There is a particular kind of opportunity that appears only when the market is looking elsewhere. Boeing is embroiled in quality scandals and production shortfalls. Airbus is sold out until the end of the decade. And somewhere in São José dos Campos, Brazil, the world’s third-largest aircraft manufacturer is quietly posting its highest backlog in seven years, watching its margins inflect upward for the first time since the pandemic, and preparing to collect on a decade of product development that nearly ended in a fire sale to Boeing.

Embraer is entering what its own CEO calls “harvest season.” The company spent the last five years restructuring, deleveraging, and refreshing its product portfolio after Boeing walked away from a $4.2 billion deal in 2020, leaving Embraer with $300 million in sunk costs and a bruised reputation. What followed was a turnaround that the market has only partially recognized: a $21.1 billion backlog, an S&P upgrade to investment grade, and four business segments all pointing in the same direction for the first time in the company’s history.

This briefing examines why Embraer at $27–$31 may represent one of the most compelling risk/reward setups in the aerospace sector. The thesis rests on four engines - commercial aviation recovery, executive jet dominance, C-390 military expansion, and high-margin services - each independently capable of driving the stock higher, and collectively pointing toward a re-rating that the consensus has not yet priced in.

To understand Embraer’s current opportunity, you need to understand what nearly killed the company. In 2018, Boeing agreed to acquire 80% of Embraer’s commercial aviation division for $4.2 billion. The deal would have effectively ended Embraer as an independent planemaker. Then the 737 MAX crashes happened. The pandemic hit. And in April 2020, Boeing terminated the agreement, leaving Embraer holding the bill for roughly $300 million in carve-in/out costs and posting a $121 million loss in Q3 2020.

It was, in retrospect, the best thing that ever happened to the company.

Forced to stand on its own, Embraer’s management under CEO Francisco Gomes Neto launched an aggressive turnaround: cutting costs, deleveraging the balance sheet, and investing in the product portfolio they had nearly sold for parts. The results have been quietly spectacular. Net Debt/EBITDA fell from 2.3x in 2022 to 1.4x in 2023. S&P upgraded the credit rating to investment grade BBB−. Free cash flow hit $318 million in 2023 - more than double the guidance of $150 million. And the backlog swelled to $21.1 billion, the highest level in seven years, driven by orders across all four segments.

“For now, we have a very young and competitive portfolio of products developed in less than 10 years and we are in a good moment. We want to sell those products and improve our financial performance.”

- Francisco Gomes Neto, CEO, EmbraerThe CEO’s choice of words is deliberate. “Harvest season” means no expensive new aircraft development programs that would drain cash flow and distract management. Instead, the company is focused on monetizing its existing E2 commercial jets, Phenom and Praetor executive aircraft, C-390 military transporter, and a rapidly growing services business. This is a capital-light, cash-generative phase of the cycle - precisely the phase where aerospace companies re-rate.

Meanwhile, Embraer’s two largest competitors are creating a vacuum. Boeing’s ongoing quality and production struggles have reduced its output and consumer confidence. Airbus has its production sold out for the better part of the decade. Airlines need aircraft. They cannot wait five years for a delivery slot from Toulouse or Seattle. Embraer has production available from 2026 onward - and the world is starting to notice.

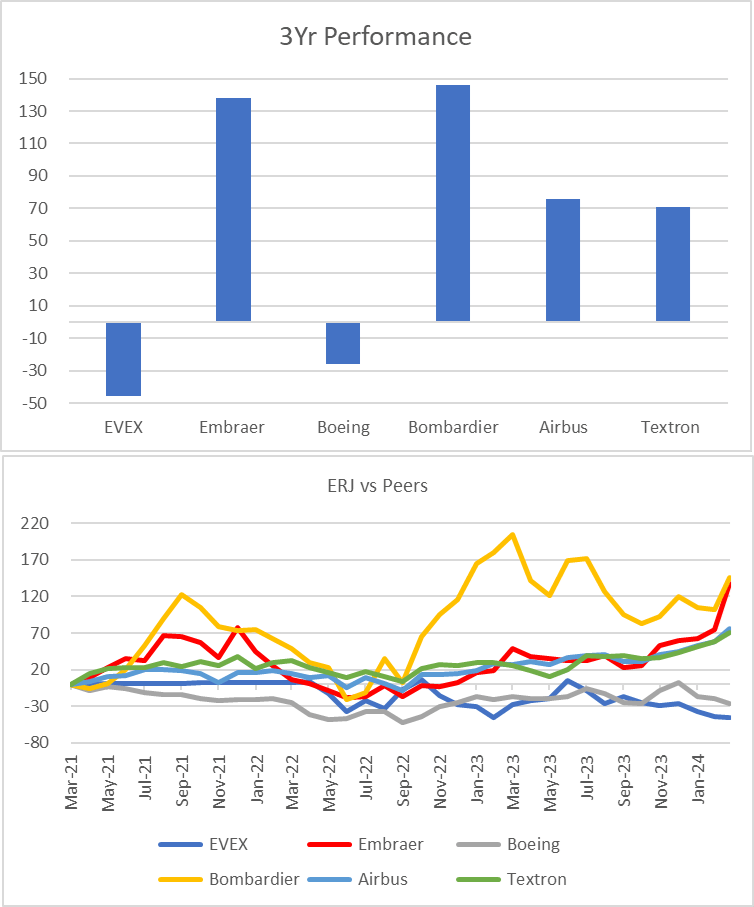

The stock has already moved - up roughly 130% from its mid-2022 bottom - but the thesis is not about what has happened. It is about what is still not priced in. Specifically: the NetJets optionality worth up to $5 billion that sits outside the disclosed backlog, the C-390’s $60 billion addressable market with only seven aircraft delivered to date, the Pratt & Whitney GTF engine contract that could add $500 million in annual high-margin services revenue, and a potential Boeing arbitration resolution. Each of these represents a catalyst the consensus has not fully modeled.

Embraer is the undisputed leader in commercial jets with up to 150 seats. Its E-Jet family - spanning the E170, E175, E190, and E195 - is the backbone of regional aviation worldwide, operated by carriers including Delta, American Airlines, JetBlue, Austrian Airlines, and Aeromexico. The newer E2 generation (E190-E2 and E195-E2) offers 17.3% lower fuel burn than its predecessor, fly-by-wire controls, 120-minute ETOPS certification, and what the company claims is the best seat-mile cost among all single-aisle jets.

The commercial segment has been the slowest to recover from the pandemic, with deliveries falling from a peak of 162 jets in 2008 to just 44 in 2020. But the trajectory is now firmly upward: 48 deliveries in 2021, 57 in 2022, 64 in 2023, and guidance for 72–80 in 2024. Management expects to approach “very close back to the three digits” in 2025 - a statement that implies approximately 90–100 deliveries, restoring production rates not seen since 2014.

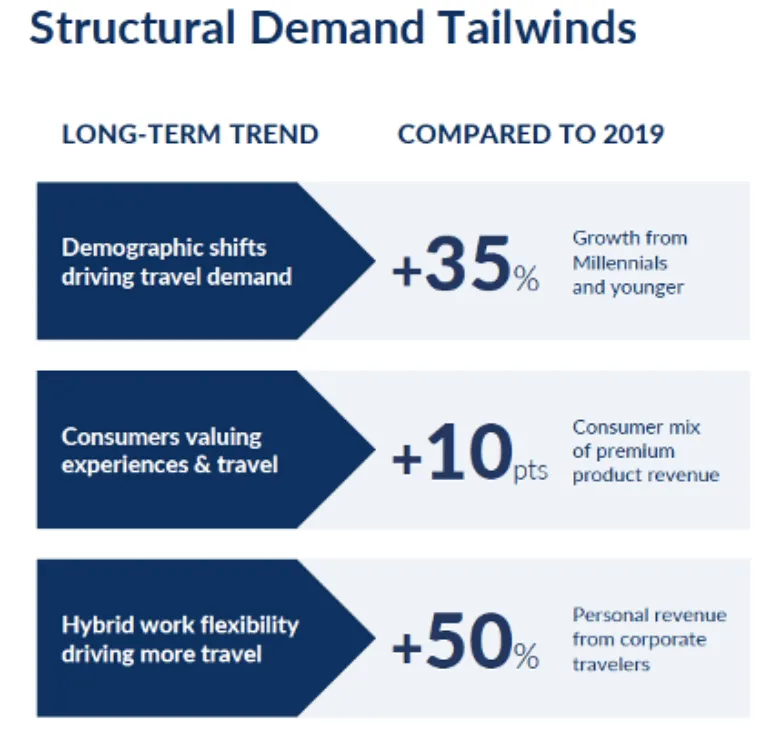

The catalyst for this acceleration is twofold. First, structural demand. Global revenue passenger kilometers (RPK) are expected to increase 9.8% in 2024, surpassing even the 4.5% growth seen in pre-pandemic 2019. Delta Air Lines’ Investor Day data reveals that demographic shifts - Millennials and younger cohorts - are driving 35% more travel demand compared to 2019, while hybrid work flexibility is generating 50% more personal revenue from corporate travelers.

Second, the supply constraint. Boeing and Airbus are capacity-constrained, unable to fulfill existing orders let alone take new ones for near-term delivery. This creates a structural opening for Embraer. American Airlines’ landmark order for 90 E175 aircraft (plus options for 43 more) - the largest single Embraer order since 2016 - was not an act of charity. It was a rational decision by a major carrier that needed planes it could actually receive.

“We currently have concrete sales campaigns for more than 200 aircraft across the world for both our E1 and E2 jet families.”

- Francisco Gomes Neto, CEO, Q1 2024 Earnings CallIn the US regional market, Embraer enjoys a unique protective moat: union agreements that limit regional jet weight to 39 tonnes. The E2 series is heavier and cannot compete in this segment, but the E175 can - and it dominates. By 2030, an average of 40 aircraft in the sub-76-seat category will be retired annually in the US, creating a predictable replacement cycle that Embraer is uniquely positioned to capture. The company is also targeting the aging Bombardier CRJ 700/900 fleet, expanding its addressable market beyond just E1 replacements.

Internationally, the E195-E2 is finding traction. China’s CAAC has certified the E2, opening the world’s fastest-growing aviation market. Singapore’s carriers are using E2s to open new routes and increase frequency. The aircraft’s 6-hour range and ETOPS certification give it operational flexibility that many airlines find compelling as a complement to their narrowbody fleets.

The commercial segment posted just 1.1% EBIT margins in 2023, but this is a high-fixed-cost business where margins leverage sharply with volume. Management targets 3–4% EBIT margin in 2024, rising to 5–6% as deliveries scale. By 2026, NHM Capital estimates the segment could generate approximately $150 million in adjusted EBIT versus just $20 million in 2023 - a 7.5x increase driven primarily by volume, not pricing. The historical margin profile for Embraer’s commercial division was “double-digit territory in the mid-teens” at peak production - a level that current volume trends suggest is achievable again by the late 2020s.

If commercial aviation is Embraer’s recovery story, executive aviation is its profit engine. The Phenom 300 has been the most delivered light jet globally for twelve consecutive years and the most delivered twin-jet for four straight years. Within the specific super-mid segment (approximately 3,000-4,000 nautical mile range, 6-8 passenger configuration), the Praetor 500 and Citation Latitude together dominate the order book, with the Praetor holding approximately 33% and the Latitude approximately 67% of combined deliveries in this sub-segment. The broader mid-size business jet market includes additional competitors in adjacent configurations (Bombardier Challenger 350, Pilatus PC-24, and others), but in the directly comparable super-mid range and cabin class, this is a duopoly where Embraer has a co-dominant position.

Q1 2024 was the “highest Q1 in terms of sales, deliveries and revenues for the division over the past eight years,” per the CEO. Eighteen jets delivered - 125% more than Q1 2023. Light jets up 83% year-over-year (11 Phenoms); medium jets more than tripled (7 Praetors). Revenue hit $240 million, a 175% increase, with gross margins swinging from negative 0.5% to positive 21.4%. The turnaround in this segment is not incremental - it is explosive.

The backlog tells an equally compelling story. Executive aviation backlog reached $4.3 billion at year-end 2023 - the highest since 2011 - having more than tripled in just three years from $1.2 billion in 2020. New delivery slots are sold out until Q1 2026. The company delivered 115 aircraft in 2023 (+13% YoY) and is investing in production capacity increases in both Brazil and the United States to meet demand.

But here is where the story gets genuinely interesting. NetJets has options for 250 Praetor 500 jets worth approximately $5 billion. So far, only five firm orders have been converted from these options, with deliveries beginning in 2025. These 250 options are not included in Embraer’s disclosed $4.6 billion executive aviation backlog. To put that in context: if NetJets exercises even half of those options, it would more than double the executive aviation backlog and create a multi-year revenue tailwind that the market has essentially assigned zero probability.

“Delivering our models to NetJets naturally balances the market.”

- Alvadi Serpa Junior, Director, Market & Product Intelligence, Executive AviationNHM Capital projects executive aviation revenue growing from $1.4 billion in 2023 to nearly $2 billion by 2026, with EBIT margins expanding from 9% to 10.5%. Management’s own target is EBIT margins “in excess of 10%” within two to three years. North America and the Caribbean account for 57% of Embraer executive jets in operation (1,015 units), making the US market the center of gravity for this segment - and the NetJets relationship its single most important growth lever.

Embraer’s defense segment has historically been the “black box” of the company - volatile, government-dependent, and difficult to forecast. But two products are changing that narrative. The A-29 Super Tucano light attack and trainer aircraft has been adopted by over 60 armed forces worldwide. And the C-390 Millennium military transport is emerging as perhaps the most significant competitive threat to Lockheed Martin’s C-130 Hercules in half a century.

The numbers tell the story. The C-390 carries 57,000 lbs of payload versus the C-130J’s 42,000 lbs. Maximum range: 4,600 nautical miles versus 3,510. Cruise speed: 540 mph versus 400 mph. Maximum speed: 614 mph versus 417 mph. Lower operating costs. It is faster, carries more, flies further, and costs less to operate. The C-390 uses technology derived from the E190 commercial jet, giving it the reliability and supply chain of a proven commercial platform - a significant advantage over the C-130, whose design dates to the 1950s.

| Specification | Embraer C-390 | Lockheed C-130J | Advantage |

|---|---|---|---|

| Payload | 57,000 lbs | 42,000 lbs | +36% C-390 |

| Max Range | 4,600 nm | 3,510 nm | +31% C-390 |

| Cruise Speed | 540 mph | 400 mph | +35% C-390 |

| Max Speed | 614 mph | 417 mph | +47% C-390 |

| Operating Costs | Lower | Higher | C-390 |

Confirmed orders include Brazil (19 aircraft), Portugal (5), Hungary (2), the Netherlands (5), Austria (4), the Czech Republic (2), and South Korea. Seven aircraft have been delivered so far - six to Brazil and one to Portugal. The first Hungarian C-390 completed its maiden flight during Q1 2024. Additionally, 11 C-390 aircraft in three active tender offers are not yet included in the backlog.

The total addressable market is staggering. Embraer estimates a $60 billion opportunity over 20 years for approximately 490 aircraft - and this excludes the US, Russia, China, and several other countries. Most tactical airlifters in operation were delivered between 1960 and 1990. Approximately 260 large transport aircraft (45,000 lbs+ class) are over 45 years old and approaching mandatory retirement. Peak deliveries in this category occurred in the 1970s at 185 aircraft; by the 2020s, only four were delivered. The replacement cycle is not speculative - it is an engineering inevitability.

Perhaps the most intriguing development is India. Embraer signed a memorandum of understanding with Mahindra to jointly pursue the sale of C-390s to the Indian Air Force, which has been evaluating a requirement for 40–80 aircraft. A single Indian order could match or exceed the entire current defense backlog of $2.5 billion.

“We have a Super Tucano production line in Jacksonville. We are expanding the team and are open to partnerships with the U.S. government and acquisition opportunities.”

- João Bosco Costa Jr., CEO, Defense & SecurityEmbraer is also actively pursuing the US defense market, where regulations require defense operations to be conducted by local companies. The company is considering M&A to establish a US presence for the C-390 and already collaborates with Sierra Nevada Corporation for Super Tucano production at a facility in Jacksonville, Florida. A partnership with Saab creates potential cross-selling opportunities - Saab helps sell the C-390, Embraer helps sell the Gripen fighter - with Sweden as a potential new market.

Management expects up to $750 million in defense revenue in 2024, with margins targeting mid-to-high single digits near term and double digits as the C-390 production rate climbs toward a capacity of 10 aircraft per year. NHM Capital projects the segment reaching nearly $1 billion in revenue by 2026 at 9% EBIT margins.

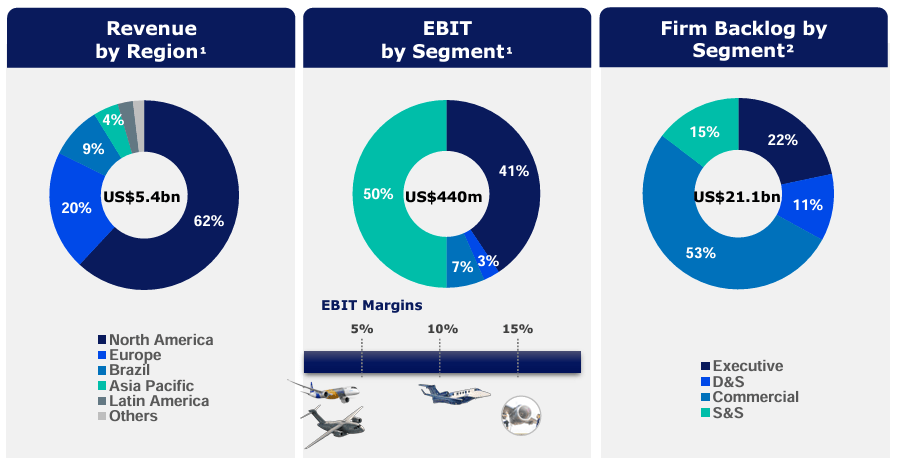

Services is quietly the most important segment of the Embraer story. With 15% EBIT margins and an all-time-high backlog of $3.1 billion, this division generates approximately half of the company’s total adjusted EBIT while requiring minimal capital investment. It is the recurring-revenue anchor that makes the entire investment case viable, and it is about to get significantly bigger.

Embraer operates 12 owned MRO (Maintenance, Repair, and Overhaul) facilities and partners with over 80 authorized service centers worldwide. The installed base of 8,000+ aircraft creates a captive revenue stream that grows naturally as more planes are delivered. Revenue has climbed from $920 million in 2020 to $1.42 billion in 2023, with EBIT margins improving from negative 2.1% to positive 15.2% over the same period.

The game-changer is the Pratt & Whitney GTF engine contract. Embraer’s joint venture with OGMA - a Portuguese MRO facility (65% Embraer / 35% Portuguese government) near Lisbon - has signed a $13 billion agreement to service Pratt & Whitney GTF 1100 engines. These are the engines that power the Airbus A320neo family, the E2 family, and other next-generation narrowbodies. The first engine was inducted at OGMA during Q1 2024, with revenue expected to ramp from $50 million in 2024 to approximately $500 million annually by 2028.

Think about what this means: Embraer is going to service Airbus engines. The competitor’s aircraft will generate high-margin recurring revenue for Embraer’s services division. It is a masterful strategic move that transforms a competitor’s market dominance into a tailwind for Embraer’s most profitable business line. NHM Capital projects the services segment reaching $2.15 billion in revenue by 2026 with 16.1% EBIT margins - a business that alone would merit a premium valuation multiple.

The consolidated picture is compelling. NHM Capital estimates total revenue reaching $8.17 billion by 2026 at an 8.9% EBIT margin, producing $729 million in adjusted EBIT and $954 million in adjusted EBITDA. This represents a company that has essentially doubled its revenue in six years while expanding margins from deeply negative to approaching double digits. The trajectory from “turnaround” to “growth compounder” is well underway.

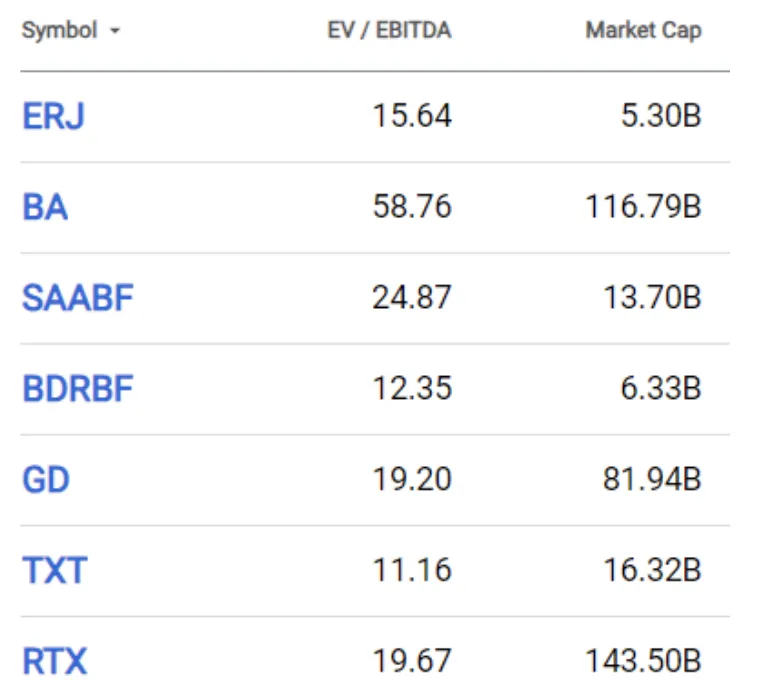

Embraer trades at approximately 15.6x trailing EV/EBITDA. At first glance, that appears roughly in line with its peer group. But the context tells a different story.

Excluding Boeing (whose 58.8x EV/EBITDA reflects ongoing crisis, not fair value), the peer average sits at 17.15x. Embraer trades at an 8.8% discount to this average. But here is the critical nuance: Embraer has the fastest revenue growth in the group at 15.7% sales CAGR - compared to Airbus at 11.8%, Boeing at 11.7%, and Textron at 5.2%. In any rational valuation framework, the fastest grower should command a premium, not a discount.

| Metric | Embraer | Airbus | Boeing | Textron | Bombardier |

|---|---|---|---|---|---|

| Market Cap | $5.3B | - | $116B | $16.3B | $6.3B |

| Revenue | $5.35B | - | $76B | $13.8B | $7.9B |

| Rev CAGR (3Y) | 15.7% | 11.8% | 11.7% | 5.2% | 5.3% |

| EBITDA Margin | 10.7% | 13.3% | 3.5% | 12.2% | 15.8% |

| Net Debt/EBITDA | 1.4x | - | 12.9x | 1.4x | 5.1x |

| EV/EBITDA ’26E | ~7.5x | 9.9x | 12.3x | 10.2x | 5.2x |

| ROE | 9% | - | - | 13.3% | - |

The forward picture is where the disconnect becomes most apparent. On a 2026 EV/EBITDA basis, Embraer trades at roughly 7.5x - its 20-year historical average. Airbus trades at 9.9x. Textron at 10.2x. Even Bombardier, with higher leverage and slower growth, trades at 5.2x. NHM Capital’s price target of $44 is based on 8x 2026E EBITDA - still a 20% discount to Airbus and Textron, which compensates for Embraer’s smaller scale and Brazilian country risk. Consensus (Capital IQ) uses 8.5x, and several analysts employ sum-of-the-parts methodologies with higher multiples for the services and executive jet segments. The direction of travel in analyst sentiment is clear: multiples are expanding, not contracting.

A third analyst targets $31.10 at 7.5x EV/EBITDA including $5 per share for Embraer’s 88.5% stake in Eve, the eVTOL subsidiary. At Eve’s current share price of $5.44, that stake is worth approximately $1.3 billion - a free option on the urban air mobility market that sits on Embraer’s balance sheet and is largely ignored in the core valuation.

Hidden Value Summary: NetJets options (~$5B, not in backlog) + 11 C-390s in active tenders (not in backlog) + Eve stake (~$1.3B) + Boeing arbitration resolution (pending). The disclosed backlog of $21.1B may materially understate the true forward revenue visibility.

The following scenarios reflect my analysis of how the stock may perform over the next 6–12 months based on the convergence or divergence of the four growth engines outlined above. These are analytical frameworks, not investment recommendations.

I am positioning for the cruising-to-climbing range. The scenario entry zone of $27–$31 provides a margin of safety relative to the base case and meaningful upside to the bull scenario. From a mid-entry of $29, the target zone of $45–$55 represents 55–90% upside, while downside to the bear case ($22–$26) implies roughly 10–24% risk. The risk/reward ratio of approximately 1:3.5 is attractive for a company with investment-grade credit, a $21 billion backlog, and four independently de-risked growth engines.

No investment thesis is complete without an honest accounting of what could go wrong. Embraer operates in a capital-intensive, cyclical industry with long production lead times, geopolitical exposure, and dependence on complex global supply chains. Here are the risks I am monitoring.

There is a question I keep returning to when evaluating Embraer, and it is this: what happens when a company that spent five years fixing itself enters a market environment tailor-made for exactly what it sells?

The answer is what we are seeing now. Boeing, which tried to buy Embraer’s commercial aviation division for $4.2 billion in 2018, is now Embraer’s greatest unintentional benefactor. Boeing’s production problems and quality crises have opened a gap in the market that Embraer is uniquely positioned to fill - not because Embraer planned for Boeing to stumble, but because it spent the years since the failed merger building the balance sheet, products, and relationships needed to capitalize on exactly this kind of opportunity. If the Boeing deal had closed, none of this would be happening. The E175 and E2 families would be Boeing products, the C-390 would likely be underinvested, and the services business would not have the independence to pursue the Pratt & Whitney GTF contract. The failed merger was Embraer’s chrysalis.

What makes this thesis compelling is not any single catalyst - it is the convergence of four independent growth engines, each at a different stage of maturation, each with its own margin expansion trajectory, and each with identifiable near-term catalysts that the consensus has not fully priced in. The commercial segment is recovering volume toward pre-pandemic levels. The executive segment is delivering record quarters with $5 billion in unrecognized NetJets optionality. The defense segment is deploying a C-130 replacement into a $60 billion market with only seven aircraft delivered. And the services segment is about to add $500 million in annual high-margin revenue from servicing a competitor’s engines.

“We are now in our harvest season. We are focusing on selling and delivering the current existing portfolio of products… we don’t have concrete plans to develop or launch a narrowbody or other aircraft in the next few years.”

- Francisco Gomes Neto, CEO, Q1 2024 Earnings CallThe CEO’s discipline is the thesis. In an industry where companies routinely destroy shareholder value by chasing expensive development programs, Embraer is choosing to monetize what it has already built. No multi-billion-dollar narrowbody gamble. No dilutive acquisitions. Just production ramp, margin expansion, and cash generation from a portfolio of products that are demonstrably competitive in their respective segments. The S&P upgrade to BBB− is the market’s acknowledgment that the turnaround is real. The backlog of $21.1 billion - four years of revenue visibility - is the order book’s acknowledgment. What remains is the stock price’s acknowledgment.

Drawing on NHM Capital’s primary research alongside four analytical lenses applied throughout this document - peer valuation comparison, backlog and optionality analysis, defense segment modelling, and services revenue trajectory - the integrated thesis is this: Embraer at $27–$31 is a de-risked aerospace compounder trading at a discount to peers with slower growth, weaker balance sheets, and less backlog visibility. The “harvest season” framework tells us management is capital-disciplined. The peer comparison tells us the market is undervaluing the growth trajectory. The backlog analysis tells us there are billions in undisclosed optionality. The defense analysis tells us the C-390 is a genuine franchise in its infancy. And the services analysis tells us the highest-margin segment is about to get significantly bigger.

The bear case is real - supply chain risk, Eve’s cash drain, country risk, and competition from Airbus are genuine concerns that I am not dismissing. But the balance of evidence suggests these risks are more than compensated by the backlog depth, margin trajectory, and catalyst density. The question is not whether Embraer is a good company - the turnaround has already proven that. The question is whether the market has fully priced in what a good company looks like at the beginning of its harvest season, in an environment where its two largest competitors are constrained, its order book is at a seven-year high, and its most profitable segments are inflecting simultaneously.

My assessment is that it has not. Not yet.

Research Desk, PolyMarkets Investment Strategies

Disclaimer: This market tip represents the author’s personal research and analysis as of July 18, 2024. It does not constitute financial advice or an investment recommendation. Embraer operates in a cyclical, capital-intensive industry subject to supply chain disruption, geopolitical risk, competitive dynamics, and macroeconomic headwinds. Always conduct your own due diligence and consult with a qualified financial advisor before making investment decisions. Past performance is not indicative of future results.