The Most Powerful Advertising Engine on Earth

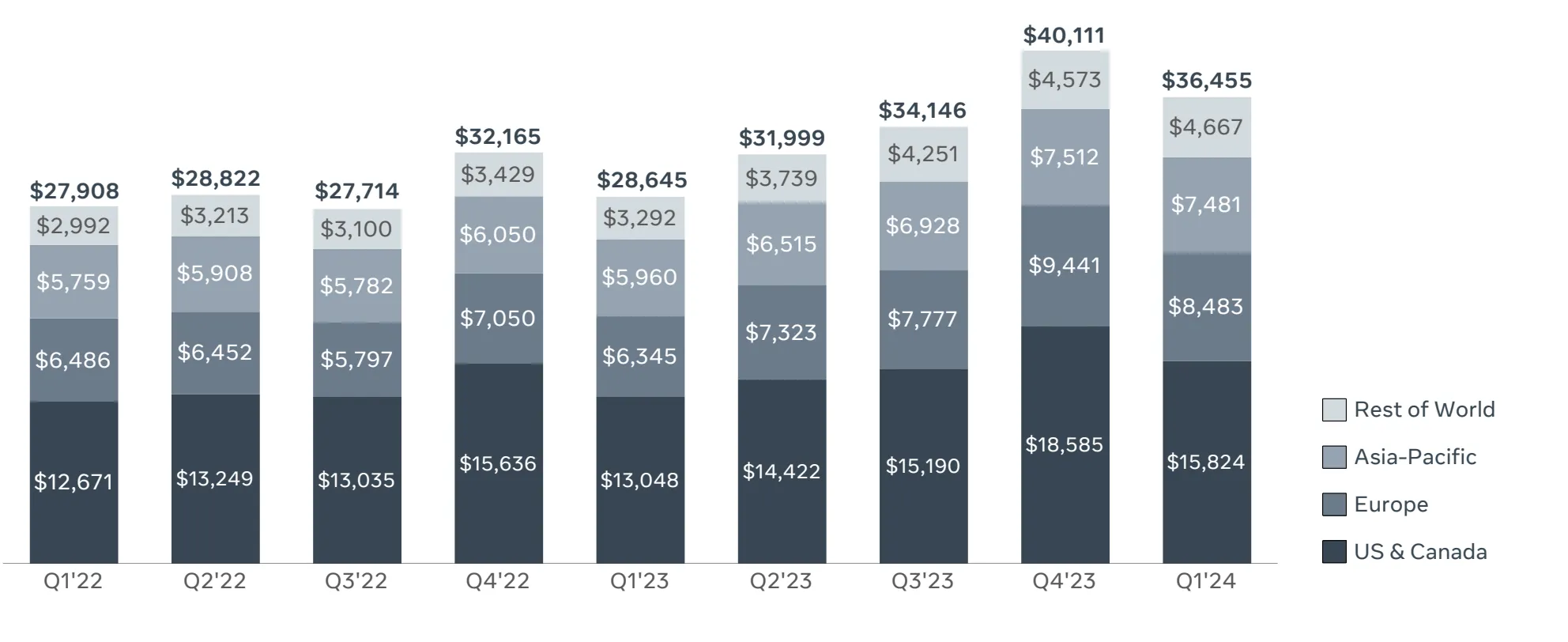

Before discussing what Meta could become, it is worth pausing to appreciate what Meta already is. The company generated $36.5 billion in revenue in Q1 2024 alone, up 27% year-over-year - its fastest rate of expansion for any quarter in three years. This growth is not coming from one geography or one product. It is broad-based and accelerating.

The geographic breakdown tells a story that many investors underappreciate. While the US & Canada segment remains Meta’s largest revenue contributor at $15.8 billion, the real acceleration is happening internationally. Europe delivered $8.5 billion (up 34% YoY), Asia-Pacific contributed $7.5 billion (up 41% YoY), and the Rest of World segment surged to $4.7 billion - a staggering 42% year-over-year increase. This is a company that has barely begun to monetize its international audience at rates approaching US levels.

What makes these numbers structurally important is the context of the broader digital advertising market. According to Precedence Research, global digital advertising spend stood at approximately $550 billion in 2023 and is projected to exceed $1.36 trillion by 2033, implying a CAGR of 9.58%. Meta does not need to take market share to grow - the pie itself is expanding at nearly double-digit rates as traditional advertising budgets continue their migration online. Yet Meta is simultaneously benefiting from both the expanding market and its own share gains through superior AI-driven ad targeting.

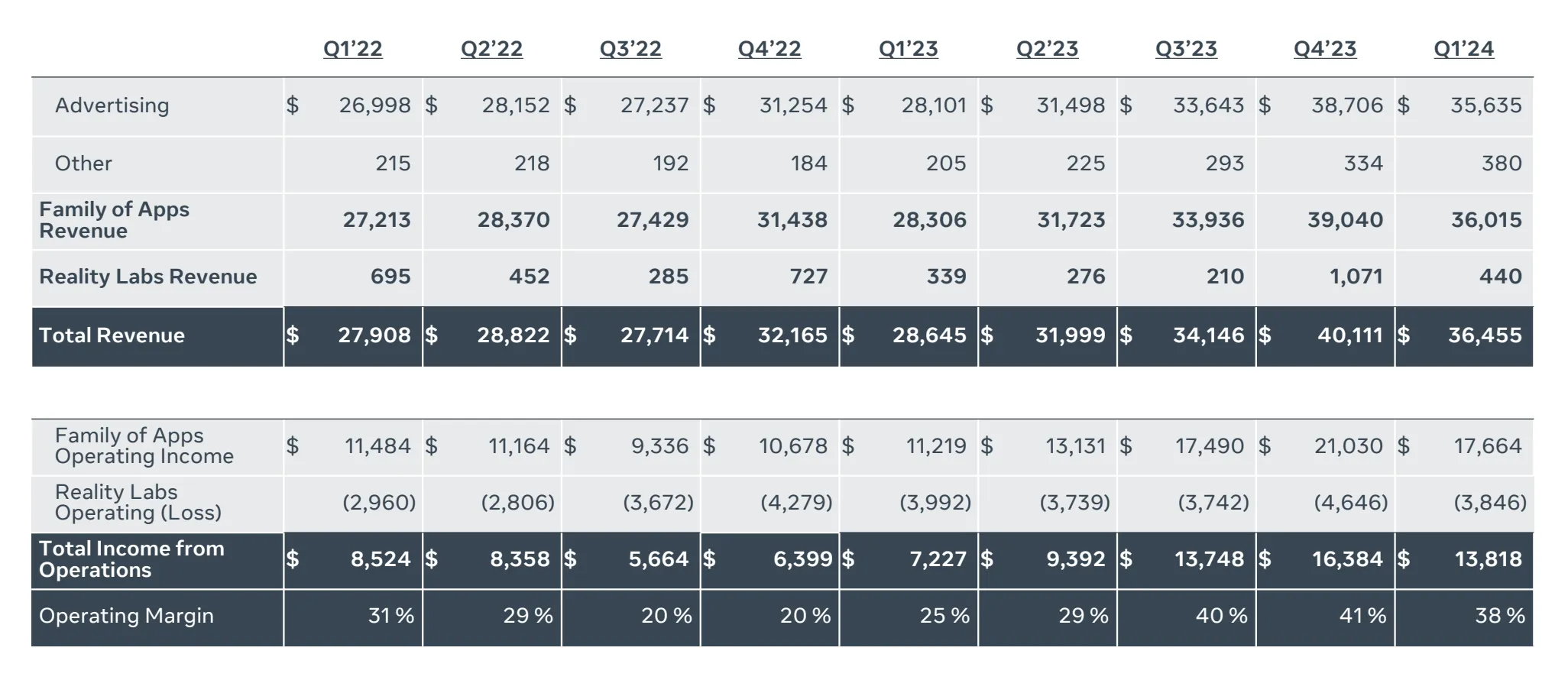

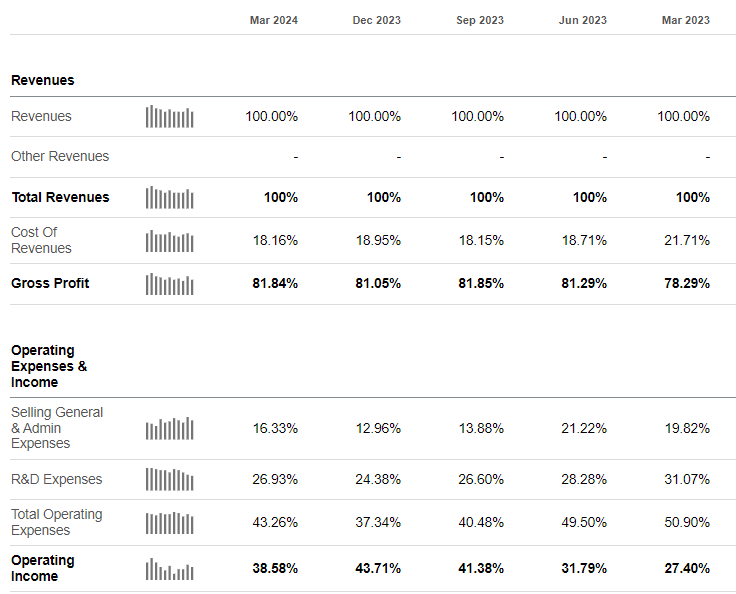

The segment-level data makes the core economics strikingly clear. Family of Apps - Facebook, Instagram, WhatsApp, and Messenger combined - generated $36 billion in revenue and $17.7 billion in operating income in Q1 2024, representing an operating margin of 49.2%. That is nearly 1,000 basis points of expansion year-over-year. This is not a company struggling to find profitability; it is a company whose core business is among the most profitable operations in the history of technology.

Advertising accounts for 97.8% of total revenue. Some analysts frame this as a concentration risk. We see it differently: it means Meta has a singular, obsessive focus on making its advertising platform as effective as possible for the millions of businesses that depend on it. And the results speak for themselves.

3.24 Billion People and Counting

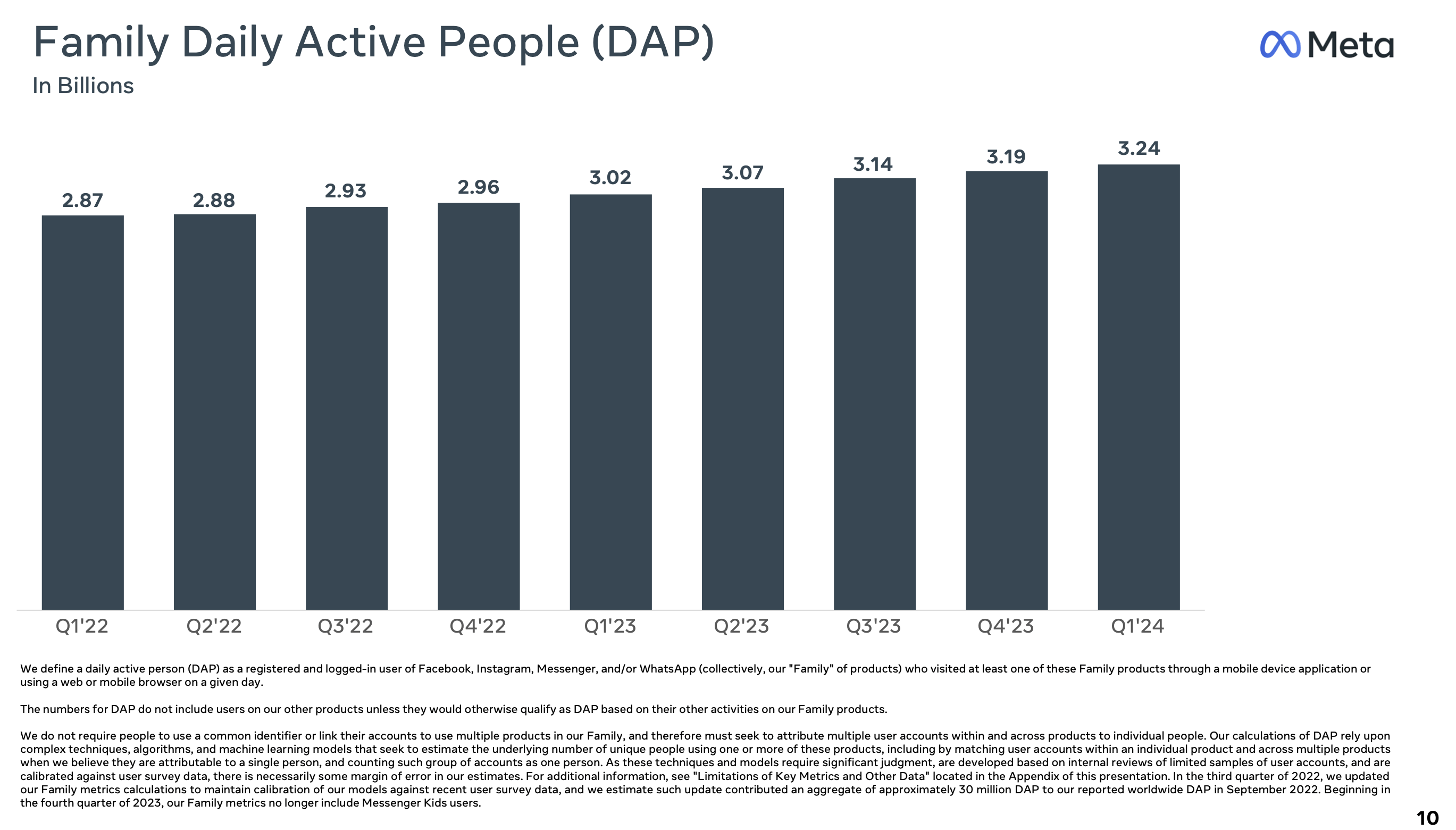

The moat around Meta’s business is not a technological secret or a patent portfolio. It is something far simpler and far more durable: 3.24 billion people use at least one Meta app every single day. That figure represents roughly 40% of the global population. There is no other company on Earth - not Google, not Apple, not Amazon - that commands this level of daily engagement with this many human beings.

What makes this metric even more remarkable is its trajectory. From Q1 2022 to Q1 2023, Meta added approximately 150 million daily active people. Over the subsequent twelve months, that number increased by 220 million - nearly 50% faster growth despite the already-massive base. The narrative that Meta’s platforms are “aging” or “losing relevance” simply does not survive contact with the data.

The competitive dynamic here is fundamentally different from what we see in cloud computing, search, or e-commerce, where the major big tech companies constantly encroach on each other’s territory. Microsoft can compete with Google in search. Amazon can compete with Microsoft in cloud. Google can compete with Amazon in advertising. But none of them can compete with Meta in social networking. The network effect is simply too powerful. Every person who joins makes the platform more valuable for every other person already there, creating a self-reinforcing cycle that no amount of engineering talent or capital can easily replicate.

No one has been able to break this dominance. Remember when Snapchat introduced Stories? Instagram adopted the feature, and Snapchat’s growth trajectory never recovered. When Twitter stumbled, Meta launched Threads - which accumulated 100 million users faster than any app in history. When Apple implemented its iOS privacy changes in 2022, Wall Street declared Meta’s ad business permanently impaired. Within eighteen months, Meta had rebuilt its measurement and targeting stack using AI, and revenue growth reaccelerated from near-zero to 27%.

There is one competitor that has genuinely challenged Meta: TikTok. ByteDance’s short-video platform captured a meaningful share of attention among younger demographics. But even here, the story is more nuanced than the headlines suggest. First, despite TikTok’s rise, Meta still managed to grow its daily active people by 370 million over two years. Second, and critically, President Biden signed a bill on April 24, 2024 that could potentially force TikTok to divest from its Chinese parent company or face a ban. Whether TikTok is ultimately banned, divested, or continues operating under increased scrutiny, the regulatory headwinds are real - and every point of uncertainty for TikTok is a potential tailwind for Instagram Reels.

Perhaps the most underappreciated aspect of Meta’s competitive position is its relationship with China. Unlike virtually every other mega-cap tech company, Meta has no operational dependency on China. Facebook and Instagram are already banned there - it cannot get worse. But Chinese companies like PDD Holdings (Temu), Shein, and Alibaba spend billions on Meta’s platforms advertising their products to Western consumers. Meta can do without China, but Chinese e-commerce companies cannot do without Meta if they want to reach the West. That is an asymmetry worth paying attention to.

Why Every Dollar of AI CapEx Is a Dollar Well Spent

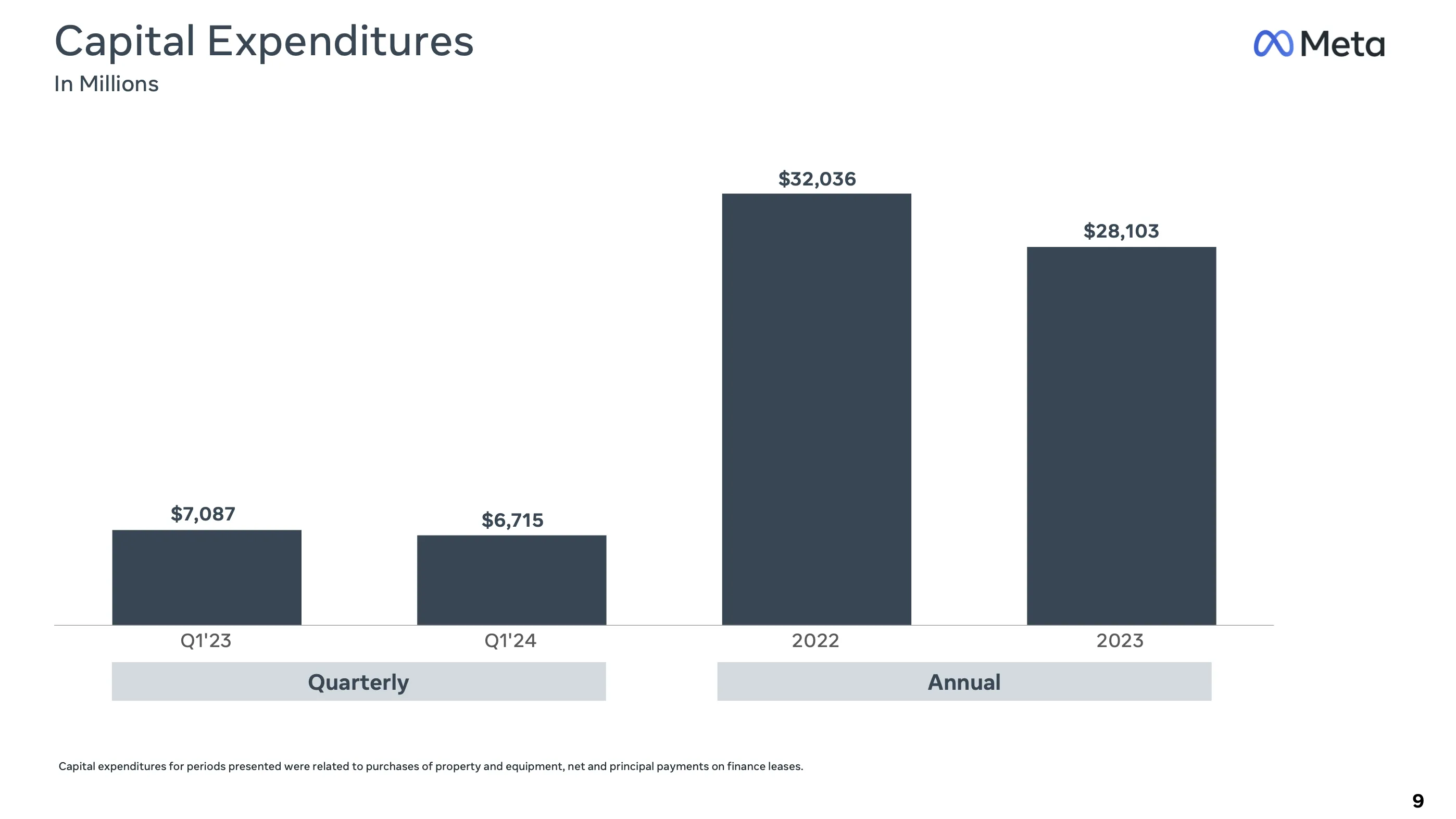

The post-earnings sell-off was driven by a single concern: CapEx is going up. Let us examine what that CapEx is actually buying.

Meta is investing in data centers, GPU clusters (predominantly Nvidia hardware), and the infrastructure required to train and deploy large language models at a scale that is genuinely unprecedented. Llama 3, released in mid-April 2024, has demonstrated performance that matches or exceeds Google’s Gemini Pro 1.0 and Mistral across key benchmarks. This is not a vanity project. This is a company building its own AI stack because the strategic implications of depending on OpenAI or Google for its core recommendation and advertising technology would be existential.

And here is what most investors are missing: the AI is already generating measurable returns.

The numbers Zuckerberg cited on the earnings call are worth unpacking carefully. Thirty percent of content on Facebook’s feed is now delivered by Meta’s AI recommendation system - up 2x over the past couple of years. On Instagram, that figure exceeds 50%. This means that AI is not some future promise at Meta; it is the engine running the core product today. Every improvement to the recommendation model translates directly into higher user engagement, which translates into more ad impressions, which translates into more revenue.

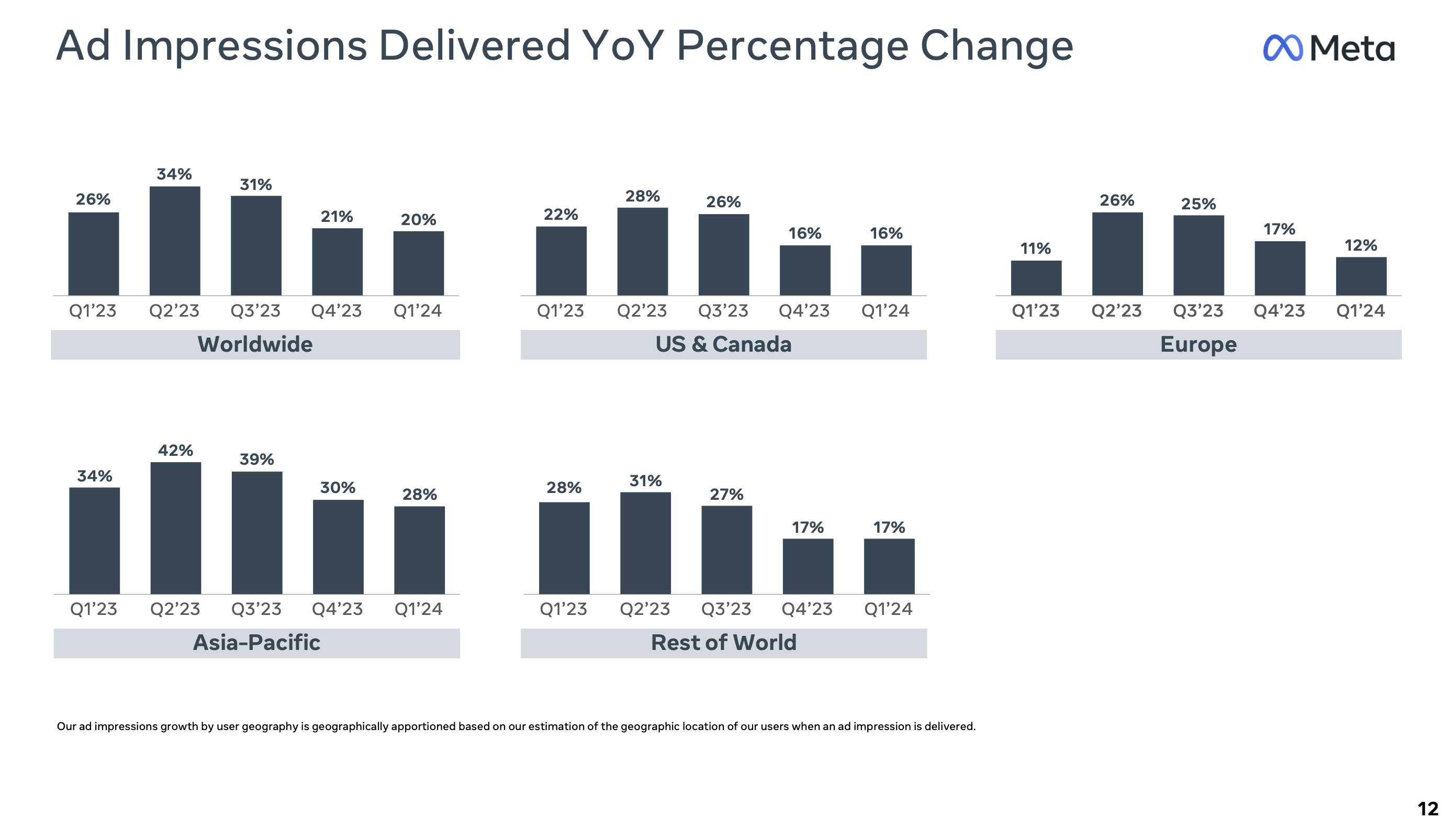

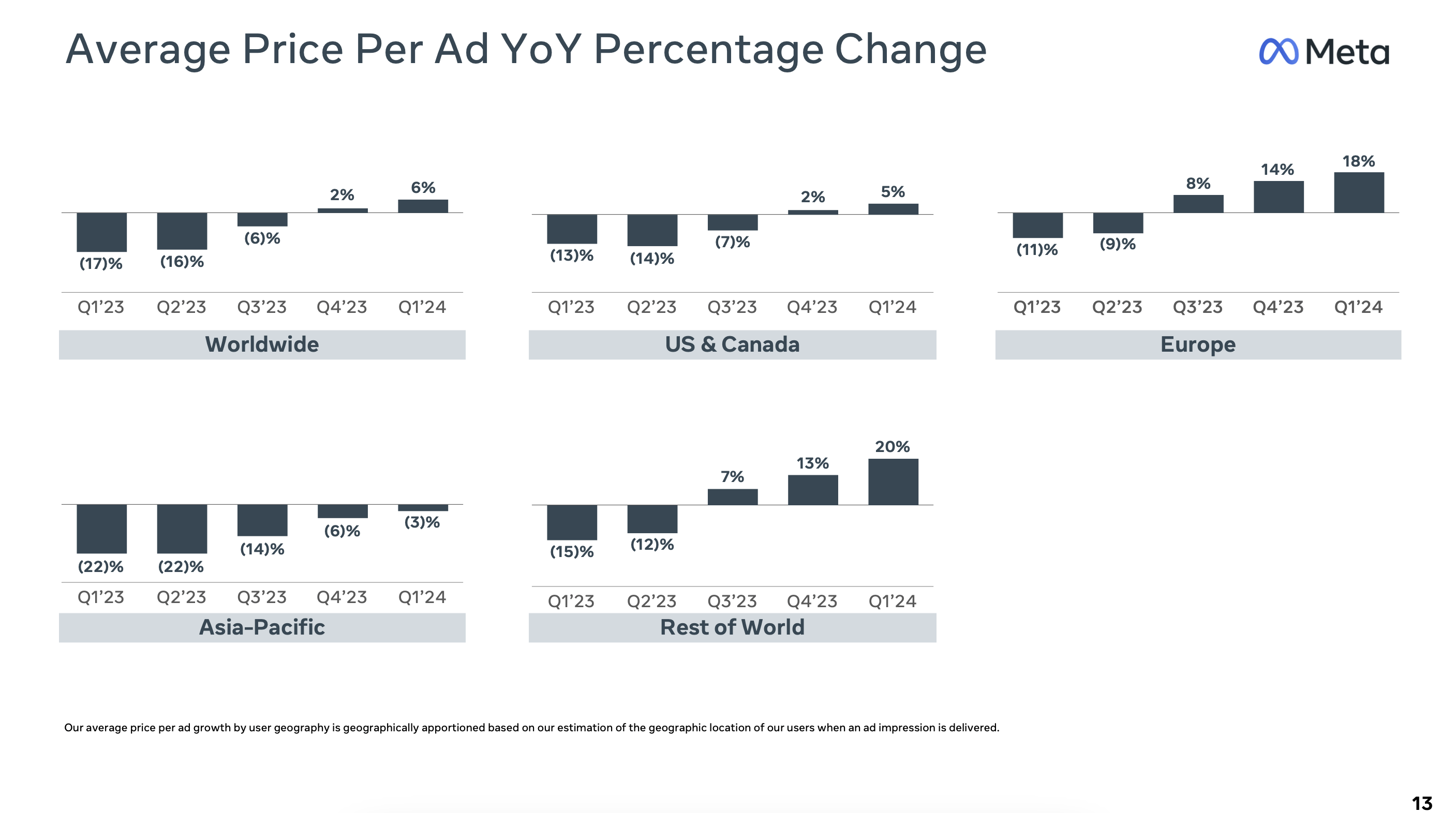

The ad impressions and pricing data paint a picture of a business that is firing on all cylinders. Ad impressions grew 20% worldwide, driven by AI-recommended content keeping users engaged longer. Simultaneously, average price per ad rose 6% globally - the first sustained increase after a multi-year period of declining ad prices that followed Apple’s iOS privacy changes. In the Rest of World segment, ad pricing surged 20% year-over-year, suggesting that Meta’s AI-powered ad targeting is making its international inventory dramatically more valuable to advertisers.

This is the flywheel that the market is underappreciating. AI investment improves content recommendations, which increases user engagement, which generates more ad impressions, which attracts more advertiser spend, which increases ad pricing, which generates more cash flow, which funds more AI investment. The CapEx is not a cost center - it is the fuel for this virtuous cycle.

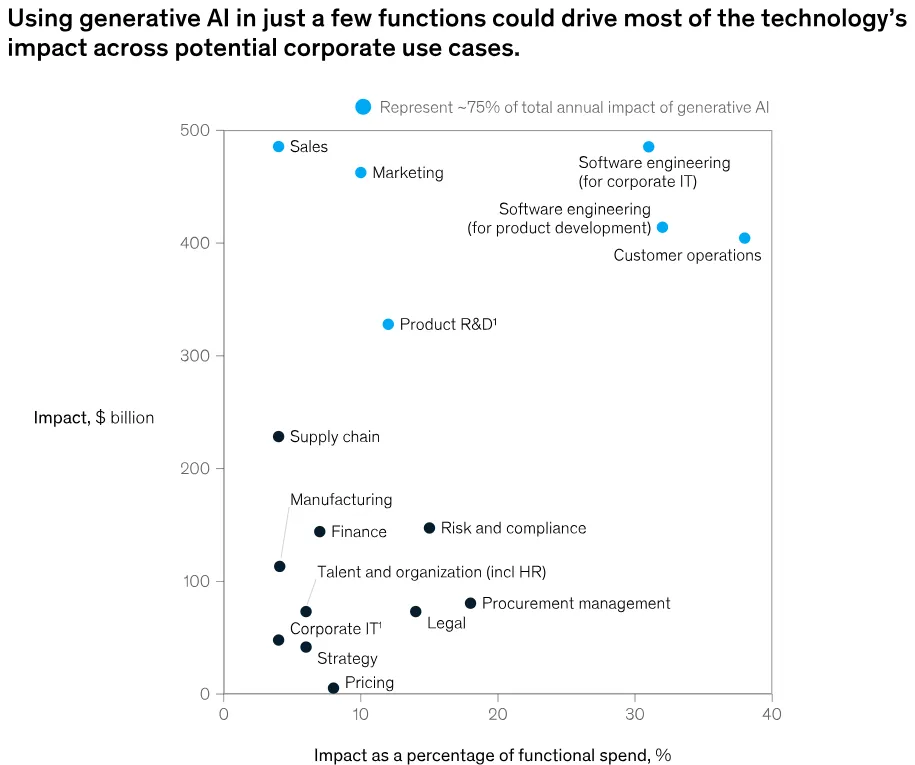

McKinsey’s analysis of generative AI’s economic impact adds an important structural dimension. The firm estimates that generative AI could bring trillions of dollars in annual economic benefits, with Sales and Marketing identified as the two single largest beneficiary functions. Meta is not just participating in the AI revolution - it is positioned at the exact intersection where the economic impact is expected to be greatest. According to Statista, the generative AI market is projected to grow at a CAGR of 46.5% between 2024 and 2030. For a company whose entire business model is selling advertising through AI-optimized content feeds, this secular tailwind could not be more directly relevant.

One analyst framed it well: “In the current environment of emerging AI capabilities, not investing in AI is much riskier than ramping up the company’s AI CapEx. Without investments in innovation, Meta might be disrupted by new technologies, which will likely significantly shorten the life cycle of the company’s business.” This is exactly right. The choice is not between spending $35 billion on CapEx and spending $25 billion. The choice is between spending to maintain and extend your competitive advantage, or becoming the next company that failed to invest during a technology transition.

The Three-Layer Thesis: Core, AI Integration & the Frontier Bet

The common critique of Meta - that it is “just an advertising company” while Microsoft, Alphabet, and Amazon have diversified into cloud, enterprise software, and e-commerce - misses a critical insight. Meta’s apparent lack of diversification is actually a strategic strength. The company has one obsessive focus: connecting three billion people and monetizing those connections. Every new capability - AI, AR/VR, commerce - feeds back into that same core engine.

Consider WhatsApp - the asset that was mocked as a $19 billion overpay a decade ago. With 2.78 billion monthly users, it is the dominant messaging platform outside the United States. Until recently, it generated essentially no revenue. That is changing. Click-to-message ads are expanding, allowing businesses to initiate conversations with potential customers directly through WhatsApp. More importantly, WhatsApp Pay is rolling out in markets like India and Brazil, enabling merchants and small businesses to sell products within the app without relying on external sites. This gives Meta control over the entire purchasing process - from ad impression to final payment.

The Zuckerberg vision, though never publicly stated in quite these terms, appears to be building a Western equivalent of Tencent’s WeChat - a super-app where you can shop, pay, communicate, consume content, and eventually interact through AR/VR, all within Meta’s ecosystem. Whether that vision fully materializes or not, the intermediate steps - WhatsApp monetization, Meta AI as a virtual assistant, Advantage+ advertising tools - are each individually valuable and already generating returns.

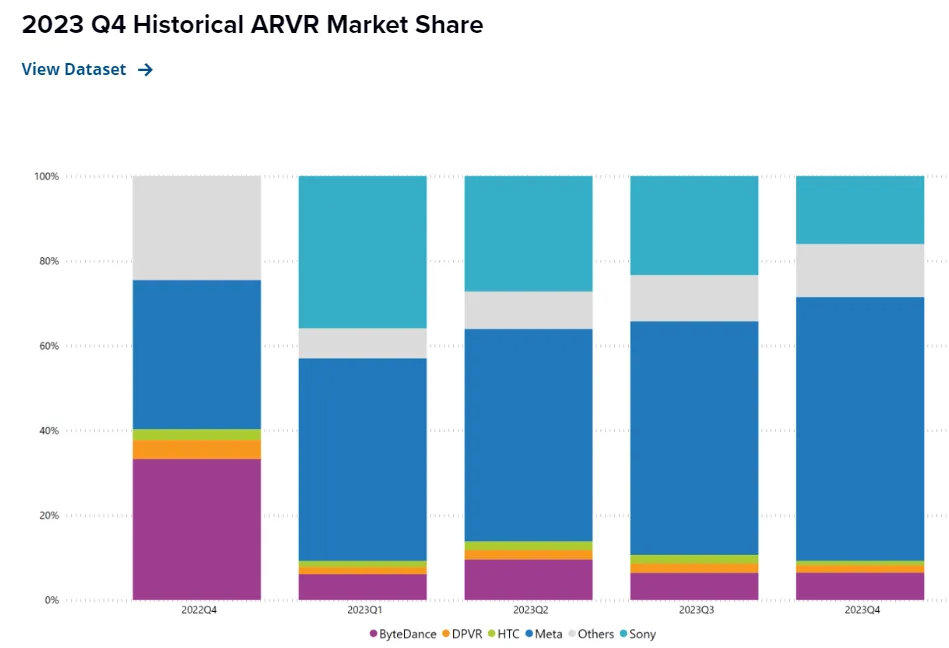

On Reality Labs: we maintain a nuanced view. The segment lost $3.8 billion in Q1 2024, and cumulative losses since its inception are approaching $50 billion. That is real money. But Meta is the undisputed market leader in AR/VR, with approximately 70% market share in headset shipments. Apple’s Vision Pro, launched at $3,500, generated lukewarm reception. There is no other company willing to invest at the scale Meta is committing to this category.

The honest assessment is this: Reality Labs is a call option on the next computing platform. It may ultimately prove transformative - or it may prove to be an expensive misstep. But at the current share price, investors are not paying for Reality Labs. If we strip out the $3.8 billion quarterly loss and value Family of Apps alone at $17.7 billion operating income (which annualizes to approximately $25 in EPS), the core business at 23x earnings is already worth more than the current stock price. Everything Reality Labs eventually delivers is upside the market is getting for free.

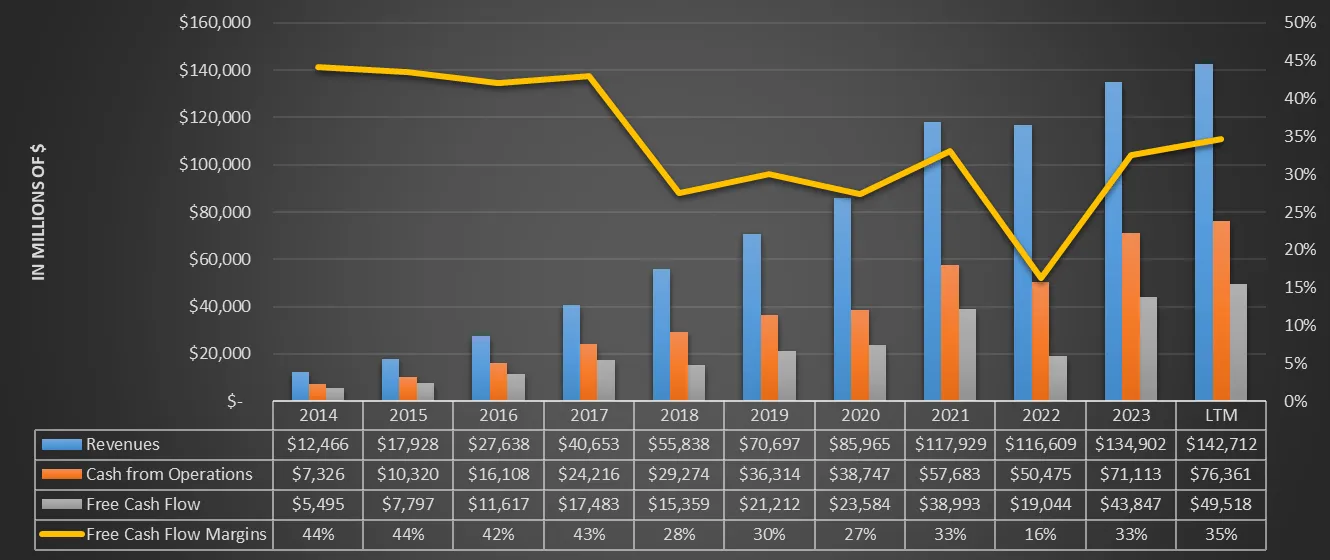

$49 Billion in Free Cash Flow and a Bulletproof Balance Sheet

The financial profile of Meta Platforms in mid-2024 is, by any historical standard, extraordinary.

From $12.5 billion in revenue in 2014 to $143 billion trailing twelve months in Q1 2024, Meta’s growth has compounded at rates that should be structurally impossible for a company of this size. The 10-year free cash flow CAGR stands at 31.1%. The current FCF margin of 35% is robust, but importantly, it could be significantly higher if Meta chose to reduce CapEx - which it could do at any time by simply scaling back Reality Labs and AI infrastructure investment.

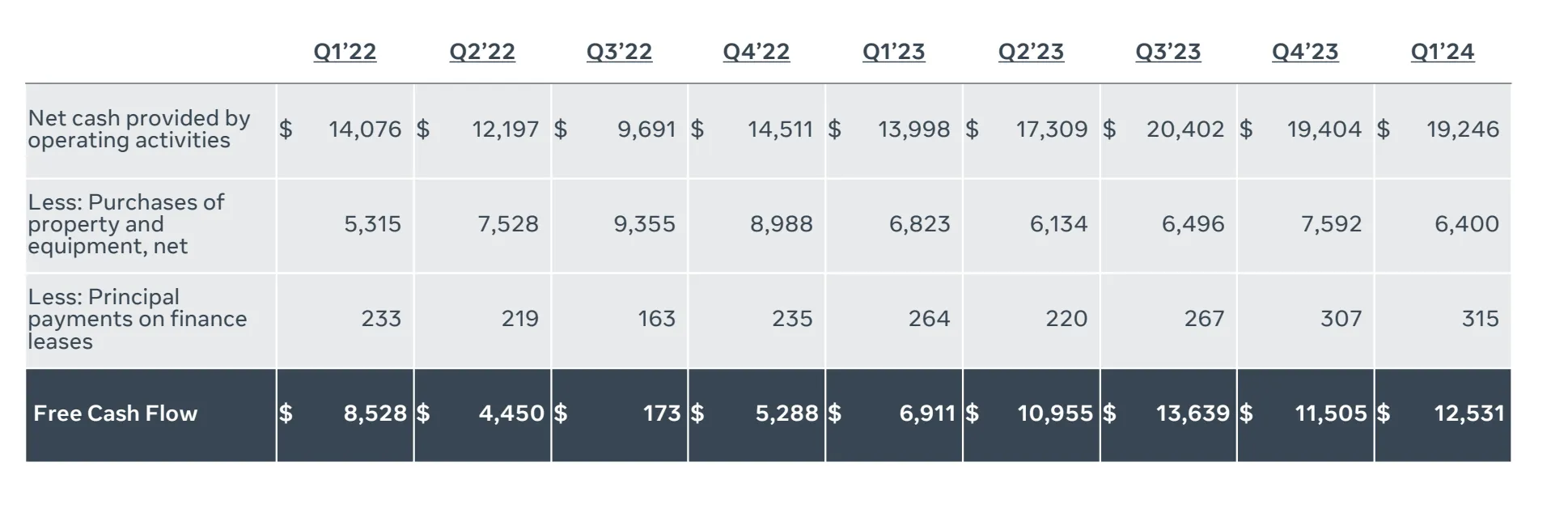

The Q3 2022 figure deserves attention. Free cash flow collapsed to just $173 million that quarter as the company simultaneously dealt with Apple’s privacy changes, a global digital advertising recession, and the peak of its Reality Labs spending spree. The stock touched $88. Eighteen months later, FCF stood at $12.5 billion per quarter and the stock was approaching $500. The resilience of Meta’s business model - its ability to absorb massive external shocks and bounce back stronger - is a competitive advantage that does not appear in any DCF model but is worth paying for.

The balance sheet provides further comfort. Meta holds $58 billion in cash and short-term investments against $18.4 billion in debt, giving it approximately $40 billion in net cash (after netting long-term debt obligations against $58B gross cash and investments on the balance sheet) - roughly 3% of its market capitalization. This is a company that could fund its entire $35–$40 billion CapEx program from operating cash flow, return $20 billion to shareholders through buybacks and dividends, and still add to its cash position.

Speaking of shareholder returns: Meta spent $14.6 billion on share repurchases and $1.3 billion on dividends in Q1 alone, for a combined $15.9 billion in total returns to shareholders. That pace - roughly $64 billion annualized - exceeds the company’s GAAP net income. Meta has a $50 billion authorized buyback program and a newly initiated quarterly dividend of approximately $0.50 per share ($5.2 billion annualized), representing about 10% of free cash flow. The buyback model that has worked so well for Apple’s stock price over the past decade is now being applied by Meta.

The “Rule of 40” framework - where a company’s revenue growth rate plus operating margin should exceed 40% - is typically applied to high-growth SaaS businesses. Meta’s Q1 score: 65% (27% revenue growth plus 38% operating margin). That places it in the stratosphere of business quality, rivaling or exceeding companies a fraction of its size that trade at far higher multiples.

Six Lenses on Value: Why 21x Earnings Is Too Cheap

At approximately $480 per share following the post-earnings dip, Meta trades at roughly 21x consensus FY25 earnings of $23.08. For a company growing revenue at 27%, generating $49 billion in free cash flow, and deploying AI across 3.24 billion daily users, this multiple is difficult to justify as “fully valued.”

We synthesized seven independent valuation frameworks from the research we reviewed. They converge on a range that is meaningfully above the current price.

| Framework | Method | Implied Value | Key Assumption |

|---|---|---|---|

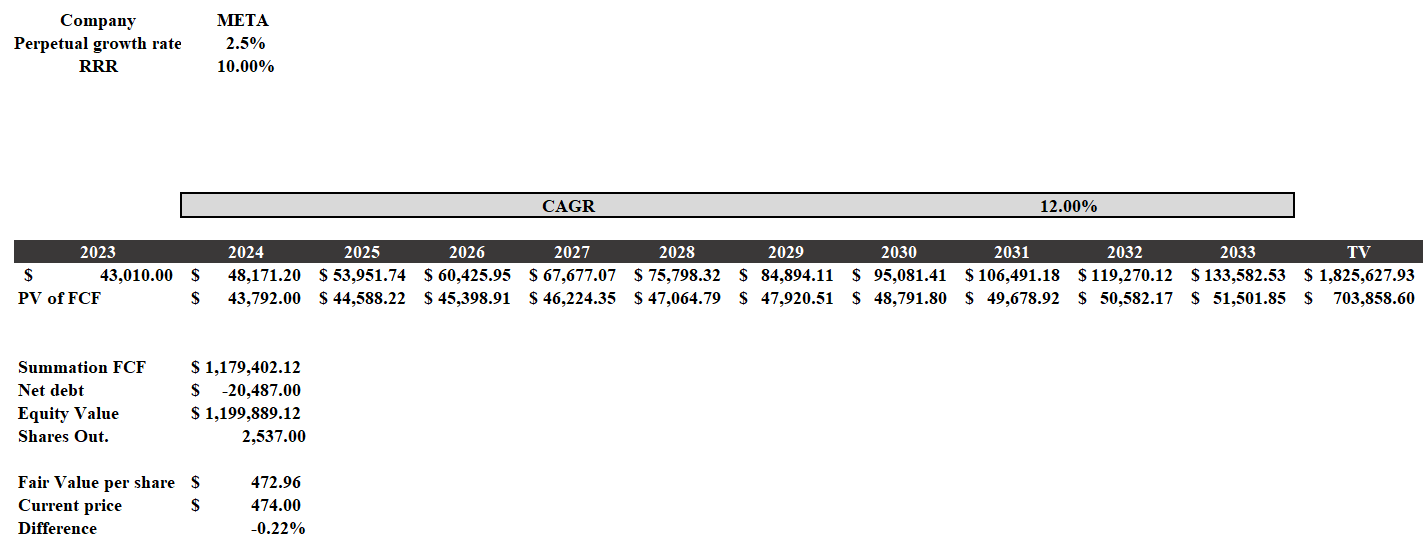

| Conservative DCF | 12% FCF CAGR, 10% RRR | $473 | Below 10-year FCF CAGR of 31%. Floor scenario. |

| Moderate DCF | 8.8% WACC, 5% terminal growth | $567 | 100bps annual FCF margin expansion. Conservative. |

| FoA Strip-Out | $25 FoA EPS × 23x + net cash | $590+ | Values Reality Labs at $0. Core business alone. |

| PEG Ratio | 0.6x PEG using 36% EPS growth | Deeply Undervalued | PEG below 1.0x is textbook “cheap for growth.” |

| MSFT Parity | P/S convergence to MSFT’s 12.55x | ~$810 | If market values Meta’s AI at MSFT’s multiple. |

| Quality Premium | 30x FoA earnings + net cash | $750+ | Applies Apple-like quality multiple to FoA stream. |

The conservative DCF arrives at approximately $473 per share using a 12% free cash flow CAGR through 2033 - well below Meta’s actual 10-year FCF CAGR of 31.1% - with a 10% required rate of return. This can reasonably be considered a floor valuation that does not credit the company for any AI-driven revenue acceleration.

A more realistic DCF using an 8.8% WACC, 100 basis points of annual FCF margin expansion, and consensus revenue projections yields a fair value of approximately $567 - a 20% premium to the current price. This model assumes FY25 revenue growth of 12.9% (in line with Wall Street consensus) and gradual deceleration thereafter. It does not assume any new revenue streams from WhatsApp monetization, AI-powered business messaging, or AR/VR.

Perhaps the most compelling framework is the Family of Apps strip-out. If we value Reality Labs at precisely $0 - treating every dollar invested there as money set on fire - the core Family of Apps business generates approximately $25 in annual EPS. At the market’s current 23x earnings multiple, that business alone is worth roughly $575. Add approximately $40 billion in net cash (after netting $18.4B in long-term debt against $58B gross cash and investments on the balance sheet - approximately $15.75 per share) and you arrive at $590+ without assigning any value whatsoever to Meta’s AI moonshots, VR leadership, or WhatsApp monetization.

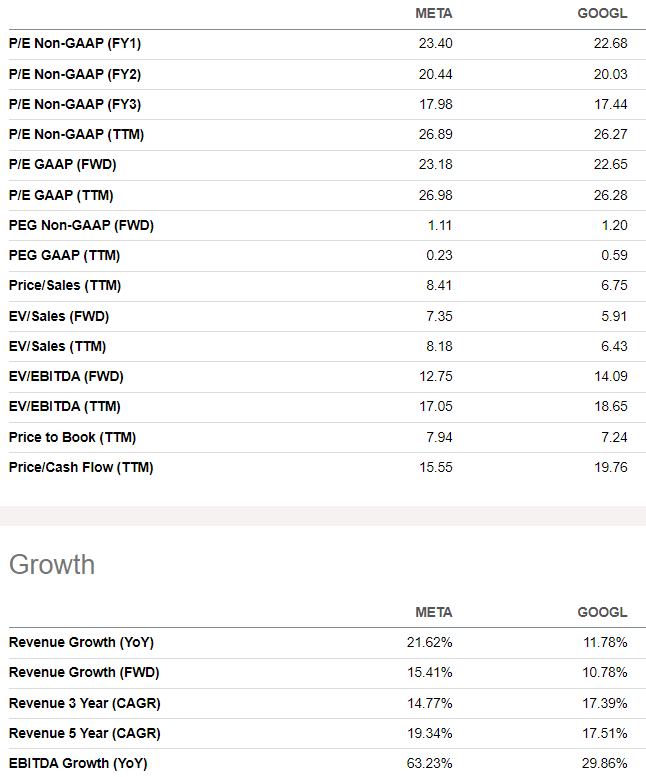

The PEG ratio provides additional context. Using the current year’s projected 36% EPS growth as the denominator, Meta’s PEG ratio stands at just 0.6x. Anything below 1.0x is traditionally considered undervalued for the growth being delivered. Meta’s PEG is well below 1.0x and below Alphabet’s 1.2x - despite Meta demonstrating faster revenue growth (21.6% vs. 11.8%).

The Amazon Moat: Why the CapEx Bears Are Making a Familiar Mistake

Wall Street’s discomfort with Meta’s increased spending echoes a pattern we have seen before. In the 2000s and early 2010s, Amazon consistently chose to invest operating income back into the business - building fulfillment centers, launching AWS, expanding Prime - at the expense of near-term profitability. Analysts were perpetually frustrated that the company “could not” show earnings. What they missed was that Amazon was building compounding competitive advantages that would eventually produce operating income that dwarfed anything the bears imagined.

Amazon’s stock is up 10x since 2015, when operating income finally began inflecting sharply higher. The bears had been right about earnings compression, but catastrophically wrong about enterprise value creation.

We see striking parallels in Meta’s current setup. The ability - and willingness - to invest enormous amounts of capital in a potentially high-ROI opportunity like AI is itself a competitive moat. Not every company can afford to invest $35–$40 billion annually in infrastructure while simultaneously buying back 5% of its shares, paying a dividend, and adding to its cash position. Meta can because its core advertising business throws off nearly $50 billion in annual free cash flow. This is the “Amazon Moat”: the capacity to invest at scale in competitive advantages that smaller players simply cannot match.

The context here is important. Just two years ago, Meta was facing genuine existential questions. TikTok was eating into Instagram’s engagement among younger users. Apple’s privacy changes had kneecapped ad targeting. The stock fell 77% from its peak. Zuckerberg responded with the “Year of Efficiency” - cutting headcount by 21,000, flattening management layers, and fundamentally restructuring the company’s cost base. That restructuring is now baked in. The efficiency gains are permanent. And the company is deploying those savings not into shareholder distributions (though it is doing that too) but into AI infrastructure that is already proving its value.

Recall that Meta’s ROIC (return on invested capital) has been historically exceptional, consistently among the highest of any mega-cap technology company. This is a management team that has demonstrated the ability to invest capital at very high rates of return. When such a team signals they see an opportunity to invest more, the empirically sound response is to follow the money, not to second-guess it because it temporarily compresses margins.

What Could Go Wrong: An Honest Assessment

No thesis is without risk, and Meta’s risk profile deserves candid examination. The bear case has legitimate elements that require ongoing monitoring.

There is another risk that is frequently overlooked: the social media industry itself could face structural headwinds from regulation. Multiple research studies have documented the negative effects of prolonged social media use on mental health, particularly among younger users. Governments may eventually impose usage restrictions, age verification requirements, or content mandates that reduce engagement. With due respect to the seriousness of the issue, the parallel to tobacco regulation in the mid-20th century - when everyone knew cigarettes were harmful and addictive, but almost everyone smoked anyway - is uncomfortably apt. Social media use has become deeply ingrained in global culture, with average daily usage increasing from 90 minutes in 2012 to 2.5 hours in 2023. Whether regulation can meaningfully reverse this trend is an open question, but it is a risk that long-term investors should monitor.

The Trade: Scenario Analysis & Execution Framework

The following scenarios reflect the author’s personal analysis and are not investment recommendations. See our full disclaimer.

Catalyst Timeline: Q2 2024 – Q2 2025

The Author’s View: What Seven Perspectives Taught Us About Meta

We began this analysis with a simple question: is the market right to punish Meta for investing in AI? After synthesizing seven independent research perspectives and the full Q1 2024 earnings call, we believe the answer is unequivocally no.

Each source we reviewed approached Meta from a different angle, yet they converge on a strikingly similar conclusion. The first perspective highlighted the raw financial power - $36.5 billion in quarterly revenue, $50 billion in annualized FCF, a 5% FCF yield despite $30 billion in annual CapEx. The second revealed what we believe is Meta’s most underappreciated advantage: it occupies a competitive lane that no other big tech company can contest, insulated from China dependency, immune to the cloud wars, and defended by a network effect that spans 40% of humanity. The third demonstrated that the post-earnings dip is a classic case of Wall Street short-termism - punishing a Rule-of-40 score of 65% because CapEx guidance increased by $5 billion.

The fourth and fifth perspectives connected Meta’s AI strategy to concrete economic data - the McKinsey framework showing Sales and Marketing as the primary beneficiaries of generative AI, the DCF models converging on $470–$570 fair value even under conservative assumptions. The sixth applied the Amazon historical parallel: a company generating enormous cash flow that chooses to invest it in competitive advantages rather than return it all to shareholders, and a market that punishes it for the decision - until, inevitably, it doesn’t.

And throughout all of it, the earnings call transcript provided the connective tissue. Zuckerberg’s commentary was remarkably clear: the AI is working, it is generating measurable revenue gains, and he intends to invest more because the returns justify it. This is not a CEO chasing a fad. This is a founder with 61% voting control who survived a near-death experience in 2022, restructured his company from the ground up, and is now deploying capital into the highest-ROI opportunity he’s seen since the original Facebook mobile transition.

Here is what we find most compelling: even if you assign zero value to Reality Labs, zero value to WhatsApp monetization, zero value to Meta AI as a standalone product, and zero value to the potential TikTok competitive tailwind - even if you strip away every speculative element and value only the advertising business that exists today - the core Family of Apps is generating approximately $25 in annual EPS at a 49% operating margin. At 23x earnings, that business alone is worth $575. The stock is trading at $480.

The market is offering you the most powerful advertising machine in history, growing at 27%, throwing off $50 billion in cash, led by a founder with a proven ability to adapt and scale - and it is pricing in near-zero optionality for AI, WhatsApp, AR/VR, and the international ARPU convergence that is already underway. We believe this is a mispricing, and we believe the $620–$660 target zone is achievable within a 6–12 month horizon as the quarterly data confirms that the AI CapEx flywheel is turning into revenue.

Warren Buffett famously said that it is far better to buy a wonderful company at a fair price than a fair company at a wonderful price. Meta is a wonderful company. And at $470–$490, the price is more than fair.

- PolyMarkets Investment Strategies Research

Important Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. Past performance does not guarantee future results. All investments carry risk, including the possible loss of principal. Meta Platforms, Inc. (NASDAQ: META) is subject to regulatory risk (EU Digital Services Act, GDPR, US antitrust), governance concentration risk (dual-class share structure), advertising market cyclicality, competitive risk from TikTok and emerging platforms, AI investment ROI uncertainty, and ongoing Reality Labs cash burn. The company generates virtually all revenue from digital advertising, making it sensitive to economic cycles and shifts in advertiser spending. The valuation frameworks presented rely on publicly available information and independent analytical models as of June 2024; actual results may differ materially. Mark Zuckerberg’s controlling stake means strategic direction cannot be changed by minority shareholders. Always conduct your own due diligence and consult a qualified financial advisor before making any investment decision.