Opening Perspective

I almost passed on this one. "Consolidated Water" - a sub-$500M market cap company headquartered in the Cayman Islands, producing desalinated seawater for Caribbean island utilities - doesn't exactly scream opportunity. It sounds like the kind of company you discover on page 14 of a stock screener, shrug at, and move on. That's precisely why I'm writing this.

What stopped me was a number I don't often see: negative net debt. The company carries $99.4M in cash and virtually no debt. At a $400M market cap, the enterprise you're actually paying for is worth roughly $300M - a water infrastructure business that has operated profitably since 1973, paid dividends since 1985, and just signed a $204M contract to build and operate a desalination plant in Hawaii for the next two-plus decades. The market is valuing 20 years of recurring O&M revenue from that contract at almost nothing.

The Q4 2024 earnings call (March 18, nine days ago) was telling. Revenue dropped 47% year-over-year - but only because two large construction projects were completed in early 2024. CEO Rick McTaggart was calm about it: "We knew this was coming." Meanwhile, recurring operations-and-maintenance revenues grew 51% to $29.3M. The company is quietly becoming more stable as a business even as the headline revenue number falls off a cliff. And construction - the volatile, high-margin driver - is coming back hard in 2026 when Hawaii breaks ground.

There is regulatory risk in Cayman. There is client-payment risk in the Bahamas. This is a microcap with thin liquidity and a non-Big-Four auditor. I am not pretending otherwise. But at $23–$26, the math on risk-reward is compelling enough that it deserves a position.

Key Metrics at a Glance

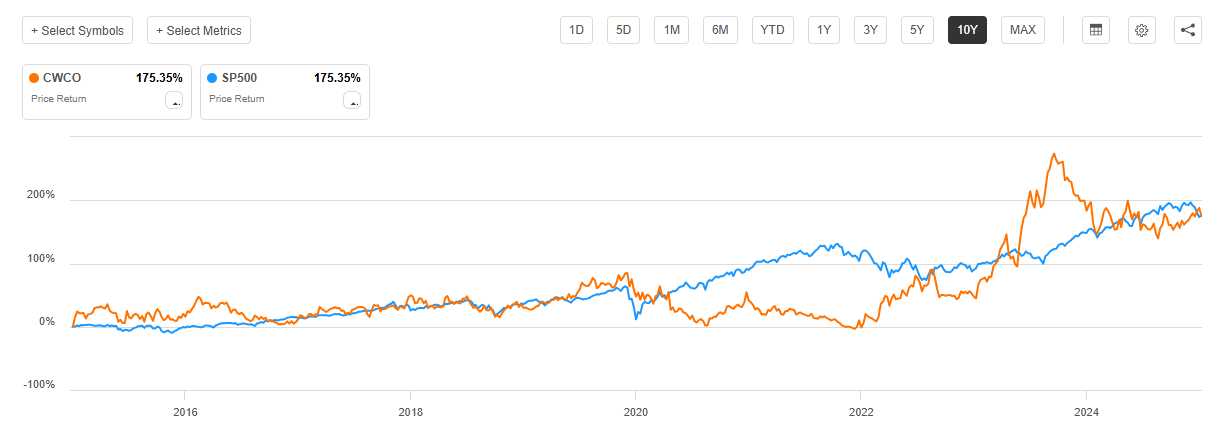

The Stock Nobody Watched - And Then It Doubled

Over the past decade, Consolidated Water has matched the S&P 500 almost tick-for-tick - a 175% total return from a microcap Caribbean water company that few institutional investors bother to cover. The catch: almost all of that outperformance came in a single surge during 2023, when a new desalination plant in Cayman and construction contracts in Hawaii and the Caribbean all crystallised simultaneously. The stock ran from under $14 to over $40. Then it gave half of it back. We're now back near the base of that rally - with an even better earnings profile and a larger catalyst on the horizon.

The historical pattern is instructive: CWCO is a sleeper with episodic catalysts. Long stretches of sideways movement, then a sharp re-rating when growth materialises. The 2023 spike was one of those episodes. The 2026 Hawaii construction commencement could be the next one - and this time the setup is cleaner because the stock has already retreated to entry-level prices while the balance sheet has actually improved.

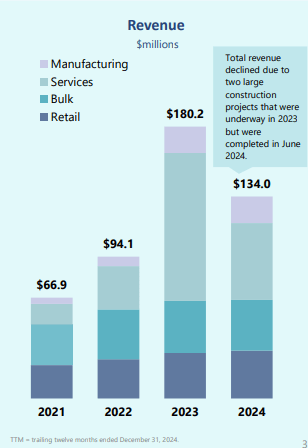

Four Revenue Streams, One Overlooked Business

The "water utility" label is misleading. Consolidated Water operates across four distinct segments - the most exciting of which (Services) looks terrible right now because two large projects were completed in 2024. Beneath the surface, the mix is actually shifting toward something more durable.

The crown jewel. Exclusive utility concession in Grand Cayman - CWCO produces all potable water for two of the island's most populated areas via reverse osmosis. Record volumes in 2024: 4.3% more customer accounts, 4.5% more water sold. Highest margins in the group. The island keeps growing.

Sells treated water wholesale to state utilities in the Caymans and Bahamas. The Bahamas client (WSC) is the concentration risk - and a chronic late-payer - but $28M in receivables has always eventually been settled with interest. The cash-heavy balance sheet turns this from a threat into an inconvenience.

The volatile segment - design-build-operate contracts. Construction revenue fell from $77.3M in 2023 to $17.6M in 2024 as two projects finished. But the underlying shift is important: O&M contract revenues grew 51% to $29.3M (plus additional project, technical, and management services revenues). PERC Water and the new REC (Colorado) subsidiary are building a recurring revenue base that's changing the segment's character permanently.

Aerex Industries - an OEM supplier of water production and treatment equipment, operating in Fort Pierce, Florida. Revenue stable at $17–18M; margins improving on better product mix and fabrication efficiency. Aerex is expanding its facility (completion late 2025) to run more jobs simultaneously. A quiet compounder inside a compounder.

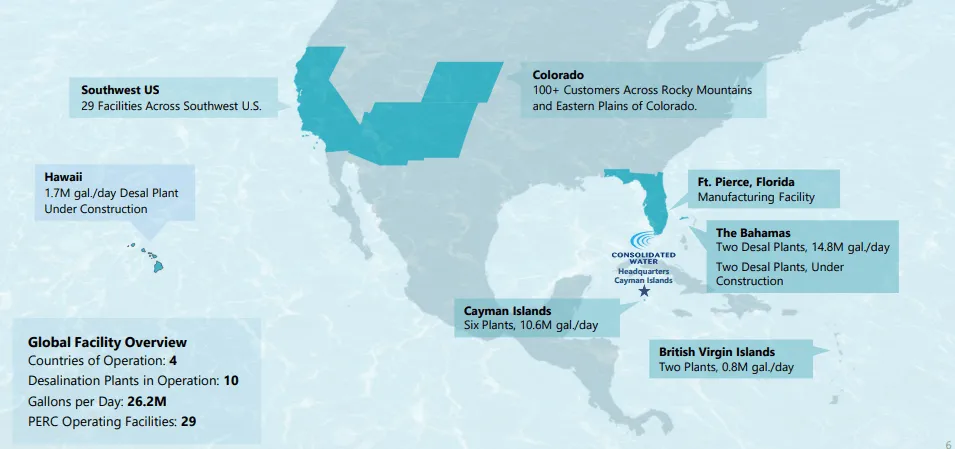

The Geographic Footprint

Twenty-nine operating facilities across four countries - from the Florida Gulf Coast manufacturing plant to desalination operations in Cayman, Bahamas, BVI, and the soon-to-break-ground Hawaii project. The US exposure is growing: Colorado, Arizona, Hawaii, and California are all active or targeted markets. Every geography the company operates in has inelastic water demand - islands cannot import water, and drought-stressed US states have no alternative to treatment technology.

One thing that gets overlooked in the geographic story: the US segments (Services and Manufacturing) carry no tariff risk and may actually benefit from policies favouring domestic water infrastructure. When the company discusses its Colorado and California O&M expansion, it is entering markets where every other operator also faces chronic water scarcity. The competitive moat isn't brand - it's the decades of RO technology know-how that makes Consolidated Water one of the few businesses that can actually build, operate, and guarantee output for a state water authority.

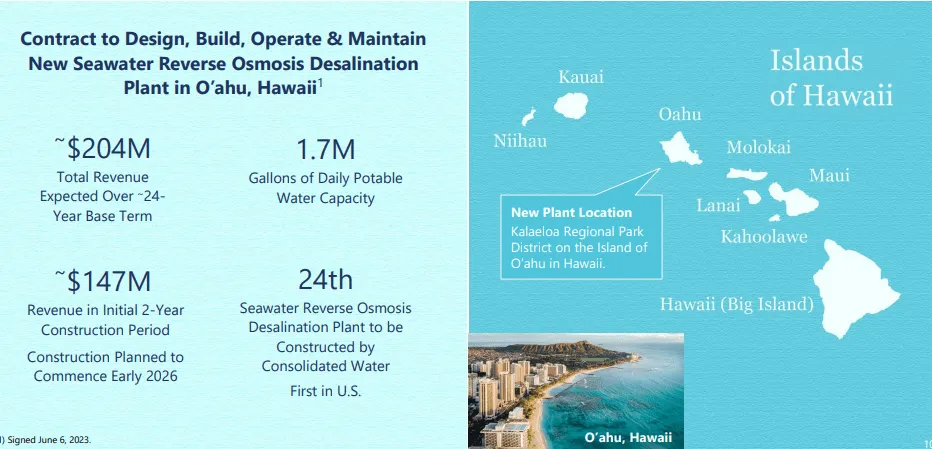

The $204M Catalyst Nobody Is Watching

Kalaeloa Desalco - Hawaii Seawater Desalination Project

In 2021, Consolidated Water's subsidiary Kalaeloa Desalco LLC was awarded a $204M contract to design, build, and operate a 1.7-million-gallon-per-day seawater reverse-osmosis plant for the Honolulu Board of Water Supply. Construction is expected to begin early 2026, with the bulk of revenues recognised in 2026 and 2027.

After construction, the company will operate the plant under a 20-year O&M agreement, with two 5-year extension options. Critically, approximately 80% of the construction cost is subject to inflation adjustments from the original contract date - preserving the margin against years of cost inflation since 2021.

The April 2025 pilot testing determination is the next binary milestone. A positive outcome clears the path for construction to begin on schedule.

The EV Math - Why Hawaii Changes Everything

Why the Market Is Mispricing This

Most analysts who cover CWCO - and there are only a handful - focus on TTM earnings. At $17.9M in continuing-ops net income against a $400M market cap, the stock looks expensive at ~22× P/E (trailing twelve months). But that multiple ignores the $99M cash buffer (real EV is $300M, so EV/earnings is ~17×), and it ignores the forward earnings profile entirely. 2025 is a trough year - management has said so explicitly. The construction gap between completed projects and Hawaii's commencement creates the illusion that the business is shrinking. It isn't. Recurring O&M is growing. West Bay is expanding. Aerex is investing in capacity. And in early 2026, a $204M construction contract begins generating revenue at margins that could match or exceed 2023.

A stock that looks like it is in decline but is actually coiling for a construction-driven re-rating is exactly the kind of setup that gets missed in a market obsessed with quarter-to-quarter trends. The entry window - while 2025 earnings disappoint - is the thesis.

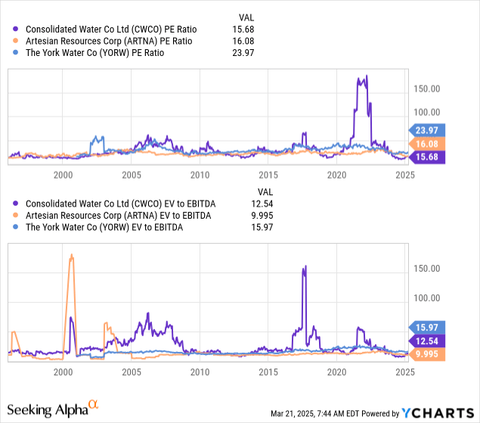

Valuation Context - Cheap vs Peers

Artesian Resources (ARTNA) and York Water (YORW) are the closest US-listed microcap water comparables. Both trade at 23–24× P/E. Both carry meaningful debt - neither has anything close to Consolidated Water's fortress balance sheet. CWCO's P/E of ~15.7× at entry reflects persistent scepticism about earnings consistency, but misses three things: (1) the debt-free balance sheet warrants a premium, not a discount; (2) the O&M growth profile is rapidly increasing earnings quality; and (3) construction revenue will surge in 2026–2027. The re-rating potential when that happens is precisely why we are entering now.

The dividend history adds another layer to the quality argument. Paid every quarter since 1985 - 40 consecutive years - with a 15% dividend increase announced alongside FY2024 results. Management raises dividends when they are confident about forward cash generation. That signal, delivered nine days before this note, is not being priced in.

Risk Register - Conditions & Forecasts

Every investment has a weather risk. These are CWCO's - assessed honestly, without softening, alongside the factors that make each manageable.

A new concession was issued in February 2025, confirming Cayman Water's exclusive supply rights. However, a separate operating license from the new utility regulator OfReg is still pending, with discussions not yet commenced. The company and analysts widely expect the eventual terms to reduce margins somewhat. The company has been investing in its Cayman infrastructure (new HQ, West Bay expansion) - suggesting it is confident in a reasonable outcome. Crucially, CWCO's debt-free status gives it patience that a leveraged utility would not have.

The Water and Sewerage Corporation of the Bahamas is chronically late. At year-end 2024, CWCO held $28M in receivables from WSC with zero bad debt reserves - because, historically, WSC has always eventually paid, including interest on overdue balances. The risk is liquidity strain if the situation deteriorates. The $99M cash balance makes this a working capital inconvenience, not an existential threat.

With the Liberty Utilities and Red Gate II construction projects complete, 2025 construction revenues will remain subdued until Hawaii commences. Management expects this; the market may react negatively to lower interim earnings without appreciating the 2026 recovery. The risk here is not financial impairment but price action during a disappointing earnings year - potentially extending the entry window but requiring patience.

The Honolulu Board of Water Supply must decide by end of April 2025 whether CWCO's pilot testing demonstrated adequate water quality match to existing supplies. A positive answer advances construction significantly. A negative outcome could trigger delays, redesign, or - in a worst case - contract renegotiation. Management submitted the enhanced pilot testing report and expressed confidence, but this is a binary event. The stock may react meaningfully either way.

CWCO trades roughly 100,000 shares per day. For institutional size this is negligible, but for individual investors taking a meaningful position, entry and exit require patience and discipline. Bid-ask spreads can widen on low-volume days. This is a stock where gradual position building at entry levels is warranted rather than chasing. The upside of illiquidity: the market is slow to price in new information, which is partly why this opportunity exists.

Three Tides - Bear, Base & Bull

These scenarios are built around the key variables: Hawaii regulatory outcome, Cayman margin impact, and O&M growth trajectory. Each assumes purchase at the midpoint of the entry zone (~$24.50).

Hawaii pilot testing fails or delays materially. Cayman OfReg terms cut retail margins by 25–30%. Bahamas WSC payment dispute escalates. O&M growth stalls. The stock de-rates back to 2022 levels. Even in this scenario, the $99M cash pile prevents a catastrophic outcome and supports the stock floor.

Hawaii pilot approved by April. Construction begins 2026. Cayman license resolved with moderate (10–15%) margin reduction. O&M revenues continue growing at 20–30% per year. 2026 earnings re-rating: market applies 18–20× to anticipated forward earnings as Hawaii construction revenues build. Stock re-rates through 2025 H2 – 2026.

Hawaii on schedule, margins preserved by inflation adjustment. Cayman licence negotiated favourably. Additional O&M contracts in California or a bolt-on acquisition in the US Southwest. Aerex manufacturing expansion unlocks new project volume. Market re-rates CWCO toward York Water's 24× P/E multiple given improved earnings quality.

Catalyst Milestones

Cayman Islands government issued a new concession to Cayman Water Company confirming exclusive rights to produce and supply water in its service area. The first major regulatory hurdle is cleared; OfReg licence discussions are next.

Enhanced pilot testing report submitted to the Honolulu Board of Water Supply. 60% engineering design reached and submitted to client's engineers. All prerequisites for the April determination are in place.

The Honolulu Board of Water Supply must confirm CWCO demonstrated a reasonable water quality match. A positive determination unlocks the path to construction commencement - the most important near-term catalyst. This is the event to watch.

The West Bay desalination plant expansion in Grand Cayman adds 1 million gallons per day of capacity. Expected to drive retail revenue growth starting H2 2025 as Cayman's growing population base absorbs new supply.

CWCO is negotiating or constructing three projects with a combined value of approximately $20M. These partially bridge the 2025 construction revenue gap and generate positive cash flow before Hawaii begins.

Aerex (Fort Pierce, Florida) completes a manufacturing facility expansion, adding assembly and storage capacity. Enables simultaneous handling of larger project volumes - directly supporting the Hawaii build and any future O&M equipment requirements.

The $204M Kalaeloa project breaks ground. Revenue from this phase - the largest single contract in company history - begins flowing into the income statement. This is the event that the stock should begin pricing in during late 2025, well before it hits the P&L.

Total revenues likely exceed $180M again - matching or surpassing 2023 highs. If net income reverts to the 2023 pattern, two consecutive $28–32M earnings years deliver ~$60M of earnings against a $300M enterprise value. The re-rating should be well underway by this point.

Post-construction, CWCO operates the Honolulu plant under a 20-year O&M contract - with two 5-year extension options. This recurring revenue stream, invisible to current earnings models, transforms the long-term earnings profile of the Services segment permanently.

Position Parameters

The following scenarios reflect the author’s personal analysis and are not investment recommendations. See our full disclaimer.

Trade Setup - Consolidated Water Co. Ltd. (NASDAQ: CWCO)

Entry targets the current pullback from 2023 highs. Consider building a position gradually given thin liquidity (~100k shares/day). The April 2025 Hawaii determination is a binary catalyst - consider sizing conservatively until that outcome is known. Stop is placed below the pre-rally 2022 base level. Dividend yield of ~1.7% provides partial compensation while waiting for 2026 construction revenues to materialise.