Gold closed 2024 as the best-performing major asset class - up 27% for the year, ahead of the S&P 500 and comfortably above investment-grade bonds. The metal has roughly doubled in value since 2019, driven by central bank accumulation, persistent inflation, and a structural shift away from dollar-denominated reserves by emerging market economies.

You would expect the companies that dig gold out of the ground to have had a banner year. Most didn't. The GDX ETF - the benchmark basket of gold producers - returned just 9.4% in 2024. That 17-point gap between the commodity and the equities is not a rounding error. It tells a story about cost inflation, execution risk, and the increasingly bifurcated nature of a sector that looks homogenous from the outside but isn't.

What makes this more interesting - and more investable - is what happened within the GDX basket. Kinross Gold rose 53%. IAMGOLD more than doubled. Agnico Eagle gained 42%. And yet Newmont fell 10%, Barrick fell 14%, and Gold Fields declined nearly 9%. Every one of these companies owns gold in the ground. The difference was execution, costs, and balance sheet discipline. That is the lens through which this ranking should be read.

The 2024 Paradox: Gold Soared, Miners Stumbled

The divergence between gold prices and gold equity performance in 2024 was not random. It reflected two structural forces that have defined this sector for the better part of a decade. The first is cost inflation: the all-in sustaining cost (AISC) for the average major producer has risen from roughly $1,100/oz in 2021 to $1,350-1,450/oz by mid-2024. Energy, labour, and input materials all contributed. When gold ran from $1,800 to $2,100 in 2023, the margin expansion was real but less dramatic than the headline price movement suggested. The companies that had held costs flat captured disproportionate leverage; those managing cost blowouts gave most of it back.

The second force was operational complexity. The wave of mergers and acquisitions that swept the sector in 2022-2023 - Newmont absorbing Newcrest for $17 billion, Agnico completing its integration of Kirkland Lake - left some management teams running post-merger integration projects simultaneously with mine operations. That is hard. When it goes well, as it did at Agnico, the stock rewards investors decisively. When it doesn't, as at Newmont through much of 2024, the street extracts a painful penalty.

"The GDX returned 9.4% in 2024 while gold gained 27%. But within that basket, the range ran from −14% to +104%. Companies with disciplined costs, clean balance sheets, and consistent operational guidance dramatically outperformed. Those without, underperformed even as the commodity ran. This is, unambiguously, a stock picker's market."

The performance divergence within the sector makes passive GDX exposure a blunt and arguably suboptimal tool. An investor who simply bought GDX at the start of 2024 captured a fraction of what a targeted allocation to Kinross or Agnico would have delivered. Understanding why requires understanding each company individually - not just by market cap, but by the quality of their assets, the discipline of their management teams, and the jurisdictional risk embedded in their reserve base.

The Structural Backdrop Entering 2025

What makes the gold mining thesis compelling at the start of 2025 is not simply that gold prices are high - it's that several independent, structural demand drivers are converging simultaneously. CPM Group's annual gold survey, released in late January, projects investment demand at 42-44 million ounces in 2025, up roughly 35% from 2024's 31-32 million ounces. That is a significant step-change. The firm's analysis attributes it to continued central bank accumulation, renewed institutional interest as the Federal Reserve's rate cycle turns, and growing retail participation in emerging markets where gold has historically served as the primary savings vehicle.

Central banks alone purchased approximately 8 million ounces of gold in 2024 - predominantly China, India, Turkey, and Gulf state sovereign wealth funds diversifying away from US dollar reserves. This buying has been less price-sensitive than traditional investment flows: central banks are building strategic reserves, not chasing momentum. That creates a relatively stable floor under the spot price even in periods of equity-driven risk-off selling.

Morningstar DBRS - Global Mining Outlook, January 2025

The conservative street consensus for 2025 sits at $2,582/oz as a full-year average - approximately 8% above 2024's realized price. But that number anchors on analyst models built before CPM Group's demand data was fully absorbed. It represents a floor, not a ceiling. At this price alone, sector margins remain in historically strong territory - adequate to fund dividends, buybacks, and reinvestment simultaneously. The upside scenario is considerably more interesting.

If CPM Group's projected 35% surge in investment demand materialises - 42–44 million oz versus 2024's 31–32 million - alongside continued central bank accumulation at ~8 million oz/year, the supply/demand balance points firmly toward the $3,000–3,500/oz range as a realistic 2025 outcome. A weaker US dollar and any escalation in geopolitical tensions extends that range further. The conservative $2,582 consensus already prices in a strong year. The structural evidence suggests the actual result could be meaningfully higher.

On the supply side, the long-running constraint on new mine development has not abated. Global gold production has plateaued near 110 million ounces per year despite elevated prices, because the pipeline of new projects that would have been greenlit five years ago never materialized. Permitting timelines in most jurisdictions now span a decade or more. The Morningstar DBRS outlook also noted M&A activity as a defining theme: Northern Star's acquisition of De Grey Mining for A$5 billion, and BHP's unsuccessful attempt at Anglo American, underscore that major producers are increasingly choosing to buy reserves rather than find them through exploration. That trend compresses supply growth and supports prices.

Two Business Models, Two Risk Profiles

Before examining individual companies, one distinction shapes the entire analysis: the difference between traditional gold miners and royalty and streaming companies. They are not the same investment, and conflating them creates analytical errors.

Traditional miners - Newmont, Barrick, Agnico, Kinross - own and operate mines. Their returns are highly leveraged to gold prices in both directions. When gold rises, fixed cost structures mean that every incremental dollar of commodity price flows almost entirely to operating profit. When gold falls, or when costs rise faster than expected, the leverage works against them. The experience of 2024 illustrates both sides: Agnico's consistent cost discipline amplified its gains; Newmont's integration-driven cost overruns amplified its losses.

Royalty and streaming companies - Franco-Nevada, Wheaton Precious Metals, Royal Gold - operate differently. They provide financing to miners in exchange for the right to purchase a percentage of future production at fixed, deeply discounted prices. Their cash cost per ounce is locked in, often at $300-500/oz, regardless of what happens at the mine. Labor strikes, cost inflation, geopolitical disruptions - none of these affect their unit economics. The tradeoff is that streamers trade at premium valuations, often 35-50x earnings versus 15-20x for miners, and grow more slowly. In a year like 2024 where the equity market rewarded operational execution, streamers like Wheaton (+14%) and Franco-Nevada (+6%) lagged pure miners like Agnico (+42%) despite their structurally superior economics.

The Top 10 Companies: Profiles and Analysis

Newmont Corporation

World's largest gold producer - scale without parallel

Newmont's 2024 performance is a case study in what happens when the world's largest acquisition meets the world's most operationally complex mining company. The $17 billion acquisition of Newcrest Mining in late 2023 was transformational in scope - adding Brucejack in Canada, Cadia in Australia, and Lihir in Papua New Guinea to an already sprawling portfolio. But integration at that scale, across four continents and multiple mine types, is genuinely difficult. AISC guidance was revised upward twice during 2024, production disappointed against targets, and the stock fell 10% in a year gold gained 27%. That 37-point underperformance is the price investors paid for the execution risk embedded in a post-acquisition integration.

The structural case for Newmont has not changed. There are 96 million ounces of reserves in the ground - a number no competitor can approach. The balance sheet carries an investment-grade credit rating. The 3.2% dividend provides real income during the wait. What the 2024 drawdown has done is compress the valuation toward the lower end of Newmont's historical range, which for a company of this quality and reserve life is a different kind of proposition than it was at 2023's peak prices. The question is how quickly the integration costs subside and production ramps toward the 7 million oz/year target management has guided to. This is a turnaround trade within a bull market - the asset base is exceptional, and the timeline for normalization is the only variable that matters.

Barrick Gold Corporation

Tier 1 focus, execution yet to match the strategy

Barrick's 2024 performance was the most frustrating in the sector for a company that looks compelling on paper. CEO Mark Bristow's strategy - concentrate only on Tier 1 assets (10+ year mine lives, low costs, expansion potential), reduce debt aggressively, and return capital - remains analytically sound. The problem was execution. Nevada Gold Mines production guidance was cut mid-year. Loulo-Gounkoto in Mali faced political complications that added jurisdictional uncertainty at a time when investors were already charging a risk premium for African operations. The company missed its Q3 production estimates significantly enough to prompt a credibility discount that the shares still carry heading into 2025.

At roughly $1,100 AISC against a gold price north of $2,700, the margin capacity is substantial - every ounce Barrick produces generates approximately $1,600 of gross profit, a figure that funds dividends, buybacks, and development work simultaneously. The long-term optionality is genuinely compelling: the Reko Diq copper-gold project in Pakistan represents a multi-decade asset of rare scale, though first production remains years away. The honest assessment is that Barrick has the right portfolio and the wrong recent track record, and the market has learned to discount management guidance until the numbers actually hit. Consistency in H1 2025 could be the catalyst for a meaningful re-rating.

Agnico Eagle Mines Limited

The sector's standout performer - no surprises, no excuses

Agnico Eagle was the standout performer among senior producers in 2024, and the reason is straightforward: the company met or beat its production and cost guidance every quarter. Canadian Malartic, LaRonde, and Detour Lake all operated within expected ranges. The 2022 Kirkland Lake merger integrated cleanly and is now generating the synergies management promised. When there are no negative surprises in a sector as operationally complex as gold mining, the market re-rates the stock with a consistency premium that compounds over time.

The jurisdictional positioning is, in the current environment, arguably Agnico's greatest strategic asset. Approximately 80% of its production comes from Canada, Australia, and Finland - all stable, well-governed, mining-friendly jurisdictions. As investors process what political instability in Mali or the Democratic Republic of Congo actually means for a long-duration capital commitment, the relative safety of Agnico's portfolio commands an increasingly valued premium. The company trades at a higher multiple than peers, but that premium reflects a genuine track record of delivery, not marketing. Fosterville in Australia has faced grade concerns for several years; management has systematically drilled and replaced those reserves. That is what disciplined exploration management looks like in practice, and the market has noticed.

Franco-Nevada Corporation

The royalty pioneer - structural immunity at a cost

Franco-Nevada's 6% return in 2024 understates its fundamental quality and requires context. The Cobre Panama copper mine - the company's single largest revenue contributor at roughly 10% of royalty income - was forcibly shut down by the Panamanian government in late 2023 following mass protests over environmental concerns. That closure overhang depressed the stock throughout 2024, even as the underlying portfolio of 400+ royalties across gold, silver, oil and gas, and base metals continued to perform. Remove Cobre Panama from the picture and Franco-Nevada's 2024 result looks considerably more coherent relative to the gold price movement.

The structural case for Franco-Nevada is its immunity from cost inflation. When AISC rises sector-wide - which it has been doing consistently since 2021 - Franco-Nevada's economics are unaffected. The company pays nothing for the ounces it receives under its stream agreements; its cash cost is contractually fixed, often at a fraction of spot. That means every dollar of gold price increase flows almost entirely to the bottom line, with no offsetting cost pressure. Franco-Nevada has raised its dividend for 17 consecutive years, which is not an accident of timing but a reflection of a business model that generates rising cash flows across gold price cycles. At current valuations, the Cobre Panama overhang provides a clear catalyst for re-rating once the political situation in Panama clarifies.

Wheaton Precious Metals Corp

The streaming specialist - leverage without the operational risk

Wheaton's business model is perhaps the purest expression of the streaming concept. The company owns the right to purchase gold and silver from 30+ operating mines at fixed, deeply discounted prices - approximately $450/oz on gold streams. At gold's current levels north of $2,700, each ounce Wheaton receives from its streaming counterparties generates over $2,000 in gross profit without the company having touched a shovel. The Salobo copper-gold mine in Brazil (streamed from Vale) and the Constancia mine in Peru are the anchor assets, and both are long-life, low-cost operations with decades of production ahead.

Wheaton's 14% gain in 2024 lagged the gold price, primarily because the equity market was rotating toward higher-beta miners for operating leverage. In a gold bull market, this is often the pattern: streamers provide steady, compounding returns over long periods but aren't the instrument investors reach for when they want maximum asymmetric upside. What Wheaton offers is a 20+ project development pipeline - stream agreements signed on mines still in construction or early production - that provides a visible growth runway without requiring any capital allocation decisions. For investors who want precious metals exposure without the volatility of operational mining companies, Wheaton and Franco-Nevada represent the sector's most reliable core holdings.

Ranks 6–10: The Next Tier

The second half of the ranking covers a group that, in aggregate, outperformed the senior producers in 2024. Kinross and AngloGold were the clear standouts. Gold Fields and Endeavour carried their own specific stories - one a ramp-up challenge, the other a political risk story. Polyus, Russia's largest producer and the world's lowest-cost miner, effectively does not exist for Western investors due to sanctions.

| Rank | Company | Market Cap | 2024 Return | AISC (est.) | Investment Note |

|---|---|---|---|---|---|

| #6 | Kinross Gold (NYSE: KGC) | ~$12B | +53.2% | ~$1,150/oz | Best senior-producer trade of 2024; Great Bear optionality still not fully priced in |

| #7 | AngloGold Ashanti (NYSE: AU) | ~$13B | +23.5% | ~$1,290/oz | Post-South Africa demerger transformation; growing toward 3M oz/yr; deep value vs. peers |

| #8 | Gold Fields (NYSE: GFI) | ~$10B | −8.7% | ~$1,320/oz | Salares Norte ramp-up disappointment dragged 2024; underlying portfolio solid once operational |

| #9 | Endeavour Mining (TSX: EDV) | ~$6B | N/A | ~$1,050/oz | Best margins in West Africa; Burkina Faso security concerns a permanent risk premium |

| #10 | Polyus (MOEX: PLZL) | ~$9B* | N/A* | ~$720/oz | World's lowest-cost producer; not investable for Western investors due to Russia sanctions |

* Polyus market cap and performance data reflects MOEX trading, which is inaccessible to most Western institutional and retail investors. It is included for completeness, as it represents one of the world's largest gold companies by production and reserve base.

Kinross Gold: The Sector's Best-Kept Story

Kinross's 53% return in 2024 came from a combination of clean operational execution and a discovery that most of the market has yet to fully model. Great Bear - a high-grade gold deposit in the Red Lake district of Ontario that Kinross acquired in 2022 for C$1.8 billion - is still being drilled out, but the emerging resource profile suggests a deposit comparable to Agnico's best Canadian assets. The stock currently prices minimal value for Great Bear development optionality, while the existing portfolio (Tasiast in Mauritania, Fort Knox in Alaska, Round Mountain in Nevada) generates strong free cash flow at current gold prices. Mauritania remains a jurisdictional risk worth monitoring, but Kinross's track record of managing complex jurisdictions has improved materially since the 2022 Russia exit.

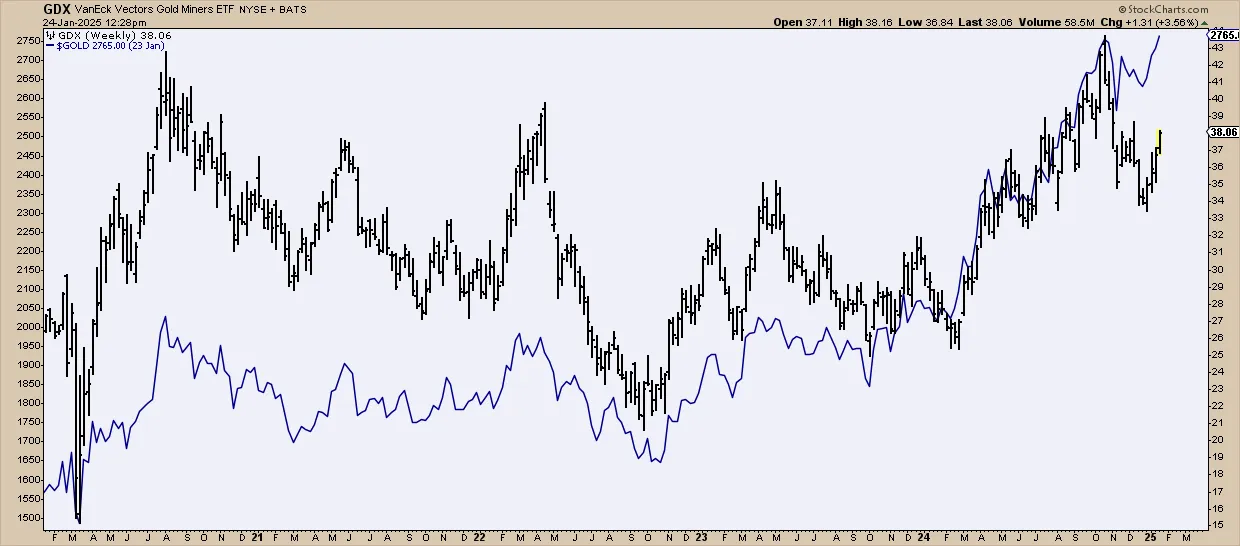

The Technical Picture: Where GDX Sits

Beyond individual company fundamentals, it is worth examining the GDX ETF's technical structure as we enter 2025, because it provides context for positioning and risk management. Through most of 2024, GDX traded in a range bounded by support at $30-33 and resistance near $38. The Bullish Percent Index for gold miners - a breadth indicator that measures what percentage of stocks in the group are on point and figure buy signals - stood at 41% heading into January 2025. That reading is not a crowded trade; it suggests that participation in the sector's recovery has been selective rather than broad-based, and that meaningful upside is available without fighting against a euphoric positioning backdrop.

The chart tells the story clearly. GDX has made a series of higher lows since the October 2024 bottom near $26, and the ZigZag pattern shows the structure tightening against resistance at $38.5. SCTR at 69.9 - StockCharts' relative technical ranking - reflects improving momentum relative to the broader market. The CMF (Chaikin Money Flow) at 0.149 is positive, indicating net institutional accumulation. RSI at 65 is constructive without being overbought. The pattern that StockCharts analysts have noted is an "inflection point" structure: GDX coiling against resistance in a way that suggests a breakout could trigger meaningful momentum buying from systematic strategies. If gold holds above $2,600 and the Federal Reserve's rate path remains accommodative, the catalyst for that breakout could arrive in Q1 or Q2 2025. The honest assessment is that the setup is among the most constructive GDX has shown since the 2020 breakout - but execution, as always in this sector, will be decided at the individual company level.

What Could Go Wrong

Key Risks for the Sector in 2025

The constructive macro backdrop does not make this a risk-free sector. Four risks deserve specific attention:

Gold price reversion. The bull case points toward $3,000–3,500, but the thesis still rests on elevated prices holding. Even at $2,582/oz - the conservative street floor - margins remain healthy. The stress-test scenario is $2,000/oz, at which many of the companies in this ranking would face significant cash flow compression. Mining stocks amplify commodity price moves in both directions: a sharp gold decline can translate to an outsized equity decline. Position sizing matters.

Jurisdictional deterioration. Mali is Barrick's most acute exposure point - the government's posture toward foreign mining companies has become materially more adversarial in the past two years. Burkina Faso presents similar risks for Endeavour Mining. The DRC, where both Barrick and AngloGold have significant assets at Kibali, has historically required intense political management. These risks cannot be eliminated with diversification; they can only be assessed and priced.

Cost inflation persistence. The sector-wide AISC increase of 2021-2024 may not be finished. Energy transition costs, indigenous community agreements, and labour market tightness in key mining regions could continue to erode margins even at elevated gold prices. Companies with fixed-cost structures - the streamers - are genuinely insulated. Operators are not.

M&A value destruction. History suggests that the current M&A cycle will include at least a few acquisitions that look less compelling in retrospect. Newmont's Newcrest acquisition is already testing that thesis. Investors should reward companies that maintain capital discipline and penalize those that make dilutive acquisitions at the top of the cycle.

The Analytical Conclusion: A Stock Picker's Market

The gold mining sector enters 2025 with a stronger structural backdrop than it has enjoyed at any point in the past decade. Gold prices are high, margins are substantial, central bank demand is persistent and price-insensitive, and the professional consensus anticipates further price appreciation even under conservative assumptions. CPM Group's 42-44 million ounce investment demand projection for 2025 - if realized - would represent the strongest annual buying since the financial crisis era.

But the lesson of 2024 is that macro tailwinds do not automatically translate to equity returns in this sector. The range of individual company outcomes was so wide - from Barrick's −14% to IAMGOLD's +104% - that the choice of which companies to own mattered more than the direction of the commodity. That is the core analytical challenge and the core analytical opportunity. An investor who spent the time to distinguish between Agnico's operational discipline and Newmont's integration complexity, or between Kinross's Great Bear optionality and Barrick's execution credibility gap, would have generated returns that bore no resemblance to the GDX benchmark.

Stock Picker's Framework for 2025

The companies most likely to outperform are those that combine three attributes: consistent operational guidance (meet what you say, every quarter), jurisdictional quality (Canada, Australia, Nevada command a premium that is justified and growing), and a catalyst that the market hasn't fully discounted (Great Bear at Kinross; Cobre Panama resolution at Franco-Nevada; margin normalization at Newmont once integration costs subside).

The companies most likely to underperform are those managing complex integration projects while simultaneously navigating operational challenges - particularly if any of those challenges are in politically uncertain jurisdictions. The sector's valuation discount to the S&P 500 provides a margin of safety, but it does not protect against company-specific execution failures in a high-cost environment.

Gold itself, at $2,850/oz and backed by structural demand from central banks that haven't shown price sensitivity, is probably not the risk in 2025. The risk is the company you choose to own it through.

"When the spread between the sector's best and worst performer runs from −14% to +104%, the ETF is a blunt instrument. The opportunity is in understanding which individual companies are genuinely positioned to capture the commodity's upside - and which ones are just along for the ride."

- PolyMarkets Investment, Research Team

Investment Disclaimer

This article is for educational and informational purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Gold mining stocks are volatile investments; prices can fluctuate 20-50% or more in short periods. Geopolitical risks, operational setbacks, and commodity price declines can cause significant losses. All performance data cited is sourced from publicly available market data as of January 2025. Past performance does not guarantee future results. Conduct your own research and consult a qualified financial adviser before making investment decisions.

PolyMarkets Investment, Research Team, January 30, 2025