People love attributing the "eighth wonder of the world" quote to Einstein. He almost certainly never said it. But the math behind compounding doesn't need a celebrity endorsement - it's the most powerful force in personal finance, and most people don't fully grasp it until they've either benefited from it for decades or, worse, missed it entirely.

Here's the fact that blew my mind when I first encountered it: Warren Buffett has accumulated over $100 billion in wealth. More than 99% of it arrived after his 50th birthday. Same strategy the entire time. He didn't suddenly get smarter at 50. Compounding just finally hit the steep part of the curve. The first few decades were the slow, boring foundation. The last few were the payoff - and the payoff was absurd.

This guide walks through exactly how compounding works, the mental shortcuts that make the math intuitive, why fees and taxes are quietly destroying your returns (and what to do about it), and which accounts actually let compounding run at full speed. Whether you're 22 and just opened your first brokerage account or 42 and wondering if you've waited too long - you haven't. But every month you keep waiting costs more than you think.

Simple vs. Compound Interest: The Fundamental Difference

This is the single most important concept in personal finance. Not budgeting. Not stock picking. The difference between simple and compound interest. And it comes down to one word: reinvestment.

Simple Interest - Flat Returns

Simple interest pays you only on the original amount you put in. That's it. $10,000 at 5% earns $500 in year one. $500 in year two. $500 in year thirty. The same flat check, forever. Your balance grows in a straight line - predictable, sure, but also painfully limited. It's like getting a raise that never compounds. You're always earning on the same base.

Compound Interest - Exponential Returns

Compound interest takes what you earned last year and rolls it back into the pot. So in year two, you're earning 5% on $10,500 - not $10,000. Year three? You're earning on $11,025. Each year the base gets bigger, and the growth curve starts bending upward. Slowly at first. Then not slowly at all.

The Difference in Numbers: $10,000 at 7% Over 30 Years

Simple interest: $10,000 + ($700 × 30) = $31,000

Compound interest (annual): $10,000 × (1.07)30 = $76,123

Same starting amount. Same interest rate. Same number of years. And compound interest produced $45,123 more - money that came from absolutely nowhere except reinvestment. Stretch that to 40 years at 8% and the gap balloons to several hundred thousand dollars. That's the whole game right there.

The Three Drivers of Compounding

Three variables control compounding. Just three. But understanding how they interact - and which one you actually have control over - changes everything about how you approach investing.

1. Rate of Return - The Engine

The annual return is the fuel. And even tiny differences in return rate produce wildly different outcomes over long periods - this is the part that's hard to internalize until you see the numbers. A 1% difference in annual return on $100,000 over 30 years? That's not a rounding error. It's more than $175,000 in different outcomes. Which is exactly why fees matter so much. Every basis point your fund charges is a basis point that doesn't compound for you. It compounds for them.

2. Time Horizon - The Multiplier

This is the variable people underestimate the most and regret the most. Here's the counterintuitive part: the last decade of a 40-year compounding journey generates more wealth than the first 30 years combined. The curve starts almost flat and ends almost vertical. So every year you delay isn't a year lost from the gentle beginning - it's a year stolen from the explosive end.

Vanguard's research puts hard numbers on this: starting at 25 versus 35, with identical total contributions, produces a retirement portfolio that is 50-60% larger. The early years don't look impressive on a statement. They're the foundation that makes everything after year 25 possible.

3. Reinvestment - The Mechanism

None of this works if you pull money out. Every dividend you spend, every interest payment you pocket, every capital gain you withdraw - that's a broken link in the chain. Gone. The simplest fix? Set up a DRIP (dividend reinvestment plan) on every holding and forget about it. Each quarterly payout automatically buys more shares, which generate more payouts, which buy more shares. In a tax-advantaged account there's no tax hit on reinvestment either, so the engine runs at full speed with zero drag.

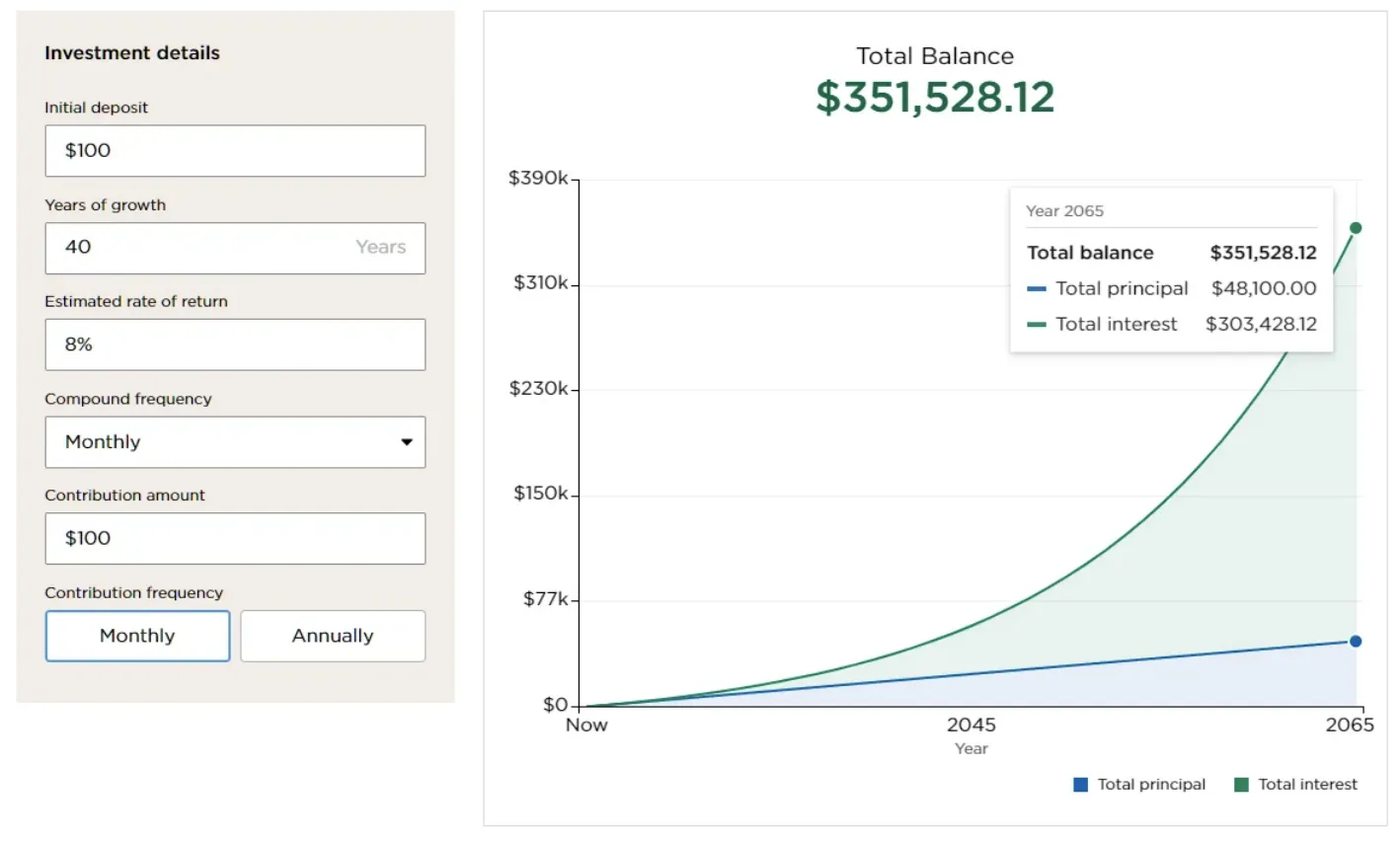

The Power of Time: What $100/Month Actually Becomes

Talking about compounding in the abstract doesn't land. You need to see the actual numbers - and this table is the one that usually makes people's eyes go wide. It's based on a $100 starting deposit plus $100 per month at 8% annual return (roughly what the S&P 500 has delivered historically).

| Years Invested | Your Total Contributions | Balance at 8% Return | Market Growth |

|---|---|---|---|

| 2 years | $2,400 | ~$2,700 | +$300 |

| 5 years | $6,000 | ~$7,500 | +$1,500 |

| 10 years | $12,000 | ~$18,000 | +$6,000 |

| 20 years | $24,000 | ~$54,000 | +$30,000 |

| 30 years | $36,000 | ~$150,000 | +$114,000 |

| 40 years | $48,000 | ~$350,000 | +$302,000 |

Read that last row again. You put in $48,000 over forty years. Your balance is $350,000. 86% of that money was created by the market, not by you. You didn't earn it at a job. You didn't inherit it. The math just... did it. And look at the chart below - you can actually see the curve go from barely noticeable to almost vertical in the final decade.

See how the line barely moves for the first 15 years? Then gently climbs for the next 10? Then goes almost vertical in the final stretch? That shape is the signature of exponential growth. And it explains something I keep coming back to: the most important investing decision most people will ever make isn't which stock to buy or which fund to pick. It's just starting. The math handles the rest if you give it enough time.

Why Rate of Return Is Everything

If compounding is an engine, the return rate is the horsepower. And what most people don't realize is how dramatically small differences in annual return separate outcomes over 40 years. Same $100 initial deposit, same $100/month - watch what the rate alone does:

| Annual Return | Balance After 40 Years | Typical Source | Note |

|---|---|---|---|

| 2% | ~$49,000 | Bank savings account (2026) | Barely beats inflation |

| 8% | ~$350,000 | S&P 500 index fund (historical avg) | Gold standard baseline |

| 15% | ~$3,100,000 | Skilled stock selection | Very few achieve this consistently |

Let that sink in. The gap between 2% and 8% - achievable by literally moving money from a bank savings account into a broad index fund - is $301,000 over 40 years. On the same $100/month contribution. The where-you-invest decision is worth more than how-much-you-invest by a factor of six. And yet people obsess over saving an extra $50/month while leaving their existing savings in an account earning next to nothing.

The Rule of 72: Your Mental Compounding Calculator

This is the one trick I use more than any other. It's a napkin-math shortcut that tells you how long it takes to double your money at any given return rate. You can do it in your head at dinner.

How It Works

Take the number 72. Divide it by your expected annual return. That's roughly how many years until your money doubles. Dead simple.

| Annual Return | Years to Double | Investment Vehicle |

|---|---|---|

| 2% | 36 years | Bank savings account |

| 4% | 18 years | High-yield savings / short-term CDs |

| 6% | 12 years | Conservative 60/40 portfolio |

| 8% | 9 years | S&P 500 index fund (long-run average) |

| 10% | 7.2 years | S&P 500 strong-decade scenario |

| 12% | 6 years | High-quality growth portfolio |

But here's where the Rule of 72 gets really interesting - flip it around to measure the damage fees do. A fund charging 1% per year? 72 divided by 1 equals 72 years. That's the doubling time of the fee drag. At 2% annual fees, your wealth gets effectively halved (relative to a zero-fee alternative) every 36 years. "Small" fees aren't small. They're compounding against you just as relentlessly as returns compound for you.

The 8-4-3 Rule: How Compounding Accelerates Over Time

This framework makes the "back-loaded" thing I keep talking about actually visible. Take a 15-year investment window and break it into three phases. Each phase gets shorter. Each phase produces more wealth than the one before it. That's the whole point - and it's why patience in the early years pays off so dramatically.

Based on $20,000 initial investment + $1,000/month contributions at 10% annual return.

What This Tells You About When to Start

The takeaway is almost annoyingly simple: you can't skip to the good part. Without those 8 boring foundation years, there's no acceleration. Without acceleration, the exponential phase never materializes. The person who looks at their portfolio after 3 years, decides "this isn't doing anything," and stops contributing? They just walked away from 90% of the wealth they would have built.

And this is why pulling money out of a long-running portfolio is so destructive. That dollar you withdraw isn't just one dollar gone. It's that dollar's entire future compounding trajectory - years 9 through 40 of growth - that you've just erased. Every withdrawal is an amputation of future wealth you'll never see.

The Fee Trap: How Costs Silently Destroy Compound Growth

Nobody sends you a bill that says "here's what fees cost you this decade." That's the problem. Fees work silently - shaving a little off your return each year, compounding that loss over decades, until the total damage is staggering. And most investors have no idea it's happening.

| Fee Scenario | Value After 30 Years | Total Fees Paid |

|---|---|---|

| 0.1% annual fee (index fund) | $9,786,859 | $275,798 |

| 0.5% annual fee (managed fund) | $8,754,944 | $1,307,701 |

| Difference (cost of 0.4% extra fee) | −$1,031,915 | +$1,031,903 |

Based on a $1,000,000 initial portfolio, 8% gross annual return, compounded over 30 years.

Read that again. A 0.4% difference in annual fees - the kind of difference you'd barely notice on a fund comparison page - costs over $1 million on a $1M portfolio over 30 years. The fee isn't just eating your principal. It's eating every dollar that principal would have generated. And every dollar those dollars would have generated. Fees compound against you with the same mathematical ferocity that returns compound for you. That's the part nobody tells you at the fund pitch meeting.

Three Rules to Protect Your Compounding from Fees

Use low-cost index funds. Period. Broad-market ETFs from Vanguard, Fidelity, and Schwab charge 0.03-0.10% per year. There is zero research justification for paying 10x that to a fund manager who, statistically, will underperform the index anyway. The data on this is overwhelming and has been for decades.

Never pay a load fee. Some mutual funds charge 1-5% upfront just to buy in - a "sales commission" that vanishes before your money even starts compounding. If someone tries to sell you a load fund, thank them and walk away. Quickly.

Stop trading so much. Every buy and sell generates transaction costs and capital gains taxes. Both reduce the effective return feeding your compounding engine. The best investors are boring investors. They buy, they hold, they let the math work.

Compounding Account Types: From Safe to Growth

Not all accounts compound the same way. The rate, the frequency, the risk, the tax treatment - all different. And putting money in the wrong type of account for its purpose is one of the most common (and most expensive) mistakes people make. Here's the landscape.

| Account Type | Typical APY (2026) | Risk Level | Best For |

|---|---|---|---|

| High-Yield Savings Account | 4.0–4.5% | None (FDIC-insured) | Emergency fund, short-term goals; access anytime |

| Money Market Account | 4.0–4.5% | None (FDIC-insured) | Higher rates than standard savings + limited check access |

| Certificate of Deposit (CD) | 4.5–5.0% (12-mo) | None (FDIC-insured) | Locked funds for 6 months–5 years; guaranteed rate |

| Series I Savings Bonds | Varies (inflation-linked) | None (government-backed) | Inflation protection; must hold 1 year; $10K/year limit |

| Roth IRA (invested in index ETFs) | ~8–10% long-run (market-based) | Market risk | Tax-free compound growth for 10+ year horizons |

| 401(k) / Traditional IRA | ~8–10% long-run (market-based) | Market risk | Tax-deferred compounding; employer matching accelerates growth |

| Dividend Stocks (DRIP enabled) | Varies (dividend yield + price appreciation) | Market risk | Compound through reinvested dividends; long-term hold |

Which Account for Which Purpose?

Emergency fund (3-6 months expenses): High-yield savings account. You need access more than you need maximum return here - but earning 4%+ on your safety net is a lot better than the 0.06% your traditional bank is offering. Check the rate on your current account. If it starts with a zero, move it today.

Money you'll need in 1-3 years: CD ladder. Lock in today's rates across 1-year, 2-year, and 3-year terms. You stagger your access dates and guarantee the yield. It's not exciting. That's the point.

Long-term wealth building (10+ years): Roth IRA and 401(k), invested in broad-market index ETFs. The combination of market returns, minimal fees, and tax-free or tax-deferred compounding is the most powerful wealth-building engine available to a normal person. Full stop. If you do nothing else from this entire guide, do this.

Income-focused investing: Dividend stocks with DRIP turned on. Each reinvested dividend buys fractional shares. Those shares pay more dividends. Those dividends buy more shares. It's a flywheel that gets stronger every quarter - and over decades, the acceleration is remarkable.

Tax Efficiency: The Silent Multiplier of Compounding

If fees are compounding's quiet enemy, taxes are its louder cousin. Every time the IRS takes a cut of your dividends, interest, or capital gains, that's money that doesn't get reinvested. And the compounding loss on taxed-away earnings adds up to a genuinely shocking amount over 30 years.

The Tax-Deferred Compounding Advantage

In a regular taxable brokerage account, every dividend, every interest payment, every realized capital gain triggers a tax event in the year it happens. If you're reinvesting a 3% dividend but the government takes 20% of it first, you're really only reinvesting 2.4%. That 0.6% gap doesn't sound like much. Over 30 years it's enormous.

In a Roth IRA? That same dividend gets reinvested at the full 3%. No tax. No drag. After three decades, identical investments in different account types produce wildly different balances - and the only difference is the tax wrapper. Same stocks, same dividends, completely different outcomes. It's one of the most straightforward free lunches in all of finance.

The 2026 Tax-Advantaged Priority List

If you can't fund everything at once (and most people can't), this is the order that maximizes your tax-sheltered compounding:

- 401(k) up to the employer match - your employer is literally giving you free money. A 100% match is a 100% instant return before compounding even starts. Not capturing the full match is the financial equivalent of leaving cash on the table. Actual cash.

- Roth IRA ($7,000/year limit in 2026) - tax-free growth and tax-free withdrawals in retirement. Best choice if you expect your tax bracket to be higher later than it is now, which most young earners should.

- Max out the 401(k) ($23,500/year) - tax-deferred compounding on every dollar contributed. The tax savings today are real. The compounding advantage over 30 years is even more real.

- Taxable brokerage - for everything beyond tax-advantaged limits. Use tax-efficient vehicles here: broad-market index ETFs that generate minimal taxable distributions. Don't put a REIT in a taxable account if you can help it.

Asset Location: What Goes Where

This is the optimization most people never think about, and it's worth a lot of money. Same investments, different accounts, very different tax outcomes. Tax-inefficient assets - bond funds, REITs, high-dividend stocks that throw off constant taxable income - belong inside your Roth IRA or 401(k) where that income doesn't get taxed annually. Tax-efficient assets like broad-market stock ETFs work fine in taxable accounts because they generate minimal annual distributions. Getting this "asset location" right can add 0.5-1.0% per year to your effective after-tax return. Compound that edge over decades and you're looking at a six-figure difference in retirement wealth. For doing nothing more than putting things in the right bucket.

The Rate Environment in 2026

After the Fed's aggressive rate hike cycle in 2022-2023, rates have started drifting back down - but they're still historically attractive compared to the near-zero wasteland of 2015-2021 when your savings account earned roughly the price of a coffee per year on ten grand.

Where Things Stand Right Now

High-yield savings accounts at online banks (Marcus, Ally, SoFi) are still paying around 4.0-4.5% APY. Traditional banks? Most are offering 0.06%. That's not a typo. The gap is 70-80x. If you have cash sitting in a traditional savings account and haven't moved it yet, you're leaving real money on the table every single month. It takes about 15 minutes to open an online savings account. Do it.

CD rates are holding at 4.5-5.0% for 12-month terms. If you've got cash you won't touch for 6-18 months, locking in today's yield via a short CD ladder makes sense - especially if you think rates will keep falling. Once they drop, you can't go back and capture what's available right now.

For long-term investors - and this is important - none of this rate chatter matters much. The long-run expected return on equities (7-10%) still dwarfs any savings account by a wide margin. Today's elevated savings rates are a nice bonus for your emergency fund and short-term cash. They don't change the fundamental math of equity compounding one bit. If your horizon is 10+ years, you should be in the market, not chasing an extra half-percent in a savings account.

Five Rules to Maximise Compounding - and Five Mistakes That Destroy It

The Five Rules

1. Start now. Not next month. Not when you "have more to invest." Now. Time is the one variable you cannot get back. $50/month starting today beats $200/month starting three years from now. Every. Single. Time. The math is unforgiving on this point.

2. Don't interrupt the process. Selling investments or pulling out returns resets the compounding clock to zero on those dollars. Build a separate emergency fund for exactly this reason - so you never, ever have to crack open your long-term compounding positions to pay for a car repair or a medical bill.

3. Reinvest everything. Dividends, interest, capital gains distributions - all of it goes back in. Turn on DRIP for every holding. In a tax-advantaged account, reinvestment is free and automatic. Don't touch it. Don't "take a little off the table." Let the flywheel spin.

4. Hunt down every unnecessary cost. Fees and taxes compound against you with the exact same mathematical force that returns compound for you. A 0.1% reduction in annual costs translates to genuinely meaningful wealth over a 30-year horizon. Check your expense ratios today. I'm serious.

5. Automate it and forget about it. Set up automatic monthly transfers from your checking account into your investment accounts. The goal is to remove your own willpower from the equation entirely. Humans are terrible at remembering to do boring-but-important things consistently. Automation fixes that. As a bonus, dollar-cost averaging smooths your entry price over time.

Five Mistakes That Destroy Compound Growth

1. Leaving long-term money in low-yield accounts. Retirement savings sitting in a bank account earning 0.5% while inflation runs at 3% means you are getting poorer every year. Your balance goes up. Your purchasing power goes down. The account type matters as much as the amount saved - probably more.

2. Not knowing what you're paying in fees. Most investors can't tell you their fund's expense ratio. A 1% fee on a $500,000 portfolio costs $5,000 per year in direct charges alone - and that's before you compound the lost returns on those fees over the next 20 years. Pull up every fund you own right now. Check the expense ratio. Compare it to the cheapest equivalent index fund. I guarantee you'll find something to fix.

3. Selling in a panic. Panic-selling during a downturn converts a temporary paper loss into a permanent real loss and kills compounding dead. The people who sold everything in March 2020 when the market dropped 34%, then waited six months for things to "feel safe" before buying back in? They missed most of the recovery and locked in far worse outcomes than the investors who did literally nothing. Doing nothing was the optimal strategy.

4. Waiting for the "right time." The best time to invest was 20 years ago. The second-best time is today. Waiting for a correction, waiting for the election to be over, waiting for rates to stabilize, waiting for "things to calm down" - historically, you miss more upside waiting than you avoid in downside. Time in the market beats timing the market. It's a cliche because it is relentlessly, boringly true.

5. Believing your amount is "too small to matter." This one kills me. The single greatest barrier to compounding isn't math, it's psychology - the belief that $50 or $100 per month is too insignificant to bother with. $100/month at 8% for 40 years becomes $351,000. That's a small fortune built from pocket change. Start small. Stay consistent. The math doesn't care about your feelings of inadequacy. It just works.

PolyMarket Investment, Research Team, June 2025