There is a phrase appearing in every serious research report on energy written this year: the new energy security age. It is not hyperbole. It marks a genuine inflection point - a moment when the old rules of global energy stopped applying and something more complex, more contested, and more consequential took their place.

For most of the post-war era, energy was primarily an economic question. Countries bought what was cheap, sold what they had, and left the politics to diplomats. That world is gone. Today, energy is national security. The cables, pipes, mines, and processing plants that produce and move energy are now treated as strategic assets - to be defended, onshored, or denied to rivals. Beijing's export controls on graphite and gallium. Washington's Inflation Reduction Act. Brussels pledging to purchase $750 billion in U.S. energy exports through 2028. These are not trade disputes. They are moves on a geopolitical chessboard.

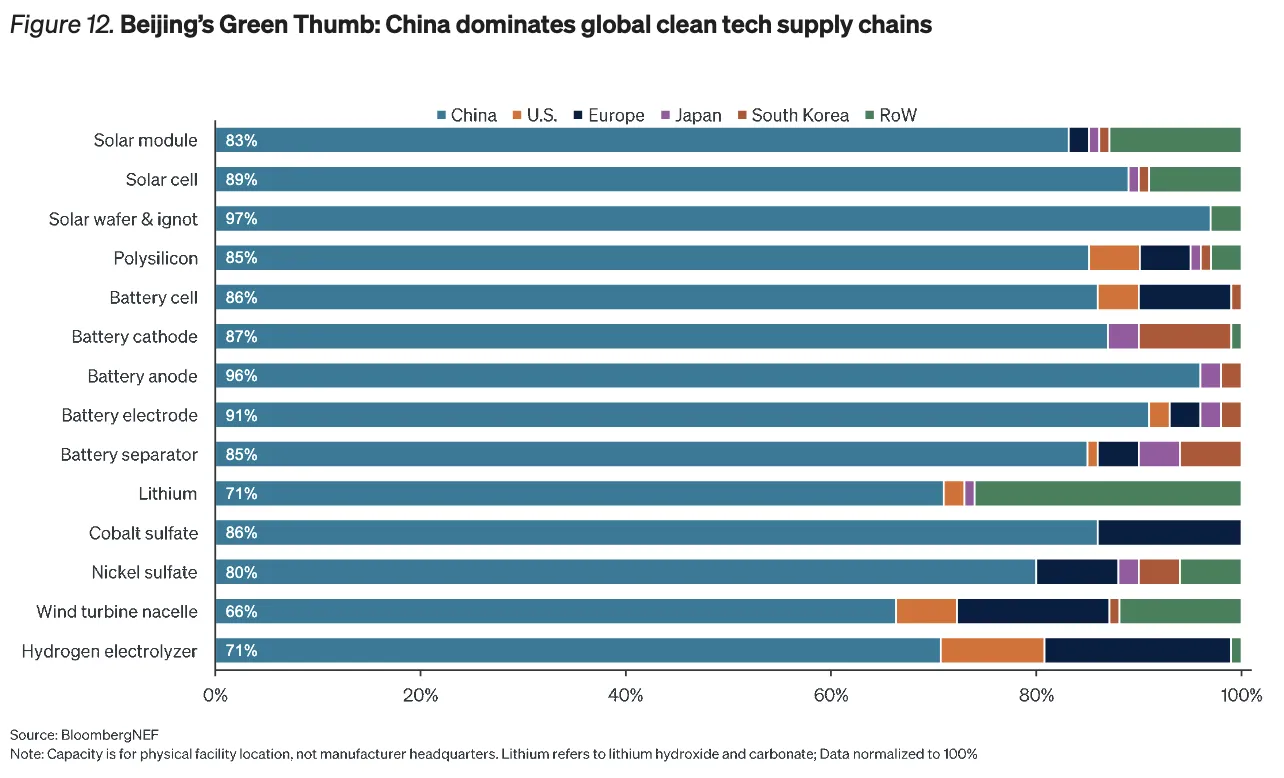

This course teaches you to read that chessboard. You will learn why geography still dictates competitive advantage in energy - and which nations hold the strongest hands. You will understand why China controls 83–97% of solar manufacturing despite not being the sunniest place on Earth. You will see how OPEC+'s production gambits interact with U.S. shale arithmetic. And you will leave with a clear investment framework for positioning across the volatility this age creates. Energy is no longer just a commodity. It is the currency of geopolitical power.

The Uneven Energy Chessboard

No energy source is universal. Geography still dictates strategic advantage - and disadvantage. Countries and regions have different competitive edges in natural resources. The race for energy self-sufficiency is being driven by artificial intelligence's voracious appetite for power, by conflict shocks, and by access to capital. Nations are now surveying every resource they have and asking: how do we play this hand?

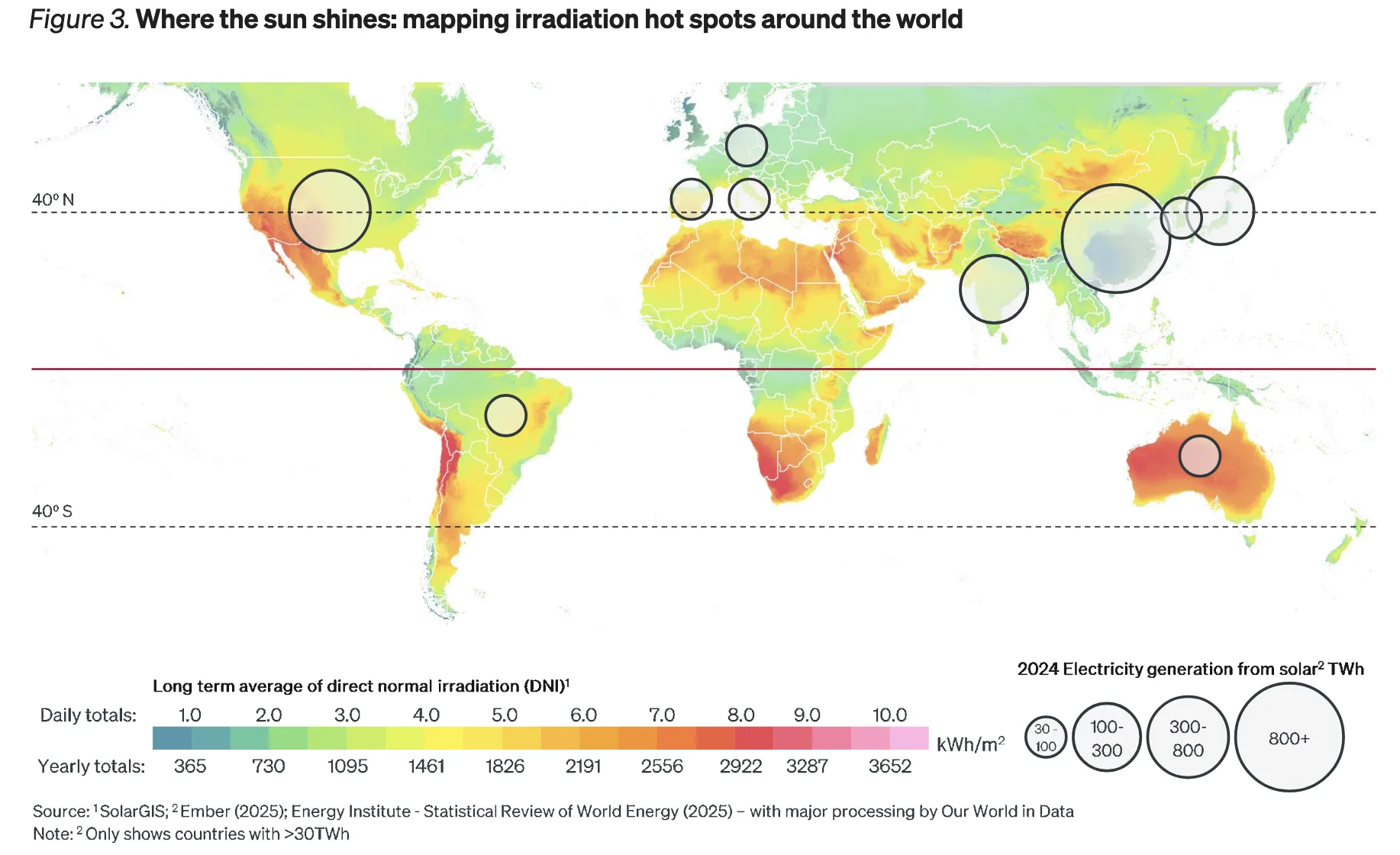

Solar irradiation - the measure of how strongly the sun shines at Earth's surface - is not distributed evenly across the globe. Due to cloud coverage at the equator and reduced annual sunlight near the poles, maximum solar potential is concentrated across two narrow bands of latitude that experience minimal cloud cover. This means well-optimised solar projects are particularly suited to the American Southwest, central Mexico, Chile, Bolivia, the northern and southern bands of Africa, and Australia.

Even traditionally rich petro-states are taking advantage of their geography's unique disposition for solar. In 2025, Saudi Arabia signed $8.3 billion worth of deals for five massive solar farms and two wind farms, together totalling approximately 15 gigawatts of new renewable capacity. Meanwhile China and India have drawn the most recent solar investment, despite not sitting squarely in the top irradiation bands - proof that policy ambition and manufacturing scale can partially overcome geographic disadvantage.

| Energy Source | Geographic Sweet Spot | Key Constraint | Investment Signal |

|---|---|---|---|

| Solar | US Southwest, Chile, N/S Africa, Australia | Intermittency; storage required | FSLR, utility-scale developers |

| Wind (onshore) | Northern Europe, US Great Plains, China coast | Land use; transmission distance | Turbine makers, grid operators |

| Wind (offshore) | North Sea, US Northeast, NE China coast | Ocean depth; cable cost | ENPH, Orsted, grid infrastructure |

| Geothermal | W. USA, Iceland, Indonesia, Kenya; now expanding via deep drilling | Site-specific; exploration risk | Fervo Energy; US/Mexico advantage |

| Fossil Fuels | Middle East, North America, Russia | Transition headwinds; carbon cost | CVX, XOM, SLB for cash yield |

| Critical Minerals | Australia (lithium, cobalt, REE); DRC; Chile | Processing chokepoints (China) | MP Materials, Lynas, Li-Cycle |

Wind, Geothermal & the Drilling Revolution

Wind and geothermal tell a different geographic story from solar - and together they help diversify the map of national energy advantage in ways that pure solar analysis misses.

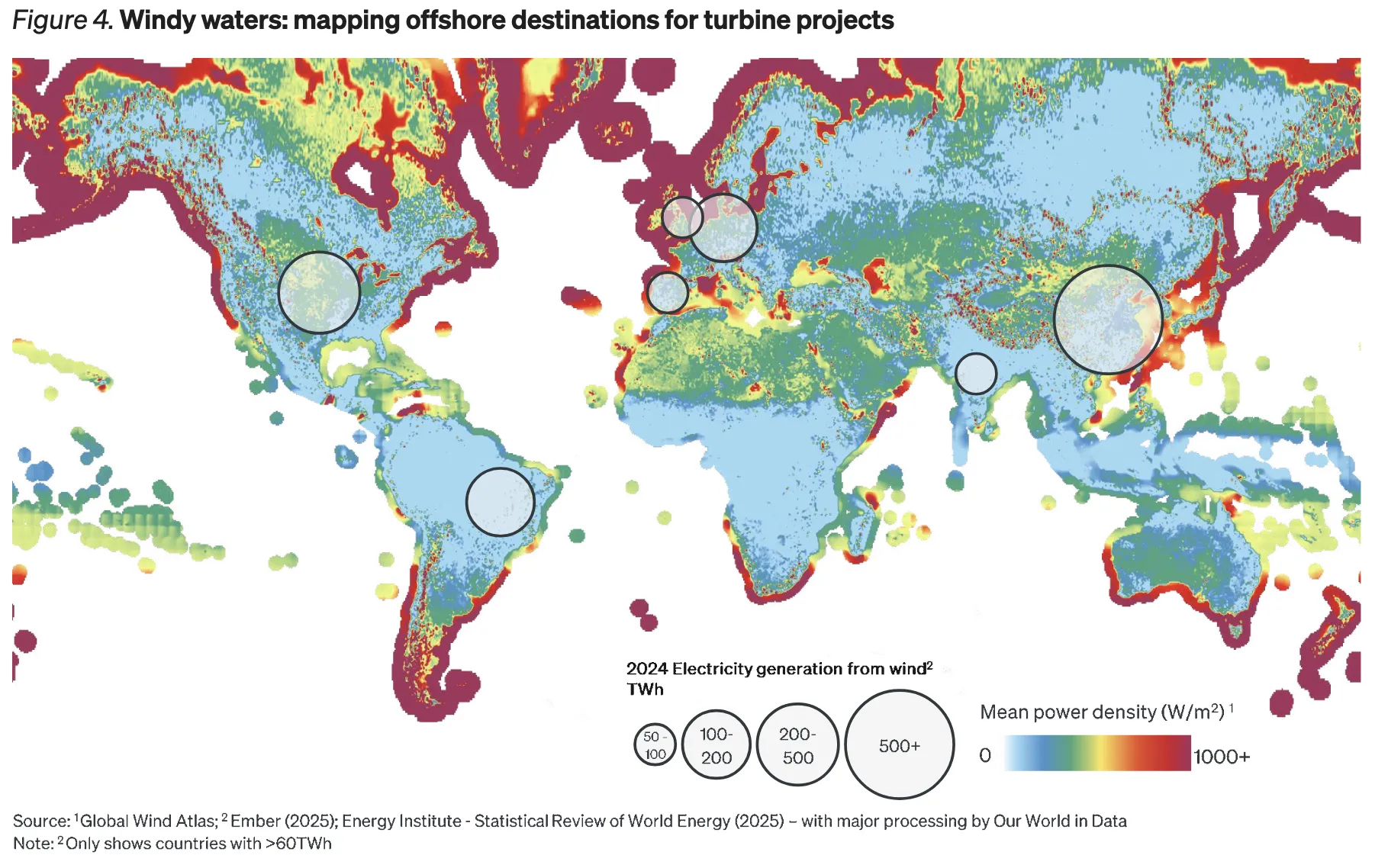

Wind strength is concentrated at both the northern and southern poles and along coastal waters - the mirror image of the solar irradiation map. Countries that lack reliable solar irradiation can often compensate with wind. Northern Europe is the clearest example: a consortium of North Sea nations are exploring the creation of artificial islands and "wind parks" in the Dogger Bank portion of the North Sea to harvest that region's high and consistent wind speeds. Shallow coastal shelf waters, where historic oil and gas infrastructure has already de-risked construction and operation, give the North Sea, Southern Australia, and North America structural advantages in offshore wind.

China has exploited its wind advantage more aggressively than any other nation. In 2024 alone, China added approximately 80 gigawatts of new wind capacity, bringing its total to roughly 520 GW - the most installed wind capacity globally, accounting for 10% of China's electricity generation. The United States ranked second with about 150 GW of installed capacity; Germany stood third at approximately 73 GW.

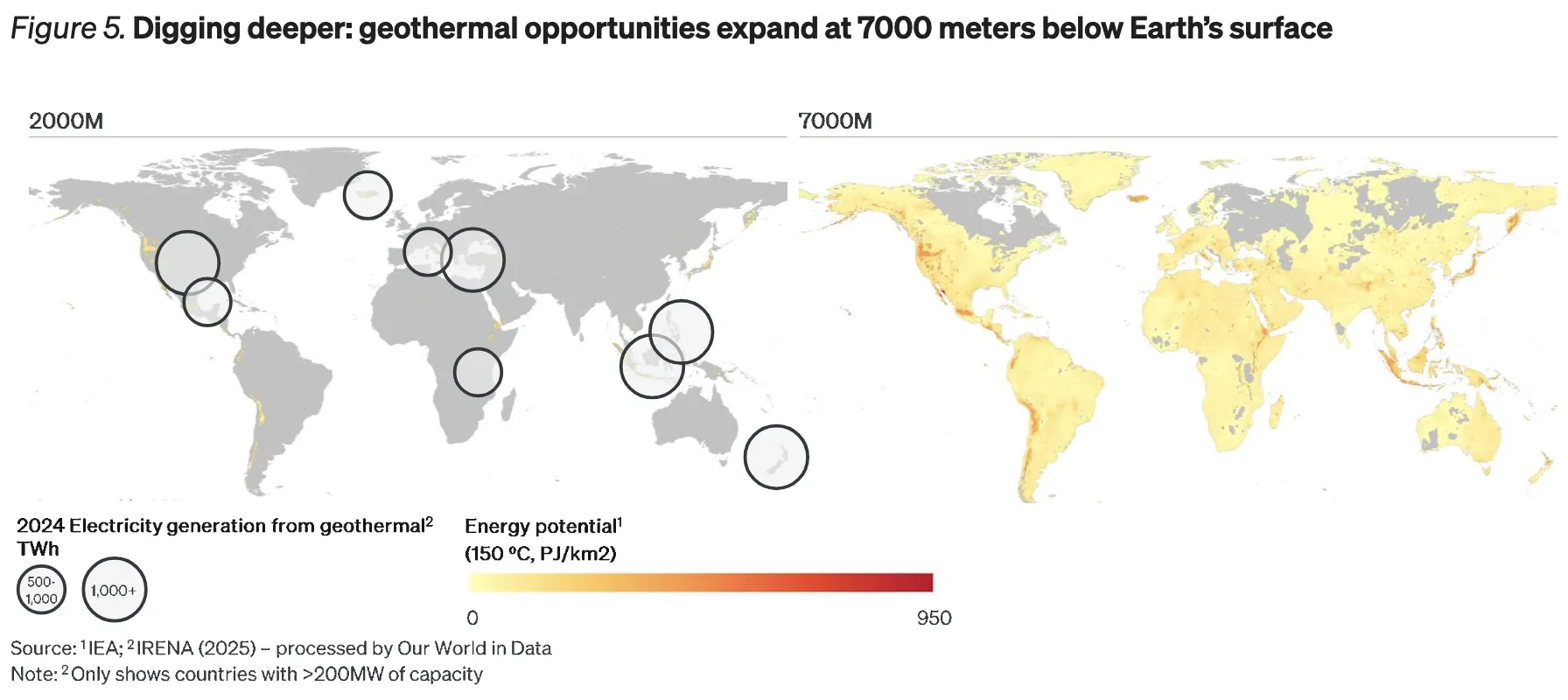

Geothermal is perhaps the most underappreciated energy story of 2025. Until recently, geothermal production was concentrated in a handful of tectonically active regions - the western US, Indonesia, the Philippines, Turkey, Kenya, New Zealand, and Iceland - where geothermal resources sit within 2,000 metres of the surface. But advanced drilling technology is changing the picture entirely. With new horizontal drilling techniques capable of reaching 7,000 metres, geothermal potential now extends across vast new territories. In Utah in 2025, Fervo Energy drilled a well to 15,765 feet in a little over two weeks, accessing temperatures of 520°F. The US and Mexico - with their deep oil-and-gas drilling expertise - hold a structural advantage in commercialising this technology both domestically and as an export.

Nation Energy Profiles - Who Holds the Best Hand?

Energy advantage is not simply about what resources you sit on. It is about what you can process, what you can export, what infrastructure you control, and how your alliances shape access. Here are the five key players whose energy strategies will define the next decade.

- 13.3M bpd oil (world #1)

- World-leading LNG exports

- Best solar irradiation in SW

- Geothermal technology leader

- Deep shale drilling expertise

- IRA subsidies catalysing clean energy

- 520 GW installed wind (world #1)

- 83–97% of global solar mfg

- Controls critical mineral processing

- Belt & Road energy diplomacy

- Nuclear capacity surpassing US by 2030

- Graphite & gallium export controls

- 49% of global lithium production

- Top cobalt, nickel & REE supplier

- Top LNG exporter

- Excellent solar & wind geography

- AUKUS security alignment

- Building processing capability

- North Sea offshore wind (Dogger Bank)

- French nuclear fleet (60%+ electricity)

- EU Green Deal investment framework

- Cut Russian gas imports by >50%

- LNG import terminals fast-tracked

- Overdependence on Chinese clean inputs

- World's lowest-cost oil producer

- Maximum solar irradiation geography

- $8.3bn 2025 solar & wind deals (15 GW)

- Aims 50% renewable power by 2030

- Pursuing civilian nuclear program

- Aramco pivoting to hydrogen & solar

The key takeaway from this comparison is that the nations holding the strongest energy hands are those with multiple overlapping advantages - not just one. The United States holds the broadest advantage across fossil fuels, solar geography, geothermal technology, and LNG export infrastructure. Australia has the raw materials but is still building its processing capability. China has manufacturing dominance but remains import-dependent for oil and has geographic solar limitations. The energy security race will be won by those who can string together multiple advantages into a resilient, diversified system.

China's Clean-Tech Stranglehold

The most consequential fact in the global energy transition is not how fast solar and wind are growing - it is that the manufacturing capacity to build them is almost entirely controlled by one country. China's dominance across the clean energy supply chain is not an accident. It is the result of two decades of deliberate industrial policy, state financing, and strategic patience.

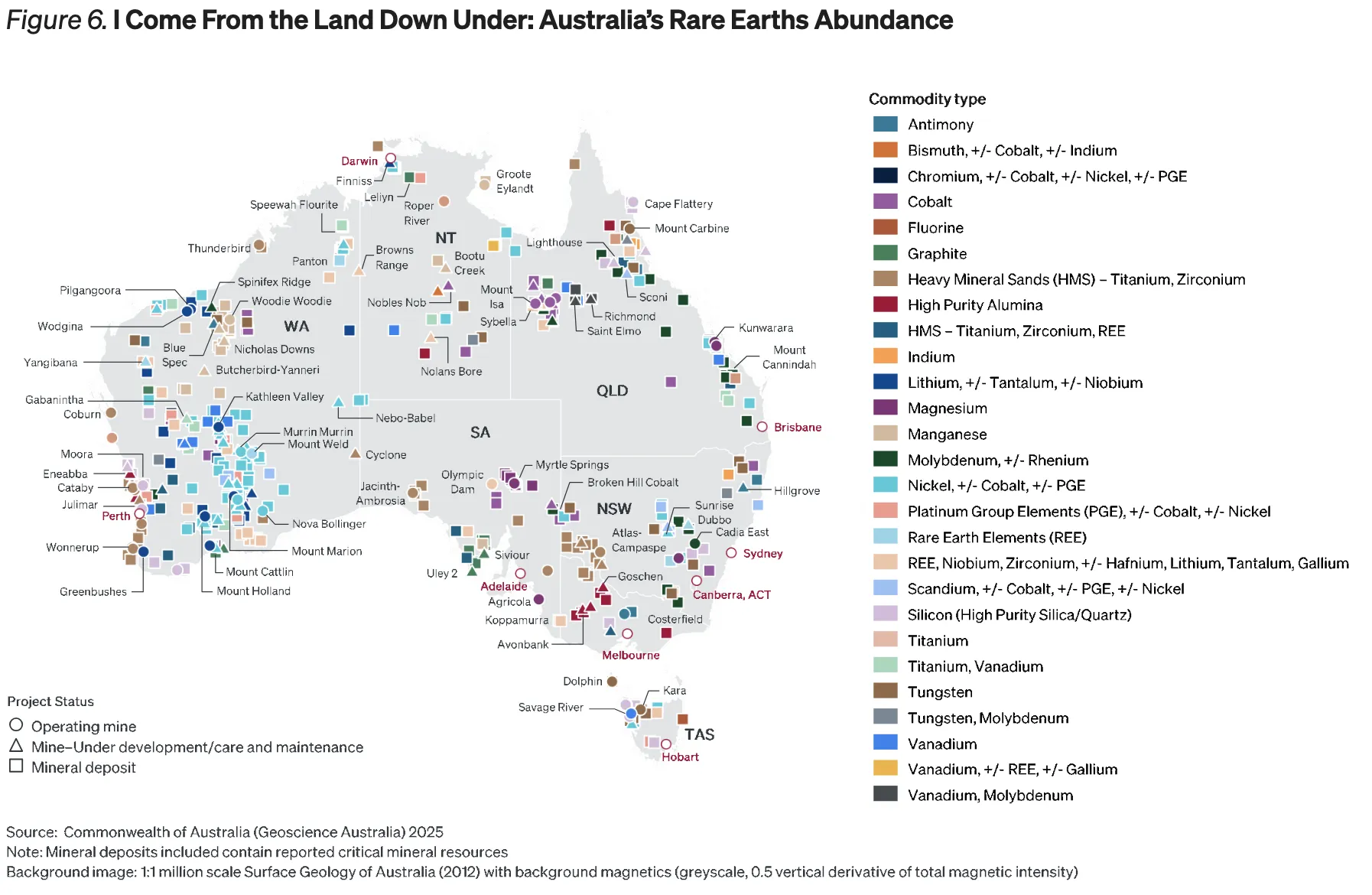

Australia holds some of the world's largest and most diverse reserves of critical minerals - 49% of global lithium production, plus top positions in cobalt, nickel, and rare earth elements. The catch: Australia exports its mined raw materials, then watches China process them into finished battery components and magnets. The economic and strategic value of those minerals is captured downstream - not at the mine.

The chart above makes the scale of China's clean-tech dominance viscerally clear. Across solar modules (83%), solar cells (89%), solar wafers and ignot (97%), battery cells (86%), battery anodes (96%), and battery cathodes (87%), China's share of global manufacturing capacity is not just leading - it is structurally controlling. Any country trying to build a clean energy future that doesn't have a plan for this dependency is building on sand.

China weaponises this position through multiple levers. Beijing's export restrictions on graphite and gallium - critical to batteries and semiconductors - demonstrate how midstream processing capabilities can be repurposed as tools of coercion. The Belt and Road Initiative provides energy financing to Africa, Southeast Asia, and Latin America that is typically tied to Chinese equipment and labour, cementing China's market share and technological partnership across the developing world. This is not just a commercial exercise - it is a deliberate strategy to reduce China's own dependence on imported crude and natural gas while extending its influence over global energy standard-setting.

China's Clean-Tech Supply Share

OPEC+ and the Oil Market Gambit

While the world debates the energy transition, the oil market is undergoing its own structural shift. OPEC+'s September 2025 decision to increase output by 547,000 barrels per day marked a strategic pivot - from price defence to market share competition - with consequences that ripple far beyond the commodity itself.

By accelerating the unwinding of pandemic-era production cuts, OPEC+ is deliberately targeting U.S. shale producers, who now dominate global output at 13.3 million barrels per day. The move aligns with President Trump's pro-lower-prices agenda, creating an unusual alignment between Washington and Riyadh. But the alignment is fragile: if Brent crude falls below $60 per barrel, Gulf state fiscal breakeven costs start to bite, and the political calculus changes quickly.

| Metric | Current Level | Key Dynamic | Investment Implication |

|---|---|---|---|

| Brent Crude | ~$70/bbl | OPEC+ hike suppressing price | Hedged energy stocks (CVX, XOM) offer yield with downside protection |

| US Shale Output | 13.3M bpd | World's largest single producer | Flexible swing capacity; watch $55 breakeven threshold |

| OPEC+ Hike | 547K bpd increase | Market share over price defence | Near-term headwind for E&P stocks; long-run supply discipline still holds |

| Potential Surplus | 1.5M bpd (IEA) | If demand falters, oversupply hits | Services companies (SLB) outperform pure-play E&P in volatile oil markets |

| Physical Market | Tight near-term | Inventory drawdown supports prices | Backwardation structure favours spot holders over futures rollover |

OPEC+'s actions also ripple into the energy transition in a paradoxical way. While increased oil output delays the urgency of decarbonisation, the capital generated by oil revenues is increasingly being diverted toward renewables. Saudi Aramco's investments in hydrogen infrastructure and solar projects in the Middle East are accelerating. Russia has deepened its energy ties with China and India following Western sanctions. The oil market is not simply declining - it is evolving into a more complex, multipolar structure.

For investors, the key insight is that oil market volatility demands a layered exposure strategy. Pure-play exploration and production companies face direct commodity risk. Oil services companies like Schlumberger (SLB) - which earn fees regardless of which direction oil moves, as long as drilling activity continues - offer better risk-adjusted exposure. Integrated majors like Chevron (CVX) and ExxonMobil (XOM) provide commodity exposure with diversified cash generation and strong dividend cover.

The U.S.-China Clean Energy Trade War

The 135% tariff the United States imposed on Chinese goods has created what J.P. Morgan analysts call a "clean energy paradox." It is designed to protect American industry. But it has simultaneously exposed the gaping gap between U.S. clean energy ambition and U.S. clean energy manufacturing reality.

Here is the arithmetic: as of 2025, U.S. solar cell production sits at approximately 13 gigawatts. Demand requires 50 gigawatts. That 37-gigawatt gap must be filled from somewhere. With Chinese imports facing punitive tariffs, American utilities have been forced to rely on lithium-iron-phosphate (LFP) batteries - almost entirely manufactured in China - even as Beijing's export controls on rare earth elements threaten U.S. magnet production for electric vehicles and wind turbines.

Meanwhile, the trade war has redirected Chinese export flows toward Europe. The euro area is projected to absorb a 10% surge in Chinese solar panels, batteries, and wind turbines by 2026. This delivers a short-term boost to European energy affordability - European HICP inflation could fall by as much as 0.15 percentage points as cheaper Chinese clean energy technology floods in. But the long-run risk is an overdependence on a single supplier for critical energy infrastructure, particularly as Beijing tightens its grip on the minerals that underpin those products.

Southeast Asian nations - particularly Vietnam, Indonesia, and Malaysia - are emerging as beneficiaries of the trade war redirection. Chinese manufacturers building facilities in these countries to circumvent U.S. tariffs are creating new local industrial bases. Battery firms in Southeast Asia and European solar manufacturers are positioned to benefit from redirected trade flows over the medium term.

The Inflation Reduction Act remains the single most important policy lever for U.S. clean energy manufacturing. Its grants, loan guarantees, and tax credits are designed to compress the timeline for domestic capacity buildout. But LNG offtake agreements have now become part of tariff negotiations - the EU has pledged to purchase $750 billion in U.S. energy exports (including nuclear technology and fuel, LNG, and crude oil) through 2028. Energy is trade policy. Trade policy is energy strategy.

Hot Zones - Where Energy Meets Conflict

The new energy security age is not just being shaped in boardrooms and legislative chambers. It is being shaped on battlefields, in shipping lanes, and at chokepoints that carry the blood of the global economy. Three hot zones demand investor attention today.

The broader investment lesson from these hot zones is that energy infrastructure is now a military-grade asset. Physical disruption risk - once considered a tail event - must be priced into any long-duration energy investment. Companies with geographically diversified production, flexible supply chains, and low-cost operations will weather disruption better than those with concentrated exposure to any single corridor or region.

The Innovation Frontier: LNG, Nuclear, Storage & AI

Even as geopolitical rivalry reshapes energy markets, four technological threads are quietly redefining what is possible - and where the long-run investment returns will be found. Understanding them is essential for any energy investor with a 5-to-10-year horizon.

| Technology | Current State | 2030 Outlook | Key Players |

|---|---|---|---|

| LNG | 2% supply growth in 2024; strong Asia & Europe demand | 6% supply rebound in 2025; "bridge or destination" debate intensifying | US LNG exporters; Cheniere (LNG), Shell, TotalEnergies |

| Nuclear / SMRs | <10% of global electricity; SMRs moving from design to pilot | China to surpass US+Europe nuclear capacity by 2030; SMR commissioning begins | Cameco, NuScale, Rolls-Royce SMR; uranium miners |

| Grid Storage | Global capacity growing; China leads at 43% share | >2 TWh by 2030; 21% annual installation growth; US at 14% share | CATL, LG Energy Solution, battery storage ETFs |

| AI & Data Centres | Data centres driving power demand surge now | AI data centres could drive 10% of global power demand growth by 2030 | Utilities (NextEra, Constellation), nuclear operators, gas turbine makers |

| Clean Energy Investment | $2.1T invested in 2024 (+11% YoY); solar leads | Investment to accelerate as harder-to-abate sectors join transition | FSLR, Enphase, Orsted; clean energy ETFs (ICLN, QCLN) |

LNG's role in the global energy mix is being actively redefined. Critics argue the world should not be locking in another fossil fuel. Advocates argue LNG is not a bridge but a destination fuel - particularly as carbon capture technology advances and countries seek stable baseload power to supplement intermittent renewables. Demand surged in 2024 and 2025, especially in Asia and Europe, as nations sought alternatives to Russian pipeline gas. New LNG export projects are set to drive a supply rebound to nearly 6% growth in 2025.

Nuclear is quietly staging one of the most important comebacks in energy history. Global investment is rising sharply, especially in China, whose nuclear capacity is set to surpass the United States and Europe combined by 2030. Small modular reactors (SMRs) - with roughly a third of the generating capacity of traditional plants but faster build times, lower capital requirements, and greater site flexibility - are at the forefront of this shift. Unlike conventional plants, SMRs can be turned off and restarted, making them ideal companions for intermittent renewables. They are ideal for phasing out coal-fired generation and can complement LNG in providing stable, dispatchable energy.

On AI: the 11,000 data centres that house generative AI tools are among the most power-hungry buildings ever constructed. These centres are projected to drive 10% of global power demand growth by 2030 - and large hyperscale data centres are set to account for almost 70% of copper demand in the building sector by that same date. The paradox is that AI technology, if deployed well, promises to cut 5–10% of global greenhouse gas emissions by 2030 through efficiency gains. The challenge is ensuring the AI energy footprint is powered by clean electrons - not new gas plants.

Investment Framework: Positioning for the New Energy Age

Energy investing in the new geopolitical era requires a different mental model from the old commodity cycle playbook. You are not just betting on oil prices or solar panel installations. You are making long-duration bets on which nations, technologies, and supply chains will win in a world where energy is national security. Here is how to build a resilient energy portfolio.

| Pillar | Thesis | Instruments | Conviction |

|---|---|---|---|

| 1. Supply Chain Diversification | Long-term gains go to firms that reduce chokepoints in critical mineral and clean energy supply chains. Lithium recycling and rare earth processing are the most underfunded links. | MP Materials (MP) - US rare earth processing; Li-Cycle (LCX) - lithium recycling; Lynas Rare Earths (LYC.AX) | High (10-yr horizon) |

| 2. Hedge Oil Volatility | Oil is not going away. But volatility is rising. Diversified integrated majors with strong dividends and oil services companies with fee-based revenues offer resilience without pure commodity risk. | Chevron (CVX), ExxonMobil (XOM) for yield; Schlumberger (SLB) for services; XLE ETF for sector exposure | Medium-High |

| 3. Target Geopolitical Winners | Redirected trade flows from U.S.-China tensions create winners. European and Southeast Asian clean energy manufacturers benefit from Chinese exports pivoting away from the U.S. | First Solar (FSLR) - US solar mfg; LG Energy Solution (LGES) - Korean battery; Australian lithium miners | High (policy-driven) |

| 4. AI-Driven Power Demand | Data centres and AI training require enormous, reliable baseload power. Utilities with nuclear, gas, or firm renewable contracts supplying hyperscalers have multi-decade earnings visibility. | NextEra Energy (NEE), Constellation Energy (CEG), Vistra (VST); nuclear ETF (NLR) | High (structural) |

The energy portfolio of the new security age is not a binary choice between fossil fuels and renewables. It is a barbell: on one side, cash-generating, dividend-paying traditional energy with strong balance sheets; on the other, structural winners in the energy transition - those building the supply chains, the storage systems, the nuclear capacity, and the grid infrastructure that a world running on clean electrons will require. Between those two ends of the barbell, the volatility of geopolitics will create constant trading opportunities - and constant traps for investors who mistake tactical noise for structural signal.

The single most important filter for every energy investment: does this company win in a world where energy is a tool of national security? If it does, the geopolitical tailwinds are enormous. If it doesn't - if it is purely exposed to commodity price cycles without differentiated assets or strategic positioning - it will find the next decade increasingly difficult.

PolyMarket Investment, Research Team, October 2025