In security, a false positive is when your system flags something as a threat that isn't one. Markets produce their own version of this - and right now, the sell-off in Zscaler is the most expensive false positive I've seen in cybersecurity in years. The stock has lost more than 50% from its 2025 highs on two legs: first, a 13% single-day drop after Q1 FY26 earnings when a guidance raise wasn't dramatic enough for a market that had come to expect miracles; then a second leg down in February 2026 as the so-called "SaaSpocalypse" narrative - the idea that vibe-coded AI tools will reduce enterprise demand for SaaS - swept indiscriminately through the software sector. Zscaler got caught in that wave despite having almost nothing to do with it.

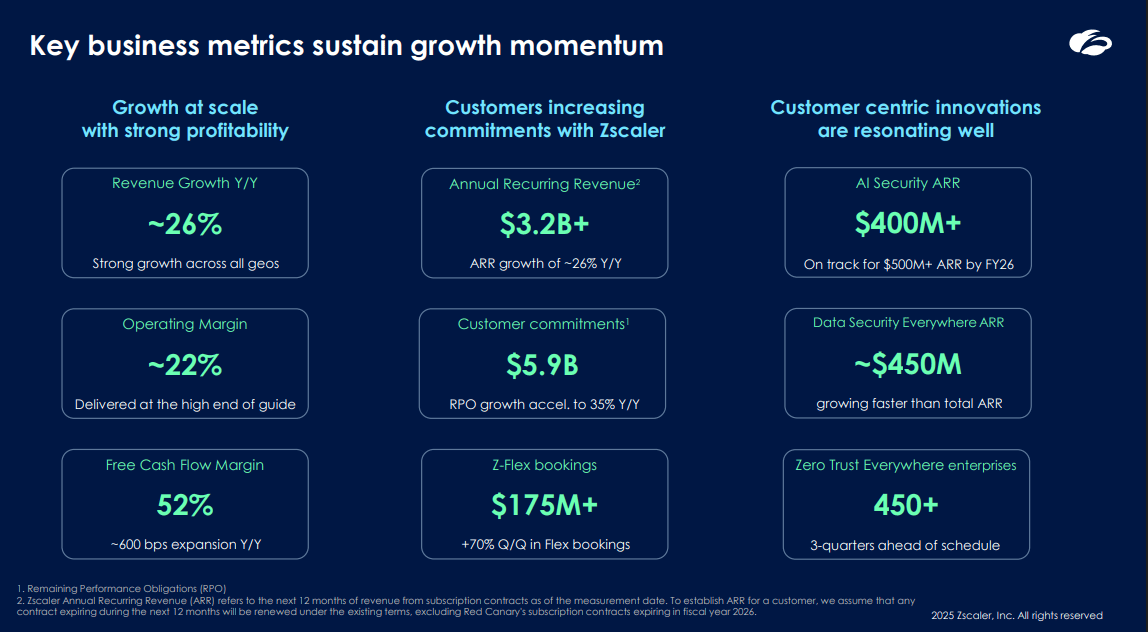

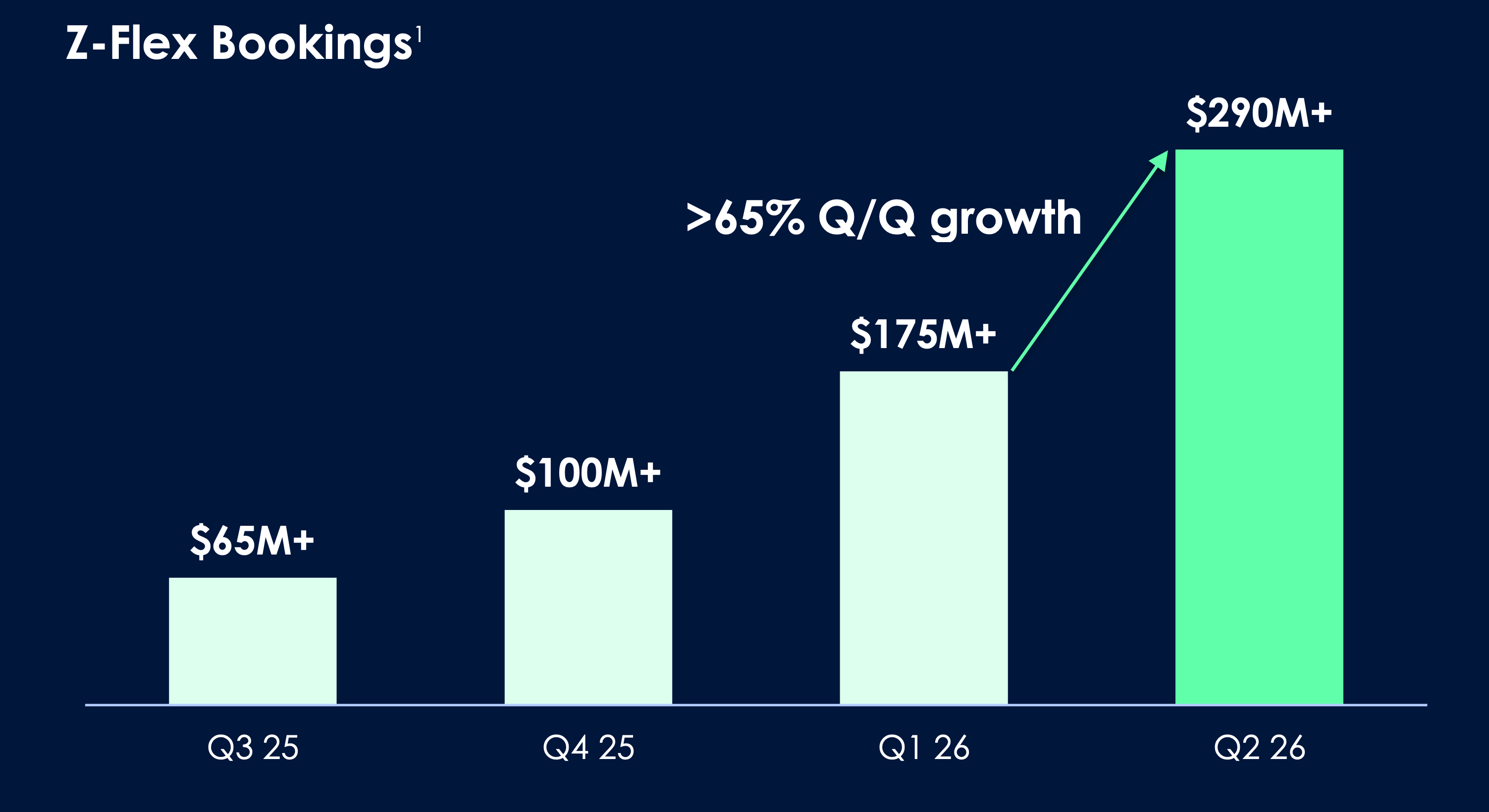

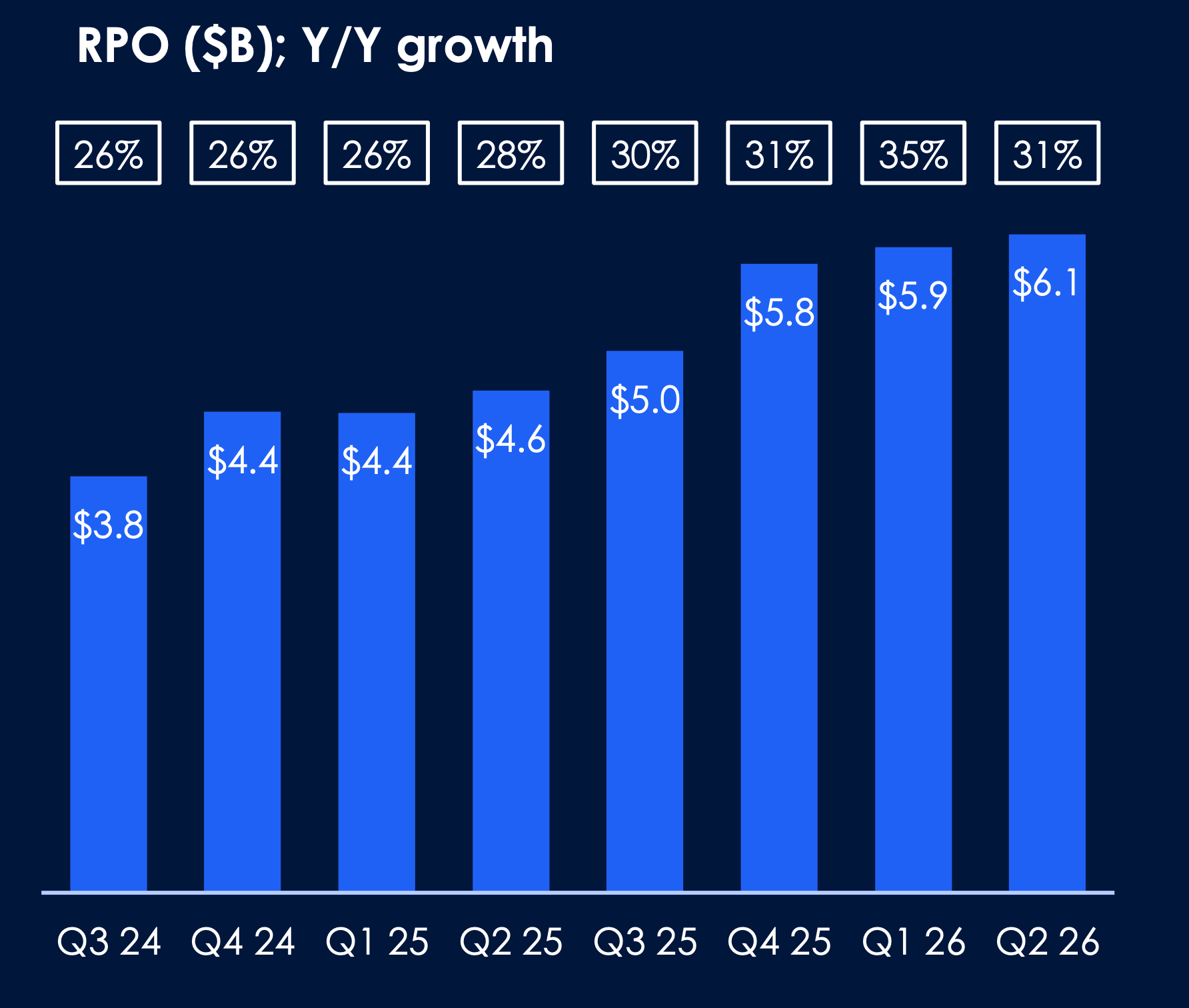

In Q2 FY26, revenue reaccelerated to 26% year-on-year, beating $798 million consensus with $815.8 million in actuals. The remaining performance obligation - contracted future revenue, not analyst estimates - hit $6.1 billion growing at 31%. Free cash flow margin reached 52% in Q1 FY26, 700 basis points better than a year prior. Z-Flex clocked $290 million in bookings in Q2'26 alone - more than four times the Q3'25 pace - and has now generated nearly $650 million in total contract value in its first year, with average terms of four years. AI Security ARR crossed $400 million three full quarters ahead of schedule. The company has beaten earnings estimates in twelve consecutive quarters. This is not deterioration. This is acceleration dressed in a falling stock price.

The entry zone of $145–$150 represents roughly 8x EV/Revenue - an all-time low for Zscaler, against a five-year median multiple of 15.3x and a three-year median of 13.2x. ZS is currently cheaper than CrowdStrike, Cloudflare, and Palo Alto Networks on every single valuation metric: EV/Sales, Price/Earnings, and Price/Free Cash Flow - despite having the fastest five-year revenue growth rate in the group at 44%. The path to $223–$246 asks for nothing heroic: a partial recovery to 10–11x forward revenue on FY27 estimates. The AI-Security opportunity, a $100 billion SAM that barely existed eighteen months ago, is not priced into any of those numbers. That is the margin of safety.

Key Metrics at a Glance

Let me be direct about what these numbers represent. When revenue grows 26% at $816 million scale, that is not a company slowing down - it is a company expanding its lead. When RPO hits $6.1 billion growing faster than revenue, customers are committing to longer, larger contracts before Zscaler has even recognised the income. That is what a platform looks like when it has become mission-critical infrastructure, not discretionary tooling.

The Rule of 40 is the software industry's standard health check: revenue growth plus profit margin should exceed 40 for a sustainable, high-quality SaaS business. Zscaler scores 78 - revenue growth of 26% plus Q1 FCF margin of 52% (note: Q1 FCF margin of 52% reflects a seasonal billing concentration - the company's full-year FCF margin guidance is 26-26.5%, with Q1 being structurally the strongest quarter due to annual contract renewals) - one of the highest readings in the industry. By contrast, if you use the non-GAAP operating margin of 22% the score is 48; still excellent, but the FCF number is what shows what the business actually earns before reinvestment decisions. Non-seat-based usage - the category that most directly addresses SaaSpocalypse fears - already accounts for more than 25% of new Annual Contract Value and is growing over 100% year-on-year. The market is pricing in an AI disruption that Zscaler is, in fact, benefiting from.

Customer quality is compounding alongside revenue. There are now 728 customers paying more than $1 million in ARR - up 18% year-on-year - and 3,886 paying above $100,000, also up 18%. Net revenue retention is 115%, meaning existing customers on average expand their spend by 15% every year without Zscaler needing to close a single new logo. The 52% free cash flow margin in Q1 FY26 - up from 45% two years prior - is the real signal: the company is not spending its way to growth, it is growing into a cost structure already built for a far larger business.

What Zscaler Actually Is - and Why It's Hard to Displace

The single biggest misunderstanding about Zscaler in the current market is that it is just another security vendor - an expensive point product in an increasingly crowded space that Microsoft or CrowdStrike could subsume tomorrow. That framing is fundamentally wrong, and it is the reason the stock is currently mispriced by a wide margin.

The traditional enterprise security model operates on what the industry calls a "castle and moat" principle: route all traffic through a firewall or VPN perimeter, and once a user is past the moat, treat them as trusted. The catastrophic weakness is that one compromised credential gives an attacker full access to the entire network. Zscaler's architecture eliminates the moat entirely. Every single request - from every user, device, application, or AI agent - is treated as an outside request until inspected and verified. There is no trusted interior. There is no perimeter to breach.

Zscaler built, from scratch, the world's largest security cloud. Its Zero Trust Exchange processes more than 500 billion daily transactions across 50 million users - and every novel threat discovered anywhere on that network instantly propagates as a defence to every other user. No enterprise can replicate this internally: the scale of threat intelligence is itself the product. It took Zscaler fifteen years and billions of dollars in infrastructure capital to build. The moat is not intellectual property that a competitor can patent around - it is the network itself, and the data flywheel it generates. Every transaction Zscaler inspects trains its AI to detect the next attack faster. The more data it sees, the smarter it gets, the better the product becomes, the more customers it attracts, the more data it sees. That cycle does not benefit a late-arriving competitor.

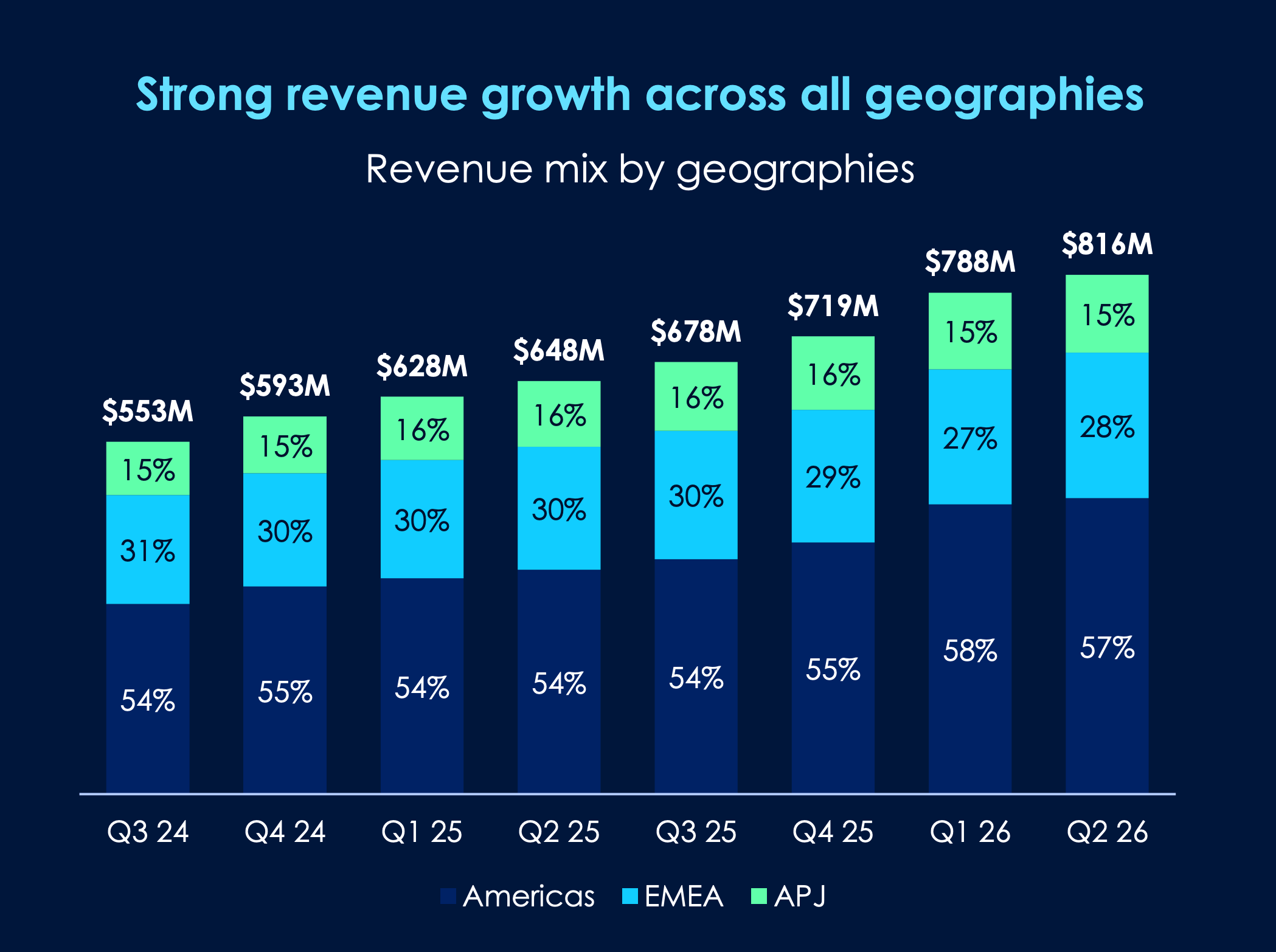

The geographic diversification tells an important story. Americas contributes roughly 57% of revenue, EMEA 28%, APJ 15% - and all three segments are growing. This is not a US-only story subject to single-market regulatory or macro shock. As enterprises globally accelerate cloud migration, the demand for a cloud-native security architecture follows naturally. Zscaler is the company that built that architecture at scale.

"In the large enterprise space - about 20,000 employees - if anything, I would say the competition has become less. These large enterprise customers are CIOs, CISOs, they all know us. The biggest focus is: one, I want to remain safe, give me Zero Trust and help me secure my AI initiatives. Two, can you do it with greater ROI and remove some of the cost? A firewall company won't do that, even though they try to talk about platform - because the biggest spend in security is still firewalls. They have to cannibalize it. We like to cannibalize it."

- Jay Chaudhry, CEO, Zscaler - Morgan Stanley TMT Conference, March 2, 2026The platform now spans four major solution pillars: Zero Trust Everywhere (users, branches, cloud workloads), Data Security Everywhere (DSPM, DLP for GenAI SaaS), Security for AI Applications (AI asset discovery, AI red teaming, AI Guardrails), and Agentic Operations (AI-powered IT and security ops). Each pillar is generating its own ARR stream. The point is that Zscaler is not a one-dimensional product company - it is rapidly becoming the security operating system for the AI enterprise.

Twelve Consecutive Quarters of EPS Beats - Every Single One

There is one data point that the current bear narrative needs to reckon with and cannot: Zscaler has beaten consensus EPS estimates in every single quarter reported since FQ3 2022. Not most quarters. Not a strong track record with a couple of misses. Every. Single. Quarter. In the most recent quarter (FQ2'26), the company delivered $1.01 adjusted EPS against a consensus estimate of $0.96 - a beat on top of an already-elevated estimate bar. That is not what a company with structural deterioration looks like.

The Q1 FY26 results are a useful template for understanding how this management team operates. Revenue guidance was $772M–$774M. They delivered $788M - a $15 million beat on a $773 million expectation. Operating profit beat. EPS of $0.96 came in 11% above the $0.85–$0.86 guided range and 25% above the prior year. The company then raised its FY26 revenue guidance from the initial range of ~$3.14–$3.16 billion to $3.282–$3.301 billion. That's how the beat-and-raise machine works, every single quarter.

To invest well in Zscaler you also need to hold the uncomfortable parts of the thesis honestly. Stock-based compensation runs at roughly 24.6% of revenue - high by any standard. The company reported a GAAP net loss of $11.6 million in Q1 FY26 despite $788 million in revenue, driven almost entirely by SBC. Annual dilution from SBC and convertible debt conversion runs 3–4%. There are no share buybacks. These are real costs to current shareholders and they matter. The non-GAAP EPS beat tells you how the business operates. The GAAP numbers tell you how much management is being compensated through equity. The investor's job is to weight both - and to decide whether the operating quality of the business justifies the dilution drag. At 8x EV/Revenue, and with a Rule of 78 on FCF, I believe the answer is yes by a wide margin.

The pattern of systematic under-promise and over-deliver is not accidental. It reflects a business with extraordinary forward visibility into contracted revenue (RPO), a manageable and predictable cost structure driven by recurring subscriptions, and a sales motion - Z-Flex - that is structurally reducing the friction of closing large, multi-year commitments. The market, in its current state of fear about SaaS broadly, is confusing Zscaler with a seat-based productivity tool that AI might displace. That is a category error that patient investors can capitalise on.

The Booking Machine - Z-Flex and RPO Tell the Real Story

If earnings-per-share is the rearview mirror, Remaining Performance Obligations and bookings data are the windshield. Both of them are pointing in the same direction: forward, and accelerating.

Z-Flex is Zscaler's consumption-based, flexible contract model - and it is growing at a rate that should be commanding attention far beyond what the stock price implies. In Q3'25, Z-Flex booked $65 million. In Q4'25: $100 million. Q1'26: $175 million. Q2'26: $290 million plus - more than 65% quarter-on-quarter growth. In three quarters, this product has gone from an interesting experiment to the company's most powerful sales motion.

The strategic importance of Z-Flex is that it eliminates the biggest friction point in enterprise security procurement: the upfront commitment to a full Zero Trust transformation. Large enterprises know they need to move away from legacy firewall architectures - but the CFO wants to see ROI before signing a $20 million, five-year platform contract. Z-Flex solves this by providing a multi-year commitment with the flexibility to activate or swap modules without re-entering the procurement cycle. Customers start where their budget allows, see the value delivered, and expand. The average Z-Flex contract runs four years. In less than twelve months since launch, the program has generated nearly $650 million in total contract value.

The deal quality is also notable. Management cited an eight-figure, five-year Z-Flex contract with an insurance company that expanded module adoption from eleven modules to sixteen - including Zscaler's new AI Security products. A Fortune 500 services firm doubled its entire ARR with Zscaler through Z-Flex. These are not pilots or proofs-of-concept. These are enterprise-scale, multi-year commitments that deepen the platform's entrenchment at exactly the moment when the market is pricing Zscaler as though it is at risk of losing customers. The direct sales channel - bypassing resellers - is also growing, from 11% of revenue to 15% year-on-year. Zscaler is building a more direct relationship with its largest buyers, which both protects margin and accelerates the Z-Flex land-and-expand motion.

The RPO trajectory is equally compelling. From $3.8 billion in Q3'24 to $6.1 billion in Q2'26 - 31% year-on-year growth - with the growth rate itself accelerating (35% in Q1'26 before settling at 31% in Q2'26 as the comparables got tougher). This is contracted, committed future revenue. When RPO grows faster than recognised revenue, it means the bookings pipeline is expanding ahead of revenue recognition. The company is building a revenue buffer that will support reported growth well into FY27 and FY28.

The AI-Security Frontier - The Opportunity the Market Hasn't Priced In

Here is the bear case's central irony: the very thing the market fears - artificial intelligence - is actually the most powerful tailwind Zscaler has ever seen. Every AI model deployment, every AI agent with access to internal systems, every GenAI SaaS tool that employees are using introduces new attack surfaces that legacy security architectures are completely blind to. Zscaler is the company that has built the framework to secure this new landscape.

The AI-Security ARR figure - $400 million and growing toward $500 million by FY26 end - represents products that barely existed eighteen months ago, and the pace at which they are growing should reframe the entire bear narrative. CEO Jay Chaudhry said on the Q1 FY26 earnings call: "I'm particularly pleased with our AI Security pillar, which grew over 80% year-over-year and has already exceeded our FY '26 target of $400 million ARR, three quarters earlier than expected. With the strong demand, I expect AI Security ARR to exceed $0.5 billion by the end of this fiscal year." A target reached three quarters early is not a company struggling with AI disruption. It is a company that turned the threat narrative into a revenue stream.

Two acquisitions in the back half of 2025 underpin this momentum. Red Canary, acquired in August 2025 for $675 million, is a Managed Detection and Response provider - it combines advanced security tooling with human threat hunters to prevent data breaches. By Q1 FY26 it was already performing ahead of schedule: the CFO confirmed Red Canary exceeded its internal $3 million quarterly ARR growth target in its first quarter inside Zscaler. SPLX, acquired in November 2025, brought AI Red Teaming capability - automated and continuous testing of AI applications for hallucination, bias, behaviour drift, and adversarial attack resistance. CEO Chaudhry cited a Fortune 150 transportation company and a Fortune 100 service provider as early SPLX customers.

The threat that AI Security addresses is not theoretical. Chaudhry disclosed on the earnings call: "One of the largest AI companies recently reported that a bad actor hijacked its AI coding assistant to autonomously perform a large-scale cyberattack against multiple organisations." AI agents are not inherently safe. They access sensitive data, interact with internal systems, execute code, and communicate with external services - every one of those actions represents an attack surface that the legacy castle-and-moat model cannot protect. Zscaler AI Guard is licensed on a token basis, not a seat basis - which means that as AI agents proliferate (Citi research estimates they will eventually outnumber human workers), Zscaler's addressable revenue expands without requiring a single additional human user to be on-boarded. The SaaSpocalypse narrative gets the direction exactly backwards for Zscaler.

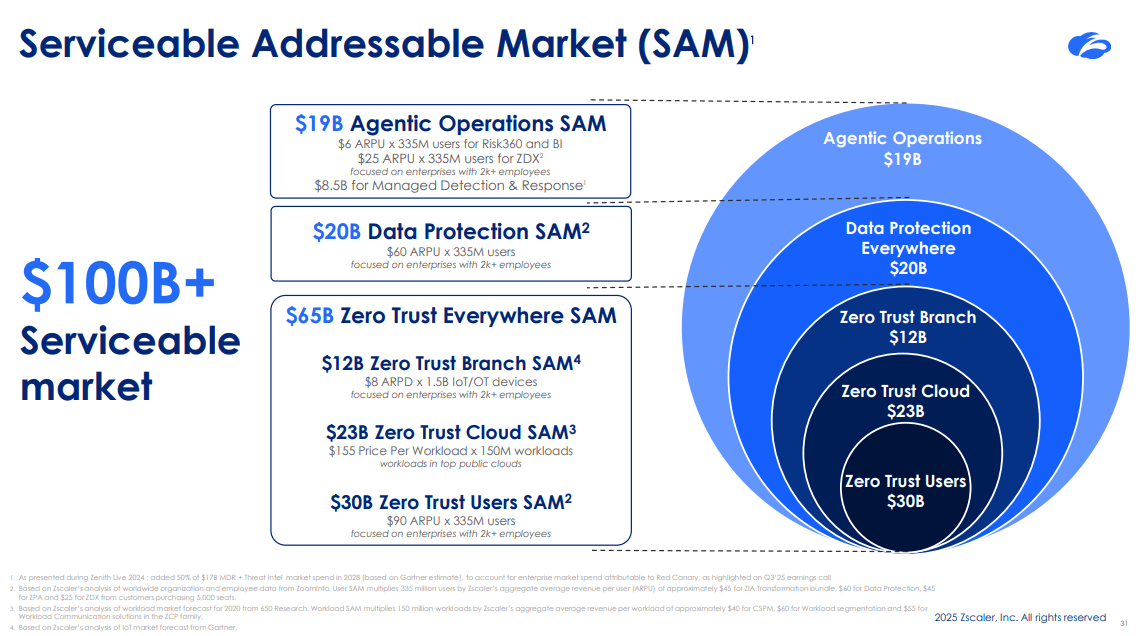

Data Security Everywhere ARR is already tracking at approximately $450 million - a fully separate revenue stream from the Zero Trust core - and growing faster than total ARR. The company has 450+ Zero Trust Everywhere enterprises, three full quarters ahead of schedule. ZDX Copilot, Risk360, Business Insights, Identity Threat Detection, Unified Vulnerability Management, Cyber Asset Attack Surface Management: these are products that didn't exist at meaningful scale when the stock was trading at $337. They exist now, they're generating ARR, and they address a total addressable market the company puts at $19 billion for Agentic Operations alone. None of this is priced into a stock at 8x EV/Revenue.

Margins, Free Cash Flow & Guidance - The Financial Architecture

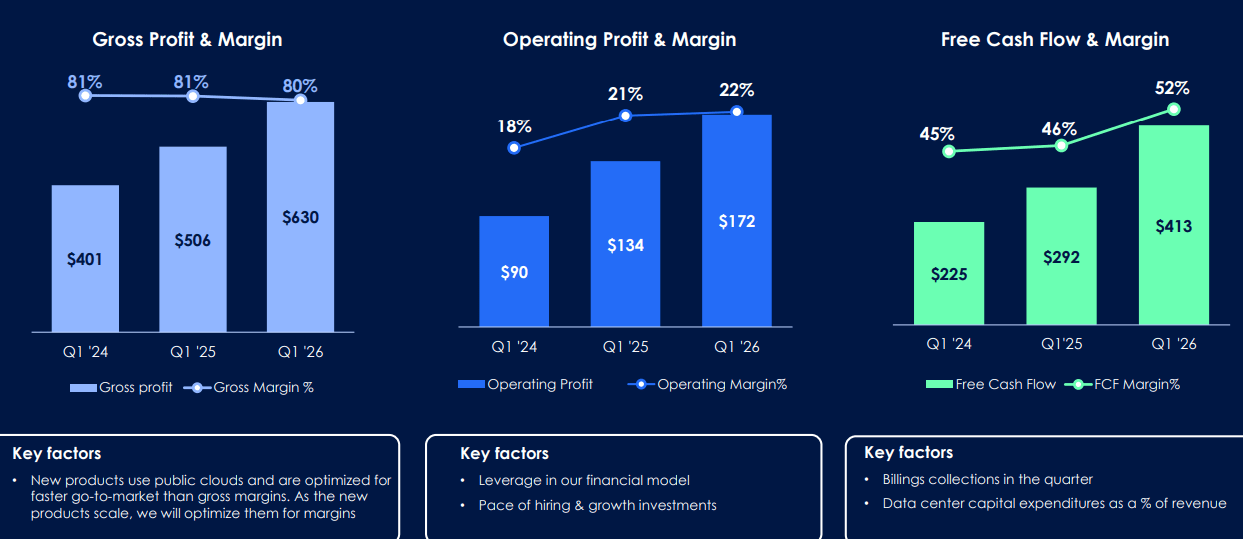

The three-year margin progression tells a story of consistent operational leverage. Gross profit went from $401 million in Q1'24 to $630 million in Q1'26 - a 57% increase, with margins holding steady at 80%. Operating profit nearly doubled in the same period: from $90 million (18% margin) to $172 million (22% margin). Free cash flow went from $225 million to $413 million - an 84% increase - with the margin expanding from 45% to 52%.

This is not a company spending its way to revenue growth at the expense of profitability. It is a company demonstrating that scale compounds in high-margin SaaS businesses exactly as the theory says it should. Every dollar of incremental revenue generates substantially more free cash than the dollar before it.

The FY26 guidance - raised after each of the first two quarters - stands at $3.282–$3.301 billion in revenue, $3.698–$3.718 billion in ARR, and adjusted EPS of $3.78–$3.82, with a free cash flow margin guide of 26.0–26.5% for the full year. The FCF margin guide is slightly below FY25's 27.2% - management has been transparent that new products (AI Security, Data Security) are being deployed on public clouds at higher near-term infrastructure cost to accelerate go-to-market speed rather than optimise margins immediately. This is a conscious short-term choice with a clear long-term payoff as those products scale. The trend is unambiguous: non-GAAP operating margins have expanded 6.8 percentage points since FY23, and the structural economics of SaaS mean further leverage is almost automatic as revenue grows.

The balance sheet provides both comfort and optionality. At quarter-end: $3.3 billion in cash and short-term investments, $1.7 billion in convertible notes at 0% coupon maturing in 2028, current ratio of 1.75. The company carries a net cash position of approximately $1.6 billion. It has demonstrated a clear appetite for strategic acquisitions in AI - Red Canary, SPLX - and has the capacity to continue deploying capital into the fastest-growing parts of the market. No existential financing risk. No debt-service pressure. A balance sheet that looks like a fortress, which is appropriate for a company that sells fortresses.

The $100 Billion Opportunity - Revenue That's Still Ahead

Zscaler currently generates approximately $3.3 billion in annual recurring revenue. Its serviceable addressable market is $100 billion - a number that encompasses $65 billion from Zero Trust Everywhere, $20 billion from Data Protection, and $19 billion from Agentic Operations. Even with generous market-share assumptions, the company has captured less than 4% of its own SAM. The runway is not measured in quarters.

What makes the market opportunity credible - rather than aspirational slide-deck content - is that each of these SAM segments is being approached with products that are already generating meaningful ARR. The Zero Trust Everywhere products underpin the $3.2 billion ARR base. Data Security is approaching $450 million. Agentic Operations and AI-Security together are tracking toward $500 million by year-end. The company isn't pitching a market it might eventually address. It is already inside it, compounding.

One of the more underappreciated dynamics here: 53.8% of Zscaler's revenue now comes from expanding existing customers rather than acquiring new ones. That number matters because it tells you something structural - the platform has genuine land-and-expand economics. Customers aren't churning. They're deepening. The 8-figure insurance company example from the Q1 earnings call (11 modules on entry, now at 16) isn't an anecdote. It's a pattern. And Z-Flex makes that pattern easier to repeat at scale by removing the upfront commitment barrier that historically slowed enterprise adoption.

Valuation vs. Peers - The Discount Is Real

The bear case often lands on "still expensive." The data says otherwise. At current prices, Zscaler is the cheapest name in its peer group on every valuation metric - and the only one with a five-year revenue CAGR above 40%.

| Company | EV / Sales | P / E (fwd) | P / FCF | 5Y Rev CAGR |

|---|---|---|---|---|

| ZS (Zscaler) | 8.2× | 41× | 30× | 44% |

| CRWD (CrowdStrike) | 21.5× | 88× | 88× | 41% |

| NET (Cloudflare) | 31.3× | 174× | 262× | 38% |

| PANW (Palo Alto) | 13.2× | 45× | 38× | 22% |

Sources: FactSet / YCharts consensus estimates, March 2026. Forward P/E based on non-GAAP EPS.

The competitive question - can anyone else build this? - is the one I keep returning to. Microsoft has Defender and Entra. CrowdStrike has Falcon. Palo Alto has Prisma. Each competes with Zscaler at the edges. None has built a cloud-native, globally distributed proxy architecture with Zscaler's inspection depth and breadth.

Palo Alto deserves specific mention because their competitive playbook is the sharpest in the market. The tactic: offer free bundled services for the duration of a competitor's existing contract to force migration conversations. Chaudhry has addressed this directly - Zscaler wins those evaluations on technical merits because the inspection architecture isn't something PANW's Prisma Access can replicate at the data layer. "Platformization" is a compelling sales narrative; it is less compelling when the platform lacks the actual proxy infrastructure to deliver on it. Zscaler's data shows it: customers who go through competitive evaluations against PANW still choose ZS in large-enterprise deals where security depth matters more than price incentives.

To compete at Zscaler's platform level requires exactly the kind of capital-intensive, infrastructure-first construction that takes a decade or more. The window for disruption was ten years ago. It's effectively closed.

What the Bears Get Wrong - Attack Vectors vs. Fundamental Reality

In security parlance, an attack vector is the path an adversary uses to gain access to a system. The bear case on Zscaler relies on six attack vectors. Most can be neutralised by the data. One deserves an honest partial concession.

"Growth is decelerating - 22–23% guide is slower than 26% actuals. The best is behind us."

Guidance is intentionally conservative - the company has beaten it by 2–4 percentage points every quarter for three years. The FY26 guide of ~23% will almost certainly print closer to 26–28% on actuals. More importantly, RPO is growing at 31–35% - ahead of recognised revenue - which means the pipeline of future revenue is expanding, not contracting. Z-Flex bookings at $290M in a single quarter represent a new growth engine that wasn't factored into consensus estimates six months ago.

"AI will commoditize network security. Microsoft and CrowdStrike will roll up everything Zscaler does."

This confuses endpoint security (CrowdStrike's domain) and identity management (Microsoft's Entra) with network security and data access control (Zscaler's domain). They are different layers of the security stack and enterprises need all of them. More critically, AI is creating a massive new attack surface that none of those incumbents are positioned to secure at the network level - but Zscaler is. AI Security ARR is already at $400M and growing. The company isn't a casualty of AI. It's a beneficiary.

"The valuation is still too expensive for a growth slowdown environment. Even after falling 50%, it's not cheap."

At $145–$150, Zscaler trades at approximately 6.5–7x forward (FY26) revenue. In 2019, when the business was a fraction of its current size with far lower profitability and no FCF to speak of, it traded at similar multiples. The company now generates a 52% FCF margin, has $6.1B in contracted backlog, and is growing AI-Security revenue from zero. A premium to 2019 multiples is justified. Even a recovery to 10–11x FY27 revenue gets to $223–$246 without requiring any multiple expansion beyond historical norms.

"Enterprise IT budgets are under pressure - large deals will get pushed or cancelled."

Cybersecurity is the last line item that enterprises cut. Data breaches average $4.5M per incident and regulatory exposure in financial services, healthcare and critical infrastructure is rising - not falling. The Z-Flex model was specifically designed to address budget timing concerns by allowing companies to start small and consume more as they see value. That's why Z-Flex bookings accelerated 65%+ Q/Q in Q2'26 even in a cautious spending environment. The demand is there. The product matches the buying behaviour of cautious IT departments.

"Stock-based compensation is out of control - 24.6% of revenue in SBC means GAAP earnings are a fiction and shareholders are being silently diluted."

This one deserves an honest answer rather than dismissal. SBC at 24.6% of revenue is high, and the ~3–4% annual dilution is real. Zscaler's GAAP net loss in Q1 FY26 was -$11.6M - the profitability story depends entirely on non-GAAP adjustments. The counter: SBC as a percentage of revenue has been declining year over year as the revenue base scales, the company is generating $1.7B+ in real FCF annually, and the $3.3B cash balance with $1.7B in 0% convertible notes gives it optionality without needing to issue equity. High SBC is a feature of every major software-infrastructure company in the growth phase. The question is whether it normalises - and the trend says it is. Management's FY26 FCF guide of 26.3% (temporarily lower due to public cloud infrastructure deployment costs) still implies ~$1.1B in cash generation this fiscal year.

"Palo Alto is giving away security for free to knock out Zscaler. They'll bundle Prisma Access at zero marginal cost and starve ZS of new logos."

The "platformization" playbook is real and Palo Alto is executing it aggressively - offering to match a competitor's product for free for the duration of their existing contract to accelerate migration conversations. In mid-market and SMB, this is a genuine threat. In large enterprise, it isn't. The reason is architectural: Prisma Access is built on a VPN-backbone model with added cloud functionality. Zscaler is built from the ground up as a cloud-native proxy that sits between the user and the internet, inspecting traffic at the packet level. You cannot replicate that with bundling. When Fortune 500 IT security teams run bake-offs - which they do - Zscaler wins the technical evaluation at the data protection and inspection layer. PANW wins on price sensitivity and existing firewall relationships. Zscaler's 728 customers above $1M ARR and accelerating NRR at 115% suggest those technical wins are holding.

Three Scenarios - Conservative, Base & Bull

Each scenario is built on FY27 estimates and an enterprise-value-to-revenue multiple appropriate to the growth and margin profile. FY27 begins August 2026. The 12-month holding period from entry aligns with the FY27 revenue story becoming visible to the market.

The expected value across these three scenarios - probability-weighted - lands comfortably above $200, against an entry of $145–$150. The risk/reward is strongly asymmetric. The conservative scenario, which requires both a meaningful macro deterioration and Zscaler underperforming its own conservative guidance, still results in a gain from entry - a reflection of how strong ZS's valuation floor is at 8x EV/Revenue with 52% FCF margins. The base and bull scenarios, which are anchored on conservative assumptions for a company with ZS's track record, imply 50–65% upside. That is an exceptional setup.

Catalyst Roadmap - What Moves the Stock

The investment thesis doesn't require a single binary event. It plays out across a series of compounding catalysts over the next twelve months.

Reading the Damage - Technicals Confirm an Extreme

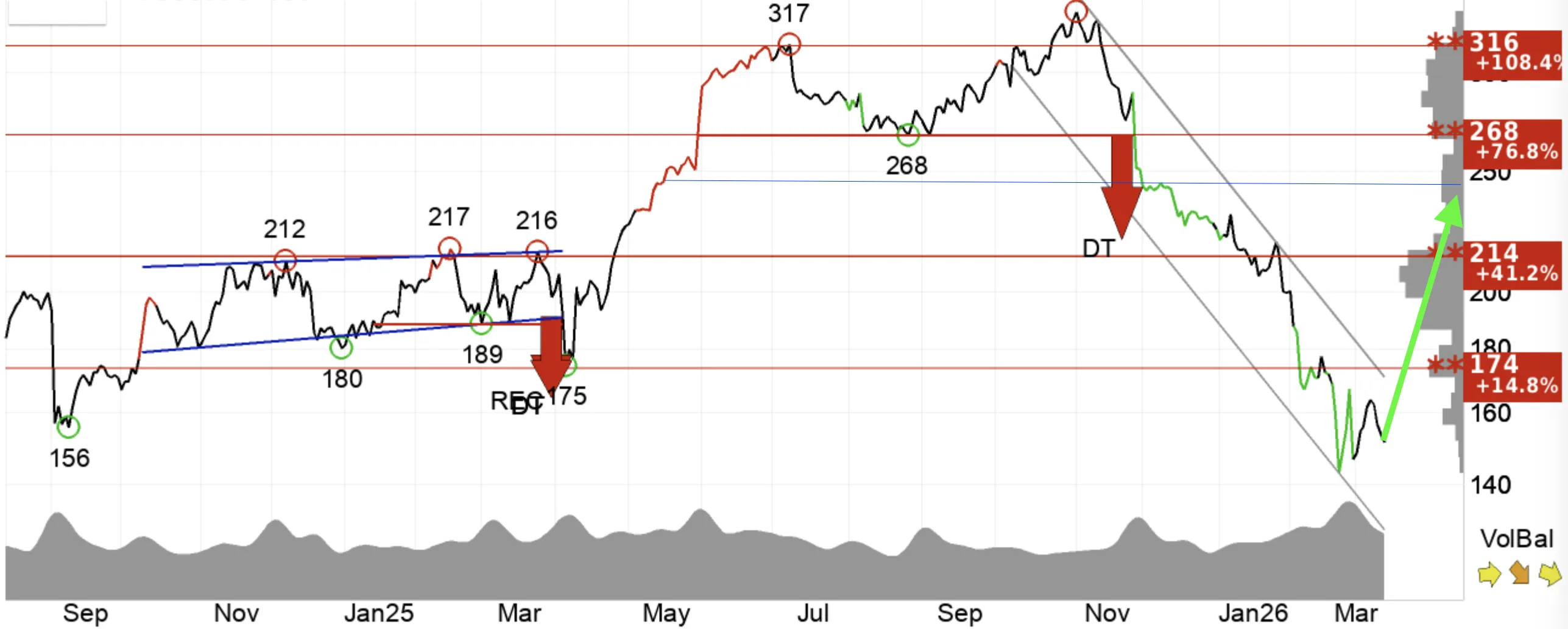

I rarely build a thesis on technical analysis alone - the fundamentals need to lead. But in this case, the chart is a useful validator. It confirms that the ZS selloff has been severe enough to reach the kind of extreme readings that historically precede significant reversals in high-quality large-cap technology stocks.

The weekly chart tells a stark story. The 50-day simple moving average sits at approximately $252 - more than 40% above the current price. The 200-day SMA, often seen as the institutional benchmark for trend direction, is at approximately $189. ZS is trading well below both - a structural downtrend that has accelerated through the $200 and $175 support zones. The stock peaked at $337 in late 2025 and has retraced more than 50% from that high.

The chart above identifies the key structural levels. The double-top (DT) pattern that formed around $268–$317 in mid-to-late 2025 triggered the breakdown that accelerated the current downtrend. Immediate resistance on any bounce sits at $174 (+14.8% from the entry midpoint), then $214 (+41.2%), $268 (+76.8%), and ultimately the prior high cluster near $316 (+108.4%). The entry zone of $145–$150 sits near documented support from the 2023–2024 base-building range - the same consolidation zone the stock used before its run to $337.

Most critically: the RSI at the time of writing is in the 19–20 range, which represents deeply oversold territory by any standard measure. What is notable is that even as the price has continued to make new lows, the RSI has begun to show positive divergence - a classic early-stage signal that the selling momentum is exhausting itself. In large-cap technology, RSI readings this extreme have historically provided high-conviction entry opportunities for investors willing to look past the fear.

The technical setup does not guarantee a recovery - no chart pattern ever does. But when extreme oversold conditions coincide with accelerating fundamentals and deeply discounted valuation, the probability of an asymmetric outcome tilts meaningfully to the upside. The $145–$150 zone is where the fundamental thesis and the technical exhaustion signal converge. That is precisely the kind of entry I look for.

The Trade - Execution Protocol

The following scenarios reflect the author’s personal analysis and are not investment recommendations. See our full disclaimer.

Zscaler at $145–$150 represents a rare alignment of a deeply discounted valuation, an extreme technical oversold condition, and a business that is accelerating - not deteriorating. The setup is asymmetric. The work is to size appropriately, execute systematically, and stay focused on the twelve-month horizon during which the catalysts above have the time to play out.

- ENTRY > Build in two tranches. Tranche 1 (60%) at $145–$150 immediately on confirmation of entry zone. Tranche 2 (40%) on any additional weakness toward $135–$140, or on the first technical bounce confirmation (close above $165 on rising volume) to average in with momentum.

- SIZE > 3–5% of a diversified equity portfolio is appropriate given moderate-to-high risk classification. Technology-focused investors may size toward the upper end given portfolio context. This is a growth stock with elevated sensitivity to interest rate expectations and macro sentiment - size accordingly.

- TP1 > Take 25–30% off the position at $185–$200. This zone represents near-term technical resistance and protects profit in the event the recovery stalls. Reduces cost basis materially while keeping core position in play.

- TP2 > Take a further 35–40% off at $215–$225. This is the base-case midpoint and the range where institutional demand from re-rating should create natural supply pressure. Locks in the majority of the base-case gain.

- TP3 > Hold the final 30–35% with a trailing stop below the prior quarterly low. In the bull scenario, let this portion run toward $246+. The AI-Security narrative has the potential to drive a re-rating that extends beyond the 12-month initial target.

- STOP > Hard stop on a sustained weekly close below $128. This would indicate either a fundamental deterioration - a dramatic guidance miss or major competitive loss - or a broad market de-risking severe enough to question all growth valuations. Below this level the thesis no longer holds.

- MONITOR > Track quarterly: RPO growth rate (deceleration below 25% would be a yellow flag), Z-Flex bookings trajectory, AI Security ARR vs. $500M target, and FY27 guide set in August 2026. Monthly: RSI and price relative to the $174 and $189 (SMA200) resistance levels.

Core Thesis - Three Sentences

- Zscaler is the dominant Zero Trust cloud security platform, generating $3.2B in ARR with 80% gross margins and a 52% FCF margin, trading at the cheapest valuation in its post-IPO history.

- The selloff is driven by sentiment, sector rotation, and macro fears - not by any fundamental deterioration in the business, which has beaten EPS estimates in twelve consecutive quarters and accelerated its bookings growth rate through the correction.

- The AI-Security opportunity - a $400M+ ARR stream growing from zero eighteen months ago - is not priced into the stock at $145–$150, and represents the single largest underappreciated source of multiple expansion over the next two to three years.

Important Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. Past performance does not guarantee future results. All investments carry risk, including the possible loss of principal. Zscaler, Inc. (NASDAQ: ZS) is a high-growth technology company subject to significant risks including: competitive pressure from Microsoft, CrowdStrike, Palo Alto Networks, and other cybersecurity vendors; dependence on continued enterprise adoption of Zero Trust architecture; macroeconomic sensitivity as a long-duration growth asset; concentration risk in enterprise IT spending; and potential for valuation compression if growth rates normalise toward 15% or below. The technical analysis presented reflects historical price and volume data and is not a guarantee of future price movements. RSI and moving average signals are lagging indicators with well-documented limitations. The scenario analysis and price targets are based on publicly available information, independent modelling, and analyst consensus data as of March 2026; actual results may differ materially. Always conduct your own due diligence and consult a qualified financial advisor before making any investment decision. Position sizing guidelines are general in nature and do not account for individual circumstances, tax situations, or risk tolerance.