Most people get this completely backwards. They want to know which stock to buy before they've figured out what account to put it in - or whether they should even be investing at all yet. I've watched friends dump money into a brokerage account while carrying $8,000 in credit card debt at 24% APR. That's not investing. That's lighting money on fire with extra steps.

So this guide starts from the actual beginning. What investing is. What you need sorted before a single dollar goes in. And the precise order in which to deploy capital once you're ready - a framework called the Investing Order of Operations, developed by financial educator Brian Preston of The Money Guy Show. It's quietly helped hundreds of thousands of people avoid the most expensive early mistakes. We've layered it with the fundamentals of risk tolerance, account types, and tax efficiency so you walk away with a real understanding, not a pile of buzzwords that sound smart at dinner.

The First Decision: Active vs. Passive Investing

Before you pick a single investment, you need to answer one question: how involved do you actually want to be? This is the fork in the road that everything else depends on. And the research on which path works better for most people is, frankly, embarrassing for the active management industry.

Active investing means you're researching individual stocks, bonds, or funds - trying to beat the market through superior analysis. Passive investing means you own the whole market (or a big slice of it) through index funds, accepting the market's return instead of trying to outsmart it. One approach requires skill, time, and conviction. The other requires patience and a willingness to be bored.

Here's the uncomfortable truth: over a 20-year period, more than 90% of actively managed funds underperform their benchmark index after fees. These aren't amateurs - they're professionals with Bloomberg terminals, research teams, Ivy League MBAs, and decades of experience. And they still can't beat a simple S&P 500 index fund with any consistency. The reason is structural. When millions of smart people are all trying to outperform each other using the same information, edges evaporate fast. But the fees? Those stick around forever.

Why Passive Wins

Index funds don't win because passive investors are smarter. They win because passive investors pay dramatically less to play the game. An actively managed fund might charge 1-1.5% per year; a Vanguard or Fidelity index fund charges 0.03-0.10%. That gap sounds small until you compound it over 30 years - then it's hundreds of thousands of dollars that went to fund managers instead of staying in your portfolio. Boring beats brilliant. It's not even close over long time horizons.

| Approach | Goal | Annual Fees | Long-Term Track Record | Best For |

|---|---|---|---|---|

| Active Funds | Beat the market | 0.5%–1.5% | ~10% succeed long-term | Sophisticated investors with conviction |

| Passive / Index | Match the market | 0.03%–0.10% | Outperforms 90%+ of active funds | Most investors - especially beginners |

| Robo-Advisor | Auto-diversify | 0.25%–0.50% | Competitive with index funds | Hands-off beginners who want automation |

| Individual Stocks | Beat the market | Transaction costs only | Highly variable; most underperform | Experienced investors with research time |

Before You Invest: Three Non-Negotiable Prerequisites

I know you want to skip this section. Everyone does. But investing without these three foundations in place is like running a marathon in flip-flops - you can do it, but the outcome is going to be ugly. Check these boxes in order before opening a brokerage account. Skipping them isn't aggressive. It's fragile.

Prerequisite #1 - Kill the High-Interest Debt

If you're carrying credit card debt at 20-29% APR, no investment on earth reliably returns more than that. Paying off a card charging 25% interest is mathematically identical to earning a guaranteed 25% return. Guaranteed. Risk-free. There is no stock, no fund, no crypto that offers that. Every dollar aimed at high-interest debt first is the single highest-returning financial decision available to you. Clear it before you invest anything. No exceptions.

Prerequisite #2 - Build an Emergency Fund (3-6 Months of Expenses)

This is not an investment. It's insurance. Park it in a high-yield savings account where it's liquid and boring and completely accessible. Why? Because without this buffer, the next surprise - a medical bill, a car repair, a layoff - forces you to sell investments at whatever price the market happens to offer that day. Which, because the universe has a dark sense of humor, tends to be the worst possible price. The emergency fund is what makes your actual investment portfolio truly long-term. Without it, you're always one bad month away from panic-selling.

Prerequisite #3 - Figure Out Your Investable Number

Calculate what you can invest each month without dipping into your emergency fund or taking on new debt. This is money you're prepared to not touch for at least five years. And here's the part people don't believe until they see the math: even $50 or $100 a month matters enormously when time is on your side. The amount is way less important than the consistency and the timeline. Starting small and showing up every month beats waiting until you can afford "real" money to invest.

The Investment Universe: Six Asset Classes

Every investable asset falls into one of six buckets. Understanding what each one actually does - and more importantly, what it can't do - is how you build a portfolio that matches your goals instead of just looking impressive on a Reddit screenshot.

Understanding Your Risk Tolerance

Risk tolerance isn't about what you can handle on paper. It's about what you can handle at 2 AM when your phone shows a 30% loss and every instinct in your body is screaming to sell. That gap between theoretical tolerance and actual behavior is where most investors blow themselves up.

So ask yourself one brutally honest question: if my portfolio dropped 30% overnight, what would I actually do? Not what you'd like to think you'd do. What you'd actually do. If the honest answer is "sell everything and hide in cash" - congratulations, you're a conservative investor regardless of what your age or timeline says. And that's fine. Building a portfolio beyond your emotional capacity guarantees the single worst outcome in investing: buying during excitement and selling during fear. An investor who sticks with a moderate allocation for 30 years crushes the one who builds an aggressive allocation and panics out of it every downturn.

| Risk Profile | Stocks | Bonds | Alt/Cash | Suitable For |

|---|---|---|---|---|

| Conservative | 30–40% | 50–60% | 10–20% | Near retirement, low volatility tolerance, short horizon |

| Moderate | 50–60% | 30–40% | 5–10% | Mid-career investors, 10–20 year horizon |

| Aggressive | 80–90% | 5–15% | 5% | Young investors with 20+ year horizon |

| Very Aggressive | 95–100% | 0–5% | 0% | Under 30, high income stability, very long horizon |

A quick starting heuristic if you have no idea where to begin: subtract your age from 110. That's roughly your stock percentage. At 25, that gives you 85% equities. At 60, it drops to 50%. It is not gospel - your personal temperament absolutely overrides any formula. But it's a reasonable, battle-tested default that's served millions of people well enough. You can always adjust once you see how you actually react to your first real downturn.

Account Types and Their Tax Advantages

This is the section most beginners skip, and it costs them a fortune. Where you hold your investments matters just as much as what you hold. The exact same S&P 500 index fund in a Roth IRA versus a taxable brokerage will produce dramatically different after-tax wealth over 30 years. Account selection is genuinely free money. Don't leave it on the table.

| Account Type | Tax Treatment | 2025 Annual Limit | Best For |

|---|---|---|---|

| Taxable Brokerage | Pay tax on gains & dividends each year | Unlimited | Post-IOO investing; maximum flexibility, no withdrawal restrictions |

| Roth IRA | After-tax contributions → tax-free growth AND withdrawals | $7,000/yr | Young investors - the single most powerful account available to most people |

| Traditional IRA | Pre-tax contributions → tax-deferred growth → taxed on withdrawal | $7,000/yr | High earners expecting a significantly lower tax rate in retirement |

| 401(k) / 403(b) | Pre-tax contributions → tax-deferred growth → taxed on withdrawal | $23,500/yr | Employer-sponsored plans - especially powerful when employer matching is available |

| HSA | Triple advantage: pre-tax in, tax-free growth, tax-free out for medical | $4,300 single | High-deductible health plan holders - the most tax-efficient account that exists |

The Roth IRA Compounding Advantage

Let me make this concrete because the numbers are wild. A single $7,000 Roth IRA contribution at age 22, left alone at 10% average annual returns, grows to roughly $316,000 by age 62. And you owe zero tax on any of it. Zero. Not reduced tax. Not deferred tax. No tax at all. No other account offers this deal. If your income qualifies, maxing your Roth every single year is one of the highest-leverage financial moves available to a young person. And yet most 22-year-olds don't even know what a Roth IRA is.

The Investing Order of Operations

This is the most important section in this entire guide. Before asking "what should I invest in," ask "where should I put it?" The sequence in which you fill your investment accounts determines how much of your wealth you actually keep versus hand to the government. Follow these steps in order. Do not jump ahead. Do not move to the next rung until the current one is maxed out.

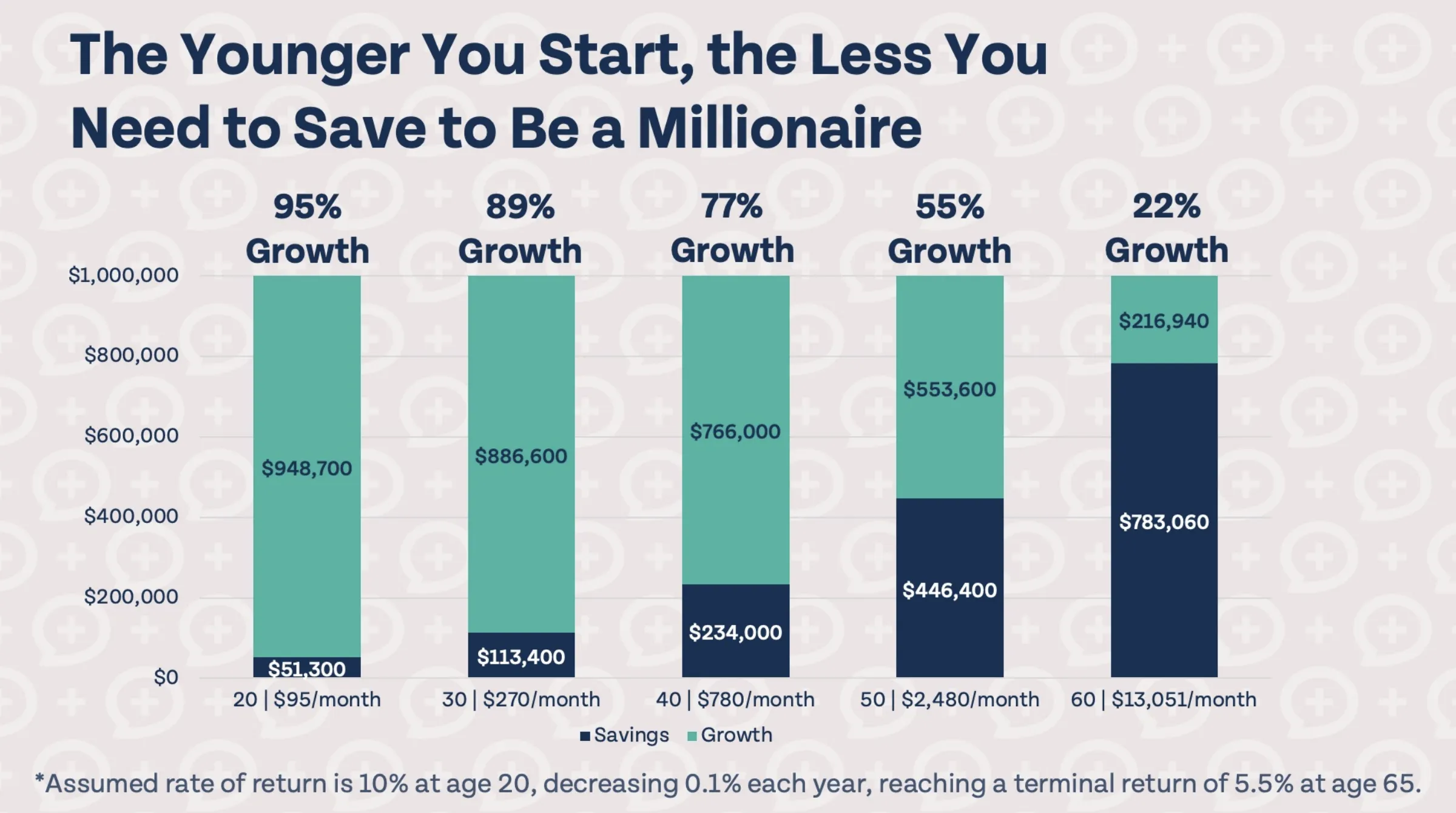

Time Is Your Single Greatest Advantage

Compound growth doesn't work the way people expect. It's not linear - it's exponential, which means the early years look pathetically slow and the later years look like a printing press. The difference between starting at 20 versus 30 is not ten years of returns. It's the difference between needing $95 a month and $270 a month to reach the same destination. Same endpoint, nearly triple the cost - just for waiting a decade.

Look at those numbers and let them really land. Starting at 20, just $95 a month grows to $1,000,000 by age 65. Of that million, $948,700 is compounded growth on only $51,300 of your actual contributions. That's 95% market gains, 5% your money. The compound engine did almost everything. You just showed up consistently.

Now look at the other end. Start at 60 and you need $13,051 every single month to reach the same million. That's 137 times the monthly amount. And $783,060 of that final total comes straight from your pocket because compound interest barely had time to do anything. Five years is not enough runway. Forty-five years is a miracle machine. The gap between those two realities is the entire argument for starting young.

The Rule of Starting Now

Even $25 a week - the cost of a mediocre lunch and a coffee - invested consistently from age 22 into a broad index fund grows to over $500,000 by 65 at 8% average returns. You do not need the perfect portfolio. You do not need the perfect entry point. An imperfect investment made today beats a perfect investment planned for next year. Every single time. The math doesn't care about your excuses.

The Power of Dollar Cost Averaging

Dollar Cost Averaging is the fancy name for something dead simple: invest a fixed amount on a regular schedule, every month, no matter what the market is doing. Up 5%? You invest. Down 15%? You invest. Sideways for six months? Still investing. It eliminates the impossible task of timing the market and - this is the clever part - actually turns volatility into an advantage rather than a threat.

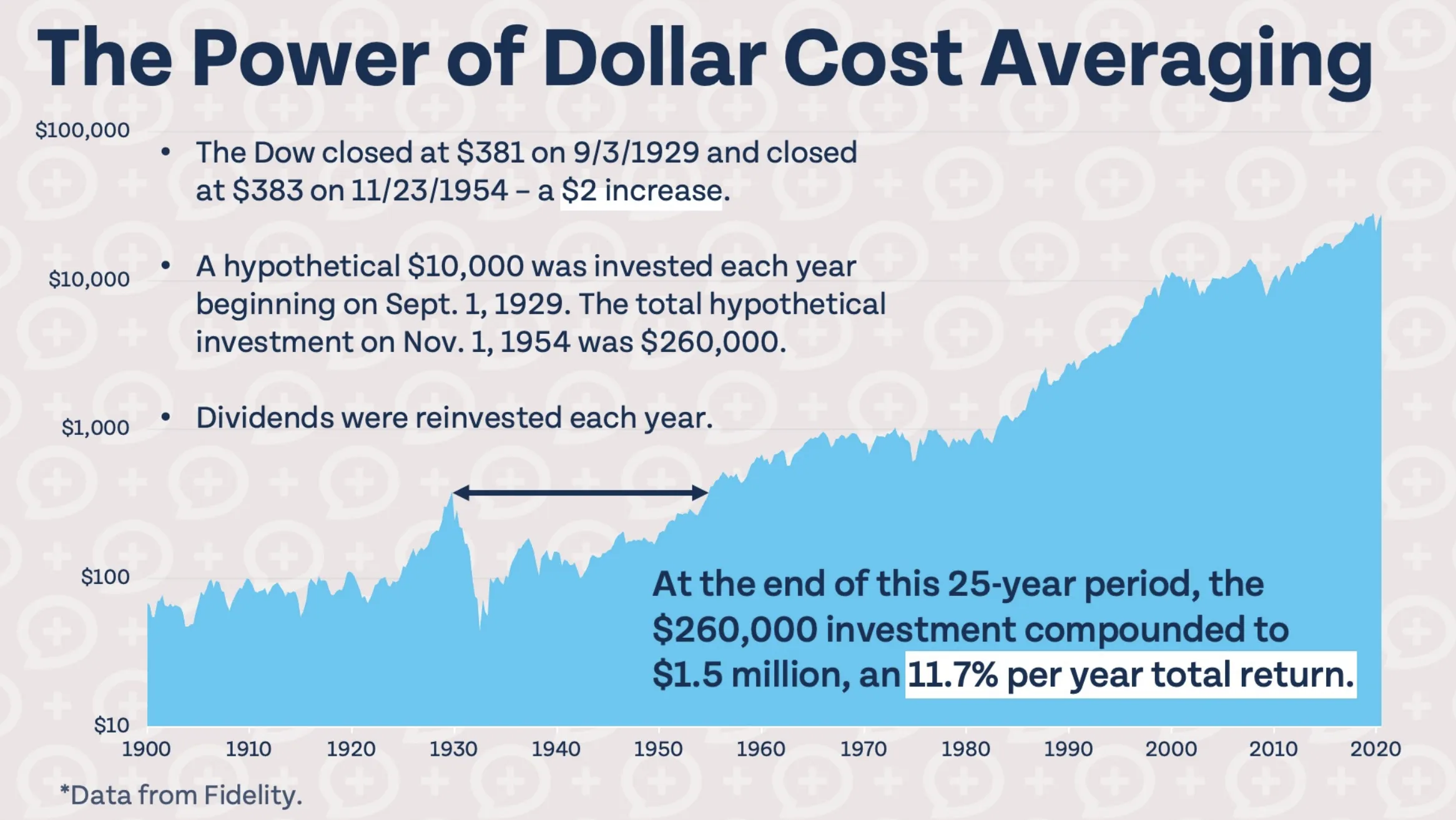

Here's a stat that should permanently end the "I'm waiting for a better time" excuse. Someone who started investing $10,000 per year in September 1929 - literally one week before the worst crash in modern financial history, the absolute peak before the Great Depression - still compounded to $1.5 million by 1954. They started at the single worst possible moment and still built serious wealth. How? By continuing to invest through the crash, they automatically bought more shares at lower prices, which crushed their average cost basis across the entire portfolio. The crash wasn't the enemy. Quitting would have been.

| Month | Amount Invested | Share Price | Shares Purchased | Running Avg Cost |

|---|---|---|---|---|

| January | $500 | $50.00 | 10.0 | $50.00 |

| February | $500 | $40.00 | 12.5 | $45.45 |

| March | $500 | $35.00 | 14.3 | $41.44 |

| April | $500 | $45.00 | 11.1 | $42.10 |

| May | $500 | $55.00 | 9.1 | $43.70 |

Average market price over those five months: $45.00. Your average cost per share through DCA: $43.70. You automatically bought more shares when prices were cheap and fewer when they were expensive. No deliberate decision required. No analysis. No gut feeling. The system did the thinking, and the system doesn't panic.

The Lump Sum Timing Trap

Waiting for the "perfect entry point" is a strategy that fails even professional fund managers with teams of PhDs. Research consistently shows that time in the market beats timing the market over any period of ten years or more. If you've got a lump sum sitting around - an inheritance, a bonus, a windfall - consider DCA-ing it in over 6-12 months. Statistically, lump-sum investing actually wins slightly more often. But the psychological comfort of spreading it out keeps people from doing something stupid if the market drops 10% the week after they go all-in. Sometimes the mathematically suboptimal choice is the right one because it's the one you'll actually stick with.

What You Pay Matters: Taxes on Investment Gains

This is the boring section that makes you rich. Tax efficiency is one of the highest-returning decisions available to any investor, and almost every beginner completely ignores it. Understanding how investment gains are taxed - and structuring around that knowledge - lets you keep dramatically more of what your portfolio earns. We're talking hundreds of thousands over a lifetime. For free. Just by knowing the rules.

| Tax Type | What Triggers It | Rate | Key Strategy |

|---|---|---|---|

| Short-Term Capital Gains | Selling an asset held under 1 year for a profit | Ordinary income rate - up to 37% | Hold all positions at least 366 days before selling to convert to long-term treatment |

| Long-Term Capital Gains | Selling an asset held 1+ year for a profit | 0%, 15%, or 20% depending on income | The goal: patient investors who hold pay a fraction of what active traders pay |

| Qualified Dividends | Dividends from stocks held 60+ days before ex-dividend date | 0%, 15%, or 20% | Similar treatment to long-term gains - highly tax-efficient income |

| Ordinary Dividends | Dividends from non-qualifying holdings or short holding periods | Ordinary income rate | Use dividend-paying ETFs in tax-advantaged accounts when possible |

| Wash-Sale Rule | Selling at a loss then repurchasing same security within 30 days | Loss is disallowed | Wait 31+ days before buying back, or switch to a similar (not identical) ETF immediately |

Tax-Loss Harvesting - Perfectly Legal, Surprisingly Powerful

When a position is temporarily down, you can sell it to realize a tax loss - which offsets capital gains and up to $3,000/year of ordinary income - then immediately buy a similar but not identical ETF to maintain your market exposure. You've just converted a paper loss into a real tax deduction while keeping your portfolio fully invested. The IRS is totally fine with this. The only rule: you can't repurchase the same security for 31 days (the wash-sale rule). Swap VOO for IVV, wait 31 days, swap back if you want. It's one of those rare strategies that's both legal and genuinely useful.

How to Monitor Without Micromanaging

Your portfolio's biggest threat isn't the economy, or interest rates, or China, or whatever's on the news today. It's you. Specifically, your reaction to short-term volatility. The most successful long-term individual investors all share one unglamorous trait: they barely look at their portfolios and they almost never trade.

There's research on this and it's damning. Checking your portfolio daily correlates directly with worse long-term returns. A 2% drop - which is completely normal, happens all the time, means absolutely nothing for a long-term investor - triggers the same neurological stress response as a physical threat. The lizard brain screams "sell and survive." The rational part of your brain knows a 2% daily swing is statistical noise. But the lizard brain is faster, louder, and it doesn't care about your 30-year time horizon.

The Notification Problem

Seriously consider removing your brokerage app from your phone's home screen. Turn off all price alerts. One study found that investors who checked daily earned an estimated 2.3% less per year than those who checked monthly. On a $200,000 portfolio, that's $4,600 a year - lost purely because of the behavior triggered by looking too often. You are literally paying thousands of dollars a year for the privilege of stressing yourself out. Move the app to a folder. Better yet, delete it and use the website when you need it.

| Review Cadence | Purpose | Actions to Consider |

|---|---|---|

| Monthly | Confirm contributions processed correctly | Adjust contribution amounts if income has changed |

| Quarterly | Portfolio drift check against target allocation | Rebalance if any allocation has drifted 5%+ from target |

| Annually | Full strategic review | Update risk profile, increase contribution rates, review account types |

| After Major Life Events | Fundamental realignment | Marriage, children, home purchase, job change - revisit risk tolerance and timeline |

Six Investing Myths That Keep People on the Sidelines

These six myths have collectively cost ordinary people decades of wealth-building. Each one sounds reasonable on the surface, which is what makes them so dangerous. Every person I know who waited too long to invest believed at least two of these.

Myth #1 - "I need a lot of money to start investing"

Wrong. Fractional shares let you buy $1 worth of Apple, Amazon, or any S&P 500 ETF. One dollar. Fidelity, Schwab, and Robinhood all offer $0 commissions and fractional share support. You can start with $25 today - right now, on your phone, in about ten minutes. The idea that investing requires thousands of dollars is a holdover from the 1990s. It hasn't been true for years. Waiting until you have "enough" is a waiting room with no exit sign.

Myth #2 - "I'll invest once the market calms down"

The market never calms down. There is always something. A trade war, an election, a banking crisis, a pandemic, rising rates, falling rates, inflation, deflation. Pick your decade - the reasons to wait always look convincing in real time. But volatility is the admission price for higher long-term returns. And while you sit in cash waiting for calm, inflation is quietly eating your purchasing power at 3-4% per year. Your "safe" money is losing value every single day you don't deploy it.

Myth #3 - "Investing is basically gambling"

This one drives me crazy. Gambling is zero-sum - one winner requires one loser, and the house always has an edge against you. Investing in productive businesses creates real economic value. These companies employ people, build products, generate cash flow, and grow over time. The S&P 500 has delivered positive returns in roughly 75% of all calendar years since 1928. Roulette wheels don't employ 150 million people or generate trillions in economic output. The comparison is lazy and it keeps people poor.

Myth #4 - "I need a financial advisor to get started"

You really don't. A two-fund portfolio - total US market ETF plus total international ETF - requires no advisor, beats most professionally managed funds over time, and takes maybe 20 minutes per year to maintain. A fee-only fiduciary advisor absolutely adds value once you have substantial assets, complex tax situations, or estate planning needs. But for someone starting out? The most important step is starting. Not optimizing. Not finding the perfect advisor. Starting.

Myth #5 - "Stock-picking is how the wealthy really build wealth"

Survivorship bias at work. Warren Buffett has explicitly instructed his estate to invest in S&P 500 index funds after he dies. Let that settle. Most billionaire wealth comes from concentrated, long-term positions built over decades in companies they often founded or led - not from scrolling Reddit and buying whatever's trending. The stock-picking mythology survives because we celebrate the rare, spectacular winners and never mention the thousands of people who made the same type of bets and lost everything. For every person who went all-in on Amazon in 2001, a hundred went all-in on Pets.com.

Myth #6 - "Cryptocurrency will replace traditional investing"

For every early Bitcoin millionaire, thousands bought near peaks, panic-sold in crashes, and never recovered. Crypto assets produce no earnings, pay no dividends, and generate no cash flow. Their value is entirely narrative-driven - which means it can move violently in either direction on nothing more than a tweet. As a small speculative allocation under 5% of your portfolio, crypto is a legitimate bet. As a retirement strategy? That is not investing. That is hope with a wallet address.

Seven Mistakes That Cost Beginners Years of Growth

Building wealth through investing is less about making brilliant calls and more about not blowing yourself up. The path to a seven-figure portfolio is littered with people who made one of these seven mistakes, all of which are common, expensive, and entirely preventable.

| The Mistake | Why It Happens | The Fix |

|---|---|---|

| Starting too late | Perpetually waiting for the "right time" or enough money | Start with whatever you have. $50. $25. The compounding clock is ticking whether you're invested or not - the only question is whether it's working for you or against you |

| Day trading | TikTok FOMO, the thrill of quick gains, overconfidence | 70-80% of retail day traders lose money over any 12-month stretch. That's not a maybe - that's the data. Redirect that energy into growing your income and investing passively |

| Using margin | Wanting to amplify small wins into big ones | Margin amplifies losses exactly as much as it amplifies gains. A 50% drop on 2x leverage is a complete wipeout. Beginners using margin is like handing car keys to someone who hasn't learned to brake |

| Panic selling | Fear of further loss becomes physically unbearable | Every bear market in modern history has been followed by a new all-time high. Every single one. Selling during a drawdown converts a temporary paper loss into a permanent, real, irreversible one |

| Skipping the employer match | Not understanding how 401(k) matching works | Contribute at minimum enough to capture 100% of the match - from your very first eligible paycheck. This is free money. About 25% of employees leave it on the table |

| Sitting in cash | Analysis paralysis, fear, waiting for a signal | Cash in a standard savings account loses purchasing power every year to inflation. At minimum, park surplus in a HYSA or short-duration treasury ETF while you figure out next steps |

| Ignoring expense ratios | Assuming all funds cost about the same | A 1% expense ratio vs. 0.03% on $100,000 costs you roughly $970/year in compounded opportunity. Every year. Forever. That's not a rounding error - it's a car payment going to your fund company |

The Simple Winning Formula

Start early. Invest consistently. Use low-cost index funds. Fill tax-advantaged accounts in the order the IOO prescribes. Then get out of your own way. That's the whole thing. The people who built real, lasting wealth over the past 50 years didn't have insider tips or a secret Bloomberg terminal in their basement. They had patience, discipline, and the self-awareness to keep their costs low and their emotions out of the decision-making process. Nothing about this formula is complicated. The hard part is sticking with it when everything around you is screaming to do something else.

Research Desk, PolyMarkets Investment, August 2025