There is a pattern that repeats itself in commodity markets, reliably and almost boringly. A great company hits a rough patch - costs run higher than expected, a legal overhang clouds the outlook, China disappoints - and the market, which has a very short memory and an even shorter temper, marks the stock down to a price that implies things will stay broken forever. Then the company quietly fixes the problem, and the stock has nowhere to go but up.

That is precisely where Vale stands in December 2025. The world's largest iron ore producer is trading near multi-year lows while its direct production cost per tonne just came in at $20.7 - below its own guidance midpoint and sitting competitively between BHP and Rio Tinto. Free cash flow for the first nine months of 2025 reached $4.08 billion. The legacy dam disaster provisions are ~75% settled, with a clearly mapped schedule for what remains. And a US-China tariff truce, combined with classic Lunar New Year restocking, is providing near-term support to iron ore prices just when sentiment was at its darkest.

The market is pricing Vale as though the cost problem is permanent, China is in structural free-fall, and the dam liabilities are open-ended. We think all three of those assumptions are wrong - and the entry zone of $12–$14 offers a meaningful margin of safety, though the degree varies significantly with entry price. The base-case DCF produces an intrinsic value of $13.83 - effectively the ceiling of the range. Entry at $12.00–$12.50 provides a genuine 10-13% discount to that base case - the strongest risk/reward zone. Entry at $13.50–$14.00 approaches or reaches the DCF base case, with upside coming primarily from the bull scenario ($100+ iron ore) rather than from a valuation discount. We recommend sizing the initial position at the lower end of the range and reserving dry powder to add if the stock tests $12–$12.50.

Vale at a Glance

Vale S.A. is the world's largest producer of iron ore - the essential raw material for steel - and one of the world's largest producers of nickel, a critical metal for electric vehicle batteries and stainless steel. Based in Rio de Janeiro, Brazil, Vale operates across more than 30 countries and ships to customers on every continent, with China representing approximately 60% of its revenues. Its Carajás complex in the Amazon is the single largest iron ore mine on earth.

Vale is, in almost every measurable sense, a company that operates at world scale. Its challenge has never been the quality of its assets - those are among the finest in the global mining industry. Its challenge has been the market's perception of its operational reliability, its legacy legal exposures, and its sensitivity to a Chinese economy that has been stubbornly reluctant to recover at pace. At $12–$14 per share, each of those concerns is reflected - and then some.

The Cost Story - Vale's Most Important Fix

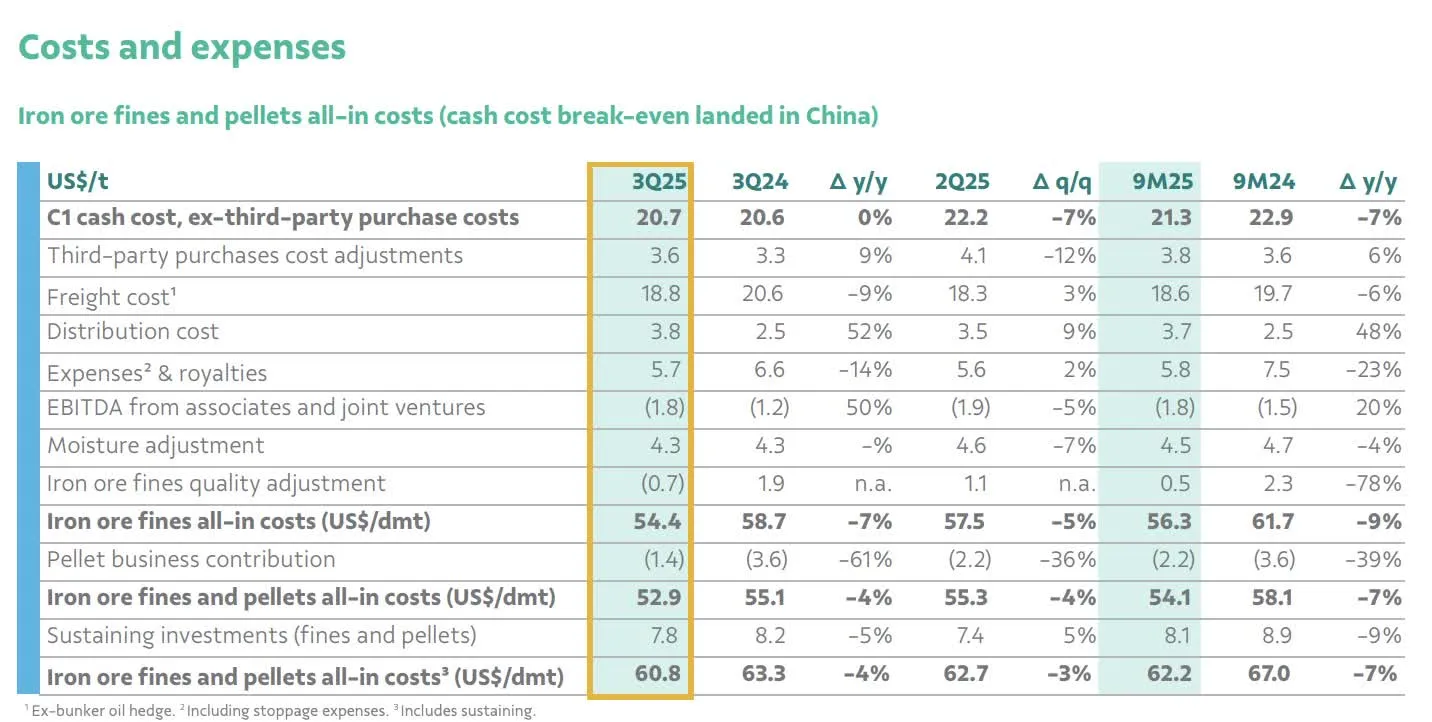

If you want to understand why Vale's stock has been under pressure for the past two years, you don't need to look at iron ore prices or China demand statistics. You need to look at one number: C1/t - the direct cost to produce one metric tonne of iron ore, excluding freight and third-party purchases. This is the number the market watches most carefully, because it's the one variable that Vale actually controls. And for a while, it was going in the wrong direction.

Rainfall disruptions, logistical bottlenecks, inventory timing issues and maintenance cycles pushed C1/t higher than guidance in several quarters - and the market responded by re-pricing the stock as if this were a permanent structural problem rather than an operational wobble. The skepticism became self-reinforcing: every guidance miss confirmed the bear narrative.

Then Q3 2025 arrived, and the picture changed materially. C1/t came in at $20.7 per tonne - a drop of 6.8% quarter-on-quarter, flat year-on-year, and below what most analysts had modelled. The full-year 2025 guidance of $20.5–$22.0/t, which had looked aspirational just two quarters ago, now looks not just achievable but potentially beatable. That single result broke the most important structural argument against Vale: that management had lost control of its cost base.

| Producer | C1 Cost (Q3 2025) | Relative Position | Cost Bar |

|---|---|---|---|

| BHP (Pilbara, FY2025) | $17.29/t | Lowest cost - premium Pilbara location | |

| Vale (Q3 2025) | $20.7/t | Mid-range - solid given logistics complexity | |

| Rio Tinto (Pilbara, 1H 2025) | $24.3/t | Highest of the three major producers |

Vale's position between BHP and Rio Tinto is actually stronger than it looks on paper, because Vale's ore comes from Brazil's Amazon basin - with higher moisture content, more complex logistics, and greater seasonal variability than the Australian Pilbara operations. The fact that Vale can compete at $20.7/t under those conditions speaks to the efficiency of the S11D complex and the ongoing operational improvement programme.

Beyond iron ore, the cost picture in Vale's other metals divisions is also improving. Copper all-in costs fell 17% year-on-year in 2025, partly because the rising gold price is providing a significant by-product credit. Nickel all-in cost guidance was revised down approximately 7%, reflecting a more efficient operation - a meaningful positive given how much the market has worried about Vale's nickel business in a period of weak nickel prices.

"When C1/t converges to the lower end of guidance, every dollar of iron ore price becomes more margin. The trend we're seeing isn't seasonal - it's structural cost improvement. That's a valuation multiplier the market hasn't fully re-priced yet."

- Analyst commentary, Q3 2025 results reviewIron Ore: Near-Term Tailwinds, Medium-Term Realism

Iron ore is currently trading around $103.5 per tonne, up from approximately $92 in July 2025. That recovery reflects two overlapping forces - one geopolitical and one seasonal - that are providing a genuine, if temporary, lift to prices and to sentiment around Vale.

The US-China Tariff Truce

In late October 2025, the US and China announced a one-year trade agreement that reduced average tariffs to 47% - a 10 percentage point reduction from the previous level - and included the temporary removal of restrictions on exports of rare earth metals. For Vale and the broader commodity complex, this matters in two ways: it reduces trade uncertainty that had been freezing Chinese industrial investment plans, and it triggers a repricing of risk for emerging market exporters like Vale, increasing the flow of foreign capital into Brazilian assets.

Seasonal Restocking and the Monsoon Effect

The Lunar New Year cycle is one of the most reliable seasonal patterns in iron ore markets. Between November and January, Chinese steel mills systematically increase their ore purchases to build inventory before the holiday. This pattern has recurred for over a decade and is well-documented in the data - it is not a surprise, but it is real. Simultaneously, Brazil's monsoon season reduces shipments from Vale's northern ports, creating supply-side pressure on futures. The DCE January 2026 contract was already trading at approximately $110/t - a 3% premium to spot - reflecting this anticipated seasonal tightness.

We want to be honest about what comes after: the medium-term picture for iron ore in 2026 is less supportive. Chinese steelmakers' hot-rolled coil margins had fallen to breakeven levels by late 2025. China's Fixed Asset Investment in the first nine months of the year turned negative year-on-year for the first time in recent memory, largely driven by a real estate sector still contracting at -9% to -10% annually. Real estate consumes roughly 30–40% of China's iron ore demand. None of that resolves quickly.

But here is the key insight for this trade: Vale doesn't need iron ore to boom for this thesis to work. With C1/t at $20.7 and iron ore holding even at $85–$90/t - a scenario more pessimistic than current consensus - Vale still generates meaningful free cash flow and sustains a dividend yield of 6–8%. The upside scenario is simply additional leverage to iron ore holding at $100+.

Beyond Iron: Copper, Nickel & the Energy Transition

The market's mental model of Vale is almost entirely built around iron ore and China. That framing is understandable - iron ore is still the dominant earnings driver - but it increasingly misses an important part of the story. Vale is quietly becoming a meaningful player in the metals that the energy transition requires, and those businesses are growing while the market's attention is focused elsewhere.

Copper: A Structurally Attractive Business Getting Better

Vale's copper operations saw all-in costs fall 17% year-on-year in 2025, a dramatic improvement driven in part by rising gold by-product credits. Gold has been on a strong run globally, and for Vale's copper mines, which produce gold as a secondary product, every dollar that gold rises reduces the net reported cost of producing copper. This creates an unusual dynamic: Vale's copper business benefits simultaneously from strong gold prices and any recovery in base metals sentiment.

Copper's longer-term fundamentals are among the most compelling in the entire commodities universe. The electrification of transport, the build-out of renewable energy infrastructure, and the explosion of data centre construction are all structurally copper-intensive. Vale's copper exposure - through its Salobo mine in Brazil and its Sudbury operations in Canada - provides a meaningful and growing hedge against any sustained iron ore weakness.

India: The Emerging Offset to China

Perhaps the most underappreciated element of Vale's medium-term story is India. Vale's CEO has stated publicly that India's steel production capacity could double over the next five to seven years - a projection consistent with India's ambitious infrastructure and manufacturing expansion programmes. While China will remain Vale's dominant customer for the foreseeable future (accounting for ~60% of revenues), India represents a genuine growth engine that could absorb meaningful additional production volumes at good prices. This diversification of the customer base is a structural positive that the market has largely ignored.

Brumadinho & Samarco: The Cloud That's Clearing

No analysis of Vale can ignore the dam disasters. The 2015 Samarco collapse and the 2019 Brumadinho disaster were among the worst environmental catastrophes in Brazil's history, causing enormous loss of life and damage, and generating legal and financial liabilities that have weighed on Vale's balance sheet and investor sentiment for years. It is right that they should. But the picture in late 2025 looks materially different from even twelve months ago, and we think the market is still pricing in the uncertainty of 2021 rather than the visibility of 2025.

Here are the facts as they stand. Since 2019, Vale has paid out approximately $7.8 billion for Brumadinho and the equivalent of roughly $14 billion for Samarco. Of the total provisions ever established for both disasters, approximately 75% has already been paid. The remaining provisions on the balance sheet as of Q3 2025 stand at $4.2 billion - a number that, while still significant, is manageable relative to Vale's cash generation capacity.

The forward cash-out schedule is now clearly mapped. In 2026, approximately $1.3 billion is expected to flow out. In 2027, approximately $1.1 billion. From 2028 onward, annual obligations fall to a range of $0.5–$1.4 billion per year - a level that Vale can absorb without materially impacting dividends or growth investment. This is not resolution, but it is a clear trajectory toward resolution. The open-ended fear that dominated the narrative two years ago has been replaced by a quantified, scheduled liability.

The Extraordinary Dividend Trigger

Vale's net expanded debt stood at $16.6 billion in Q3 2025, down 5% year-on-year. Under Vale's capital allocation framework, when net expanded debt falls below $15 billion, the company is obligated to distribute extraordinary dividends above its regular programme. With the dam liability schedule now clearly mapped and FCF remaining strong, that $15 billion threshold is moving closer - creating a potential catalyst for a significant special dividend payment that is not currently priced into the stock.

Free Cash Flow & Dividend: The Real Story

The most important number in the Vale investment case right now isn't the iron ore price or the P/E ratio. It's the FCF yield. At a stock price of $12–$14, Vale is generating free cash flow at a rate that implies a yield of approximately 14% on 2025 estimates - one of the highest FCF yields of any major mining company globally. Even under a conservative iron ore scenario for 2026, that yield remains strongly positive.

Bear Scenario

Base Scenario

Bull Scenario

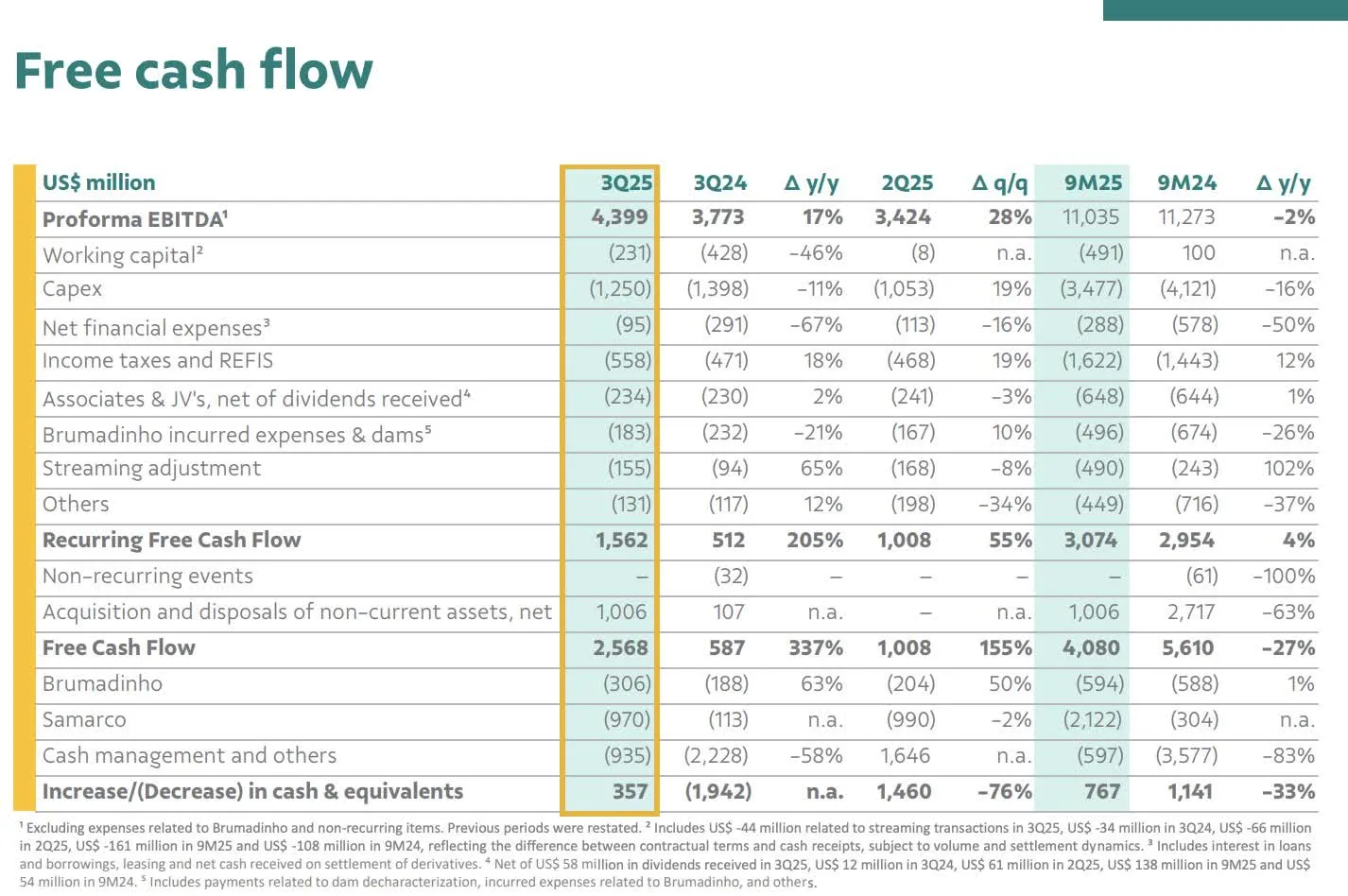

To understand what those numbers mean in practice: Vale generated $2.58 billion in free cash flow in Q3 2025 alone - even after absorbing $306 million in Brumadinho payments and $970 million for Samarco in the same quarter. The operations are generating enough cash not just to pay the ongoing dam-related obligations but to do so comfortably while still funding a growing capital expenditure programme of $5.4–$5.7 billion for the full year.

Brazil has a mandatory minimum dividend of 25% of company profit, and Vale has consistently distributed 60–80% of FCF as dividends over the long term. At current prices and a base case iron ore scenario, that translates to a dividend yield of approximately 6–9% per year - an extraordinary level of income for a company that also has meaningful capital appreciation potential as the re-rating plays out. It's worth noting that Brazil recently reinstated a 10% withholding tax on dividends for non-resident shareholders, so investors outside Brazil should verify the net yield applicable to their specific situation.

Valuation - What the Numbers Say

Valuing a cyclical commodity company requires intellectual honesty about the assumptions. We cannot know where iron ore will be in 2027. What we can do is stress-test the valuation across a range of scenarios and ask whether the current price already reflects the worst realistic outcome.

DCF Model: Conservative Base at $13.83

A DCF model built on Vale's Q3 2025 results uses $4.25 billion in FCF as a starting point for 2025 - deliberately conservative given the $1.5–$1.8 billion of additional CAPEX expected in Q4. From there, a 4.5% CAGR over the first five years (reflecting copper/nickel growth, China demand stabilisation, and operational improvements) followed by a 3.5% CAGR for the subsequent five years, with a 2.5% terminal growth rate. Using a WACC of 10.5% and accounting for the full $16.64 billion in expanded net debt (including all dam provisions), the model produces an intrinsic value of $13.83 per share.

This is not an aggressive number - it is a floor built on conservative assumptions. The key sensitivity: if FCF averages $5–$6 billion per year over the next decade (plausible in a normalised iron ore environment and with copper/nickel growing), the intrinsic value rises substantially toward the upper end of our target range. The $13.83 figure is therefore best understood as the lower bound of fair value - the price below which the margin of safety becomes compelling for long-term investors.

What's Priced In vs. What Isn't

The most useful question you can ask about any investment is not "is this a good company?" but "what does the current price assume?" In Vale's case at $12–$14, the price encodes a remarkably pessimistic set of assumptions. Below is our read of what the market has priced in - and what it hasn't.

What the Market Fears (Priced In)

- Permanently uncontrolled production costs (C1/t well above guidance)

- Structural Chinese steel demand collapse, not a cycle

- Open-ended, unpredictable dam liability exposure

- Iron ore in a sustained sub-$90 environment indefinitely

- Brazil political risk with no resolution in sight

- Nickel oversupply permanently destroying segment economics

What the Market Is Missing (Not Priced In)

- C1/t at $20.7 - guidance achieved, cost discipline restored

- India as a genuine secondary growth market for iron ore

- ~75% of dam provisions already settled; remainder clearly scheduled

- ~14% FCF yield sustains dividends even at bear-case iron ore

- Extraordinary dividend trigger at $15B net debt - approaching

- Copper cost down 17% YoY; growing as a portfolio diversifier

- US-China tariff truce reduces the geopolitical risk premium

The Risk Q&A

Rather than listing risks as bullet points, we think it's more useful to address them the way a thoughtful investor would - as questions. Here are the most common objections to this trade, and our honest responses.

Technical Picture

Vale's stock spent much of 2024 and early 2025 in a sustained downtrend, driven by the combination of factors we've described - cost concerns, China sentiment, and the legal overhang. By mid-2025, that selling pressure began to exhaust itself, and the stock has been building a base in the $11–$14 range that is consistent with long-term support at multi-year lows. The $12–$14 entry zone sits squarely within this base, representing the kind of accumulation zone where long-term investors have historically stepped in.

The recovery in iron ore from $92 to $103.5 since July has provided a constructive backdrop. RSI on the daily chart has recovered from oversold levels and is settling in a neutral-to-constructive range, consistent with a stock that has absorbed its sellers and is beginning to attract buyers. Moving averages remain in a challenging configuration - the stock is still below its longer-term moving averages - which is expected given the duration of the downtrend, but the rate of decline is flattening, which is typically the first technical sign of a trend change.

Live Price Chart (NYSE: VALE)

The Trade

The following scenarios reflect the author’s personal analysis and are not investment recommendations. See our full disclaimer.

Core Thesis: Scenario Range for VALE in the $12–$14 Zone

Vale S.A. at current prices represents a compelling risk/reward opportunity in a high-quality, world-scale mining company whose near-term headwinds are well-known and largely priced in, while its improving cost structure, mapped legal liability schedule, extraordinary dividend trigger, and copper/nickel growth runway are not. A ~14% FCF yield, a 6–9% dividend yield in the base case, and a DCF floor near $13.83 provide significant downside support. The path to $17–$22 runs through cost discipline, iron ore seasonality, and the gradual re-rating of a market that has been too pessimistic for too long.

Catalyst Timeline: Q4 2025 – Q4 2026

Execution Guide

- Scenario Entry Range: $12–$14. Build in tranches. Tranche 1 (50%) at $12.50–$13.50 immediately. Tranche 2 (30%) at any pullback toward $11.50–$12.50. Tranche 3 (20%) in reserve for a potential flush toward $10.50–$11.00 on broad EM risk-off.

- Risk Consideration: This is a moderate-to-high risk position due to commodity price sensitivity and EM exposure. 3–5% of a diversified portfolio is appropriate. Income-focused investors may size toward the higher end given the 6–9% base-case dividend yield, which compensates for holding time.

- Dividend Collection: Vale pays dividends semi-annually. Collecting dividends while waiting for the thesis to develop reduces effective cost basis and provides a material yield during the holding period. Non-resident investors: verify the applicable net yield after Brazil's 10% withholding tax for your specific jurisdiction.

- Upside Scenario Milestones: First exit (30%) at $16–$17 - initial resistance zone and near the DCF intrinsic value floor. Second exit (40%) at $19–$20 - mid-target zone, approaching historical valuation support. Final exit (30%) at $21–$22 - upper target, full re-rating scenario.

- Thesis Invalidation Level: $10.50. A sustained close below this level indicates either iron ore structurally below $80 or an unexpected escalation in the legal liability. Below this level the thesis no longer holds.

- Key Monitoring Points: Weekly iron ore spot price (DCE contract); Vale's quarterly C1/t cost results; net expanded debt trajectory toward the $15B extraordinary dividend trigger; any developments in the UK Samarco/Brumadinho legal proceedings; China FAI and real estate investment data monthly.

Important Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. Past performance does not guarantee future results. All investments carry risk, including the possible loss of principal. Vale S.A. (NYSE: VALE) is subject to commodity price risk, emerging market risk, geopolitical risk, currency risk (BRL/USD), legal liability risk related to the Brumadinho and Samarco dam disasters, and general market risk. Iron ore prices are highly volatile and may not follow the seasonal or cyclical patterns described herein. Chinese economic policy, real estate activity, and steel demand are inherently unpredictable. Brazil's interest rate environment and regulatory framework may change materially. The 10% withholding tax on dividends for non-resident shareholders may reduce effective dividend yields; investors should consult a tax advisor regarding their specific situation. The DCF valuation and FCF yield estimates are based on publicly available information and independent analytical models as of December 2025; actual results may differ materially. Always conduct your own due diligence and consult a qualified financial advisor before making any investment decision.