory-enabled issuance, the system may be running at capacity with the dollars already on-chain.

Circle's stock performance deserves a closer look because it embodies the regulatory risk in one ticker. IPO'd on NYSE in June 2025 at $31, now down 24% in 2026. The company's fate is almost entirely tied to the yield debate. If the Clarity Act kills stablecoin yield, USDC becomes less attractive versus bank deposits. If it permits activity-based rewards, Circle's distribution economics flip dramatically. There's no middle ground. It's a binary outcome for Circle's biggest growth driver, and the market is pricing in uncertainty by selling first and asking questions later.

15 The Investment Landscape: Where the Opportunity Sits

Most investors I talk to still think of stablecoins as "a crypto thing." It's not. Or at least, it's not just that anymore. The opportunity set spans payments infrastructure, regulatory arbitrage, and increasingly traditional banking. Here's how I'm thinking about the positioning:

Strategic Positioning Framework

Visa (V) and Mastercard (MA): The "adapt or die" plays. Both trading at compressed multiples relative to the S&P 500 due to stablecoin disruption fears. The bear case assumes interchange fees erode; the bull case notes that both networks are aggressively integrating stablecoin settlement. MA's 17.6% revenue growth and 45.7% profit margins suggest the duopoly remains intact - for now. 39 analysts maintain a Strong Buy with a median target of $662 (30% upside from current levels).

Coinbase (COIN): The infrastructure play. $7.2B total 2025 revenue. 12 products over $100M annualized. Stablecoin revenue growing 38% YoY. Stores 12% of all crypto in the world. The risk: 26% YTD decline reflects broader crypto market weakness and regulatory uncertainty. The opportunity: if stablecoin revenue expands 2-7x as Bloomberg Intelligence projects, the current valuation looks cheap.

Circle (CRCL): The pure-play issuer. $77B USDC market cap, 25% stablecoin market share, MiCA-compliant for European access. The risk: 24% YTD decline, binary Clarity Act outcome on yield. The opportunity: USDC is the regulated stablecoin of choice for institutional settlement, and every new Visa/Mastercard/Stripe integration reinforces that position.

SoFi (SOFI): The banking bridge. First FDIC-insured bank to issue a stablecoin. Mastercard settlement integration. If bank-issued stablecoins become the regulatory preferred model, SoFi has a structural first-mover advantage.

Stripe (STRIP): The platform play. $1.1B Bridge acquisition, 101-country stablecoin financial accounts, Open Issuance for branded stablecoins. Bloomberg reports Meta is exploring stablecoin payments across Facebook, Instagram, and WhatsApp with Stripe as likely integration partner. If accurate, this could be the consumer adoption catalyst the ecosystem has been waiting for.

16 The Conclusion: Financial Infrastructure, Not a Crypto Story

Stablecoins in 2026 aren't a crypto story. They're a financial infrastructure story. And the difference between those two things is about $30 trillion in addressable market.

After spending weeks with 22 separate research sources - earnings calls, McKinsey analyses, regulatory filings, central bank working papers, Citi forecasts - the picture that emerges is surprisingly clear. Stablecoins have found genuine product-market fit in a specific set of payment use cases: B2B cross-border settlement, remittances, payroll in underserved corridors, and emerging-market dollar access. Not because of $33 trillion in headline volume (most of which is noise). Because of $390 billion in real payment flows that doubled year-over-year. Growing faster than any payment rail in modern history. That's the number that matters.

The regulatory infrastructure exists. The technology has been abstracted to the point where a REST API call is a REST API call, whether you're moving card payments or stablecoins. And the institutional infrastructure? Visa, Mastercard, Stripe, SoFi, Coinbase, Circle - they're all racing to become the plumbing. Not debating whether to participate. Racing to win.

What makes 2026 different from 2021 or 2023 isn't the growth rate. It's what's driving the growth. Payroll. Merchant settlements. Corporate treasury management. Cross-border invoicing. The boring, high-margin, recurring-revenue stuff that traditional payments companies built monopolies on. That's where stablecoins are landing now.

Patrick Hennes, a digital assets expert quoted in a Venturebloxx report, framed it in terms a central banker would understand: stablecoins "are forming a new monetary layer and positioning themselves as a future extension of the M1 and M2 money supply." Two years ago, that kind of statement would have gotten you laughed out of a room at the Fed. With the Treasury Secretary projecting $3 trillion in stablecoin supply by 2030, nobody's laughing.

The plumbing is going in. Whether you're positioned for it or not.

Important Disclaimer

This article is for educational and analytical purposes only and does not constitute financial advice. Stablecoin and cryptocurrency investments carry significant risks including regulatory changes, technology failures, counterparty risk, and potential loss of value. The regulatory landscape described herein is evolving rapidly and may change materially from what is described.

Market projections are estimates from third-party sources (Citi, McKinsey, Bloomberg Intelligence) and may differ materially from actual results. Past performance and growth rates are not indicative of future results. Consider consulting a financial advisor before making investment decisions based on this analysis.

PolyMarkets Investment Strategies, Market Research, March 26, 2026