I've been watching the AI investment landscape closely since 2022, and here's what strikes me: most investors treat "AI" as a single trade. Buy Nvidia, maybe Microsoft, call it a day. But AI isn't one investment. It's an entire value chain - from the companies making the machines that make the chips, all the way up to the software running inference workloads for enterprise clients. And the risk/reward profile at each layer is completely different. Understanding that chain is the difference between intelligent AI exposure and just buying whatever ticker CNBC mentioned this morning.

This guide walks through the complete ecosystem. Hardware enablers, foundries, cloud platforms, pure-play AI companies, and the often-overlooked equipment and materials suppliers that make everything else possible.

Key Takeaway

The AI value chain spans five critical layers: semiconductor equipment, chip manufacturing, cloud infrastructure, platform services, and AI applications. Each layer has a distinct risk/reward profile and growth trajectory. The picks-and-shovels plays at the bottom of the stack often carry less risk than the pure-play names at the top - and many investors have this exactly backwards.

Understanding the Semiconductor Value Chain

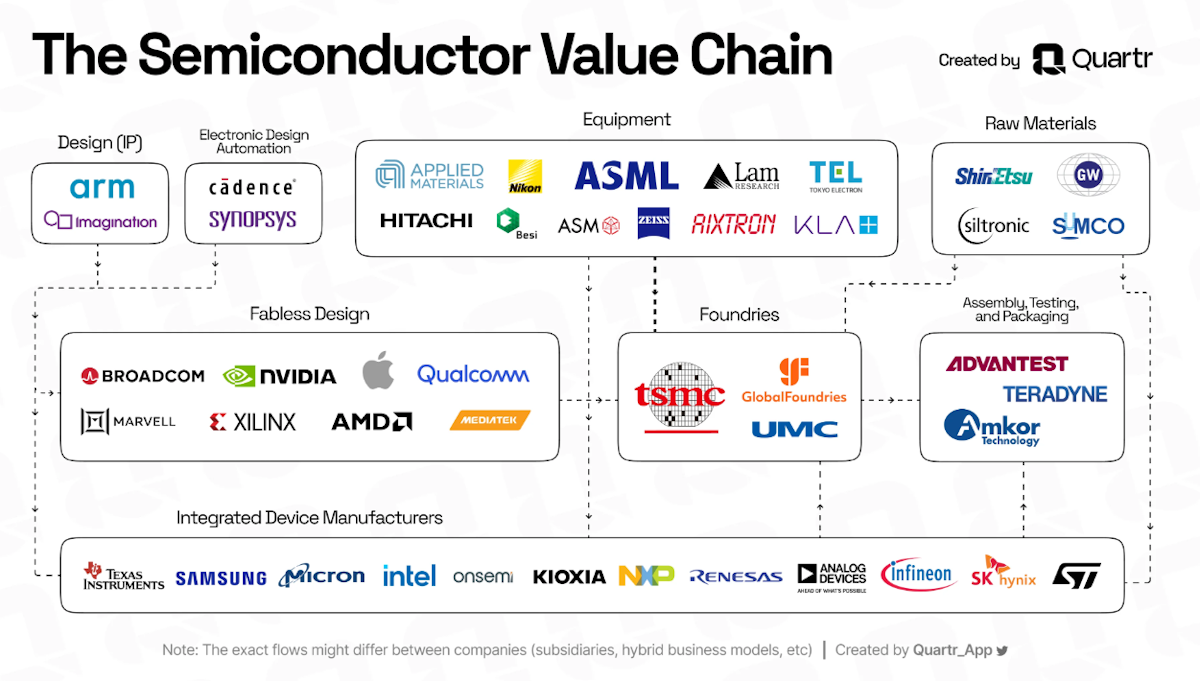

Everything starts with chips. No chips, no AI. The semiconductor value chain is more complex than most investors realise - dozens of specialised companies at each stage of production, many of them operating in what amounts to monopoly or duopoly positions. If you want to identify where the real pricing power sits in the AI buildout, this is the place to start looking.

Complete Semiconductor Value Chain: From Equipment to End Applications

The value chain flows through distinct stages:

- Equipment Manufacturers: Companies like ASML create the ultra-precise machinery needed to fabricate advanced chips

- Materials Suppliers: Providers of silicon wafers, photoresists, and specialty gases

- Chip Design: Fabless companies like NVIDIA and AMD that design but don't manufacture chips

- Foundries: Manufacturing specialists like TSMC and Samsung that produce chips for designers

- Testing & Packaging: Companies that verify chip functionality and prepare them for integration

- End Applications: Cloud providers, device manufacturers, and AI software companies

Layer 1: Chip Infrastructure - The Hardware Foundation

At the base of everything: the chip makers. These are the companies designing and manufacturing the silicon that powers AI training runs costing millions of dollars in compute, and the inference workloads that serve hundreds of millions of users daily. Three names dominate.

NVIDIA (NVDA)

Market Position: Dominant AI chip designer with 80%+ market share in AI training GPUs

Key Products: H100, A100, and upcoming Blackwell architecture GPUs designed specifically for AI workloads

Investment Thesis: First-mover advantage in AI-specific chips, strong software ecosystem (CUDA), and expanding into AI inference and edge computing

Risk Factors: High valuation multiples, increasing competition from AMD, custom chips from tech giants

Taiwan Semiconductor (TSMC)

Market Position: World's largest and most advanced chip foundry, manufacturing chips for NVIDIA, Apple, AMD, and others

Key Capabilities: Leading-edge 3nm and 2nm process technology, unmatched manufacturing expertise

Investment Thesis: Critical chokepoint in semiconductor supply chain, benefits from all AI chip demand regardless of designer

Risk Factors: Geopolitical tensions around Taiwan, massive capital expenditure requirements, customer concentration

ASML Holding (ASML)

Market Position: Monopoly provider of extreme ultraviolet (EUV) lithography systems essential for advanced chip manufacturing

Key Technology: EUV machines that cost $200M+ each, required for cutting-edge chip production

Investment Thesis: Irreplaceable technology, high barriers to entry, every advanced chip requires ASML equipment

Risk Factors: Export restrictions to China, long product development cycles, dependence on semiconductor capital spending

Layer 2: Platform Giants - Cloud Infrastructure Providers

The hyperscalers are the middlemen between the chip layer and the end user - they buy the hardware, build the data centres, and sell AI compute as a service. What makes them interesting as investments is that they benefit from AI demand regardless of which specific AI model or application wins. They're selling the shovels and the land. Here are the three that matter most.

Microsoft (MSFT)

AI Strategy: Deep partnership with OpenAI, Azure AI services, Copilot integration across product suite

Competitive Advantages: Enterprise relationships, Azure cloud infrastructure, Office/Windows distribution channels

AI Revenue Exposure: Azure AI growing 50%+ annually, Copilot monetization beginning, GitHub Copilot proving enterprise AI demand

Investment Case: Best positioned mega-cap for AI enterprise adoption, diversified revenue base reduces risk

Alphabet/Google (GOOGL)

AI Capabilities: DeepMind research, custom TPU chips, Gemini AI models, Bard chatbot

Infrastructure: Google Cloud Platform with AI/ML services, massive internal AI deployment (Search, YouTube, Maps)

Strategic Position: Leading AI research organization, vast proprietary data for model training

Key Risk: Search disruption from AI chatbots, regulatory scrutiny, slower enterprise cloud market share gains

Amazon (AMZN)

Cloud Leadership: AWS dominates with 32% cloud market share, offering comprehensive AI/ML tools

AI Products: Bedrock foundation model service, custom Trainium/Inferentia chips, Amazon Q assistant

Unique Assets: E-commerce data for AI training, logistics optimization AI, Alexa voice platform

Investment Angle: AI accelerates AWS growth, cost optimization opportunities across retail operations

Layer 3: Equipment & Materials Suppliers

This is the part of the AI value chain that most retail investors ignore entirely - and it's arguably the most defensible. Behind every advanced chip sits a web of specialised equipment and materials suppliers, many of them operating in narrow markets with almost no competition. These companies don't get the headlines, but they have the margins.

Key Equipment Categories

- Lithography: ASML (EUV), Nikon, Canon (DUV systems)

- Deposition: Applied Materials, Lam Research (thin film creation)

- Etching: Lam Research, Tokyo Electron (pattern transfer)

- Metrology: KLA Corporation (inspection and measurement)

- Materials: Shin-Etsu, SUMCO (silicon wafers), JSR, Tokyo Ohka (photoresists)

What makes these businesses attractive from an investment perspective:

- Long-term secular growth in chip demand driven by AI

- High switching costs and technological moats

- Recurring revenue from service contracts and consumables

- Expansion as foundries build new advanced fabrication facilities

Layer 4: Pure-Play AI Companies & ETFs

If you want exposure to AI beyond the chip and cloud giants, the pure-play space is where things get both more exciting and more dangerous. These are smaller companies whose entire business model depends on AI adoption scaling. The upside is enormous when it works. The downside is that many of these names are still proving their business models, and a growth miss can send the stock down 30% in a session.

Individual AI Stocks

C3.ai (AI)

Focus: Enterprise AI software applications for predictive maintenance, fraud detection, supply chain optimization

Status: High-growth, unprofitable, significant revenue volatility

Palantir Technologies (PLTR)

Focus: Data analytics and AI platforms for government and commercial clients

Strengths: Strong government relationships, increasing commercial adoption, profitable business model

SentinelOne (S)

Focus: AI-powered cybersecurity and threat detection

Growth: Rapid customer acquisition, high revenue growth, path to profitability

AI-Focused ETFs

If picking individual AI stocks feels like too much single-name risk (and frankly, it should for most people), ETFs offer diversified exposure across the theme:

- Global X Robotics & AI ETF (BOTZ): Broad exposure to automation and AI companies

- ARK Autonomous Tech & Robotics ETF (ARKQ): Active management focusing on disruptive AI technologies

- iShares Robotics and AI ETF (IRBO): Global AI and robotics companies

- Roundhill Generative AI & Technology ETF (CHAT): Focused on generative AI beneficiaries

ETF Considerations

Watch out for overlap. Many AI ETFs are heavily weighted toward Nvidia, Microsoft, and Google - names you may already own through a standard S&P 500 index fund. If you add an AI ETF on top of VOO, you might be doubling down on the same five stocks without realising it. Always check the top 10 holdings before buying.

Layer 5: Supply Chain - Fabrication, Design, Testing, Packaging

Between the raw silicon and the finished AI chip, there are dozens of specialised steps - and each one represents a potential investment opportunity. Some of these companies are invisible to most investors but absolutely critical to the supply chain.

Chip Design Tools (EDA - Electronic Design Automation)

- Synopsys (SNPS): Leading chip design software, essential for complex AI chip development

- Cadence Design Systems (CDNS): Complementary design tools, strong in custom chip design

Foundry Services

- TSMC: Premium foundry, cutting-edge processes

- Samsung Foundry: Second-tier advanced node competitor

- GlobalFoundries (GFS): Mature node specialist, less exposed to AI but stable

Testing & Assembly

- Amkor Technology (AMKR): Outsourced assembly and test (OSAT) leader

- ASE Technology: Largest OSAT provider globally

Investment Strategy Framework

How you structure AI exposure depends entirely on your risk appetite. Here are two frameworks - not prescriptions, but starting points for thinking about allocation across the value chain:

Risk-Adjusted Strategy

Conservative (Lower Risk):

- 40% Platform Giants (Microsoft, Google, Amazon)

- 30% Semiconductor Infrastructure (TSMC, ASML)

- 20% Chip Designers (NVIDIA, AMD)

- 10% AI-focused ETFs

Aggressive (Higher Risk/Reward):

- 30% NVIDIA/AMD

- 25% Equipment suppliers (ASML, Applied Materials)

- 25% Pure-play AI software (C3.ai, Palantir)

- 20% Emerging AI startups (via venture-focused funds)

Key Considerations for AI Investors

1. Valuation Discipline

This is where most AI investors get themselves in trouble. The narrative is so compelling that people forget to check the price tag. Many AI stocks trade at multiples that require everything to go right for a decade. Focus on companies with:

- Proven revenue growth from AI products (not just announcements)

- Clear path to profitability or existing strong margins

- Competitive moats (technology, scale, or network effects)

2. Timeline Alignment

Not every AI investment pays off on the same schedule. The hardware layer is benefiting right now. The application layer might take years to produce consistent winners. Make sure your investment horizon matches the layer you're buying:

- Already benefiting: NVIDIA, TSMC, cloud providers

- Near-term (1-2 years): Enterprise AI software, AI-enhanced productivity tools

- Long-term (3+ years): Autonomous vehicles, robotics, scientific discovery applications

3. Diversification Across Layers

Don't put all your AI exposure in one layer. If you're 100% in chip designers and the semiconductor cycle corrects, your entire AI thesis gets punished even though AI adoption itself is still accelerating. Spread across equipment, chips, cloud, and applications. The AI revolution will produce winners at every level - but betting on which specific company wins at any single level is harder than most people think.

Risk Management

Key Risks to Monitor:

- Valuation Compression: High P/E ratios vulnerable if growth disappoints

- Competition: Rapidly evolving landscape with new entrants constantly emerging

- Geopolitical: Trade restrictions, especially involving China and Taiwan

- Technology: Risk of technological disruption or commoditization

- Regulation: Potential AI safety regulations impacting deployment

Conclusion: Building Your AI Investment Portfolio

AI is a multi-decade investment opportunity. That part of the thesis I'm confident about. What I'm less confident about is which specific companies at which layers will be the long-term winners - and anyone who tells you they know with certainty is selling you something. The smart approach: understand where value gets created at each layer, spread your exposure across the chain, and size positions based on what the earnings actually justify rather than what the narrative suggests.

Action Steps

- Start with Infrastructure: Consider positions in NVIDIA, TSMC, or Microsoft as core AI holdings

- Add Diversification: Layer in equipment suppliers (ASML) or AI ETFs for broader exposure

- Size Appropriately: Limit individual AI stocks to 3-5% of portfolio given volatility

- Rebalance Regularly: Take profits on winners, add to underperformers with strong fundamentals

- Stay Informed: AI landscape evolves rapidly; monitor earnings, product launches, and competitive dynamics

The companies building AI infrastructure today - from the equipment makers to the chip foundries to the cloud platforms running inference at scale - are positioned to capture enormous value over the coming decade. But "positioned to capture value" and "currently priced to capture value" are two very different statements. The best AI investments will be the ones where the market hasn't fully appreciated the earnings power yet. Those tend to be lower in the stack - the equipment makers, the materials suppliers, the less glamorous names with genuine monopoly positions and decades-long order backlogs. Keep looking there.

Disclaimer: This article is for educational purposes only and should not be considered investment advice. AI investments carry significant risks, including valuation volatility, technological disruption, and competitive threats. Always conduct thorough research and consult with financial advisors before making investment decisions.

Research, PolyMarket Investment Strategies, January 2026