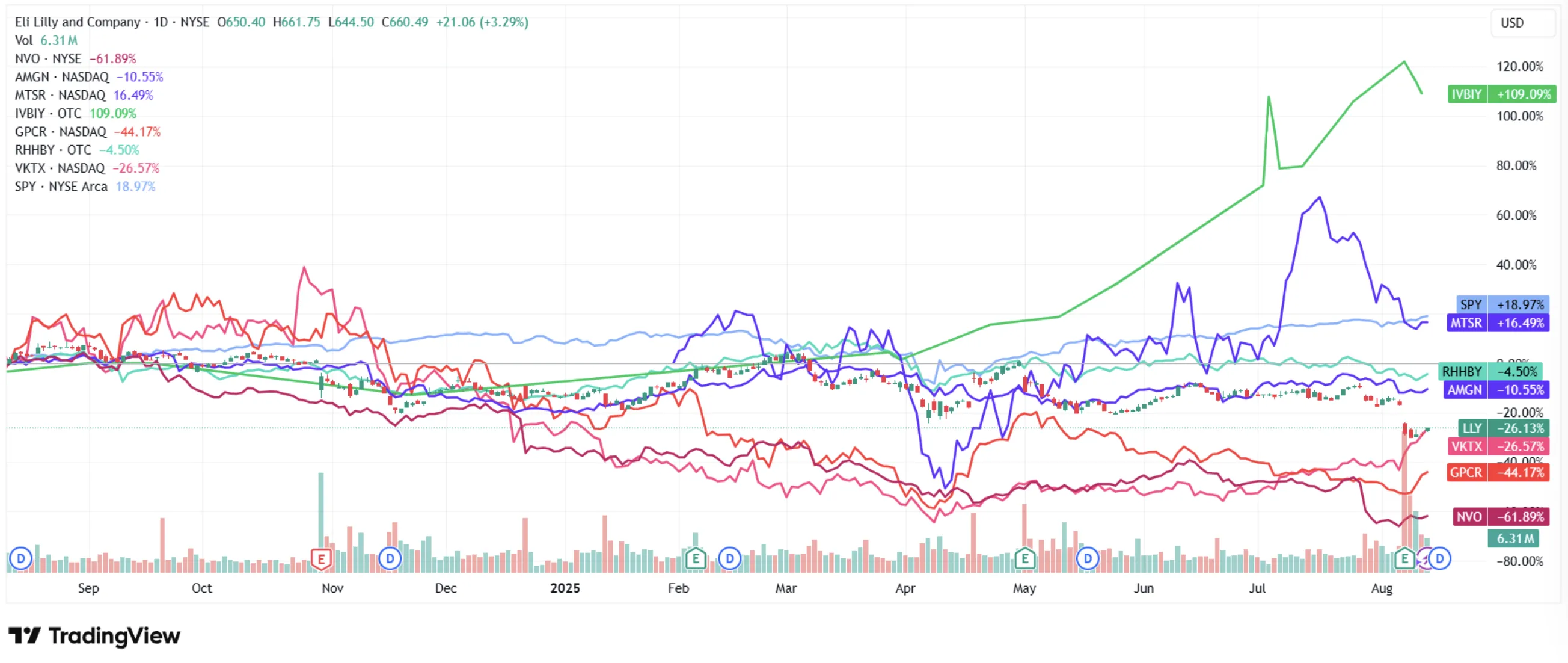

Something remarkable has happened in pharmaceutical markets over the past twelve months. Novo Nordisk - the company that invented the modern GLP-1 era, the maker of Ozempic, the firm whose drugs are now cultural phenomena - has seen its stock lose over 60% from its all-time highs. Meanwhile, Eli Lilly sits 25% off its peak, still commanding nearly three times Novo's earnings multiple. The market has decided, in effect, that one company has already won the GLP-1 war and the other is a fading champion.

We think the market is wrong - or at least, oversimplifying a far more nuanced story. A discounted cash flow analysis suggests Novo needs just 1% annual growth to justify its current valuation. Lilly needs 18%. That gap isn't a rounding error. It's a mispricing that may represent one of the most compelling asymmetric opportunities in large-cap pharma today.

This research note examines both companies through the lens of what actually matters: drug efficacy, manufacturing capacity, pipeline depth, the coming oral revolution, geopolitical headwinds, and - most critically - where the market has priced in too much pessimism and where it hasn't priced in enough risk. The GLP-1 market will exceed $150 billion annually by 2030. The question isn't whether these companies will grow. It's which one the market has gotten more wrong.

Financial figures and pipeline data cited throughout this analysis draw from company annual reports, SEC and 20-F filings, Bloomberg consensus EPS estimates, and ClinicalTrials.gov registrations current as of the article's publication date. Analyst price targets reflect consensus ranges compiled from Wall Street research coverage. Revenue projections attributed to unnamed analysts represent Bloomberg consensus or FactSet median estimates unless otherwise specified.

The Battle That's Reshaping Healthcare

The GLP-1 receptor agonist market has become the fastest-growing pharmaceutical segment in history - and it's still in its infancy. Of the roughly 890 million adults globally living with obesity, barely 1-2% are currently treated with GLP-1 drugs. The addressable market is enormous and largely untapped, which is precisely why two companies - Novo Nordisk of Denmark and Eli Lilly of Indianapolis - are engaged in what may be the most consequential competitive battle in modern pharmaceutical history.

This isn't simply a contest over which injection produces more weight loss. It's a multi-front war spanning manufacturing capacity, clinical trial strategy, oral drug development, pricing power, patent protection, and - increasingly - geopolitics. President Trump's administration has sent letters to 17 major pharmaceutical CEOs demanding price concessions under threat of "Most Favored Nation" pricing, adding an entirely new dimension of regulatory uncertainty to what was already a volatile landscape.

Both stocks have been punished severely. Novo's shares have cratered from their 2024 highs, wiping out over $300 billion in market value. Lilly has fared better but still trades well below its peak. The sell-offs were driven by a combination of efficacy uncertainty from clinical trial results, intensifying competition, compounded drug threats, and political headwinds. But beneath the fear, the fundamentals tell a more nuanced story - one where both companies remain dominant, both have robust pipelines, and at least one appears dramatically undervalued.

Two Giants, Two Strategies

Understanding this battle requires understanding how fundamentally different these two companies are - despite competing in the same market.

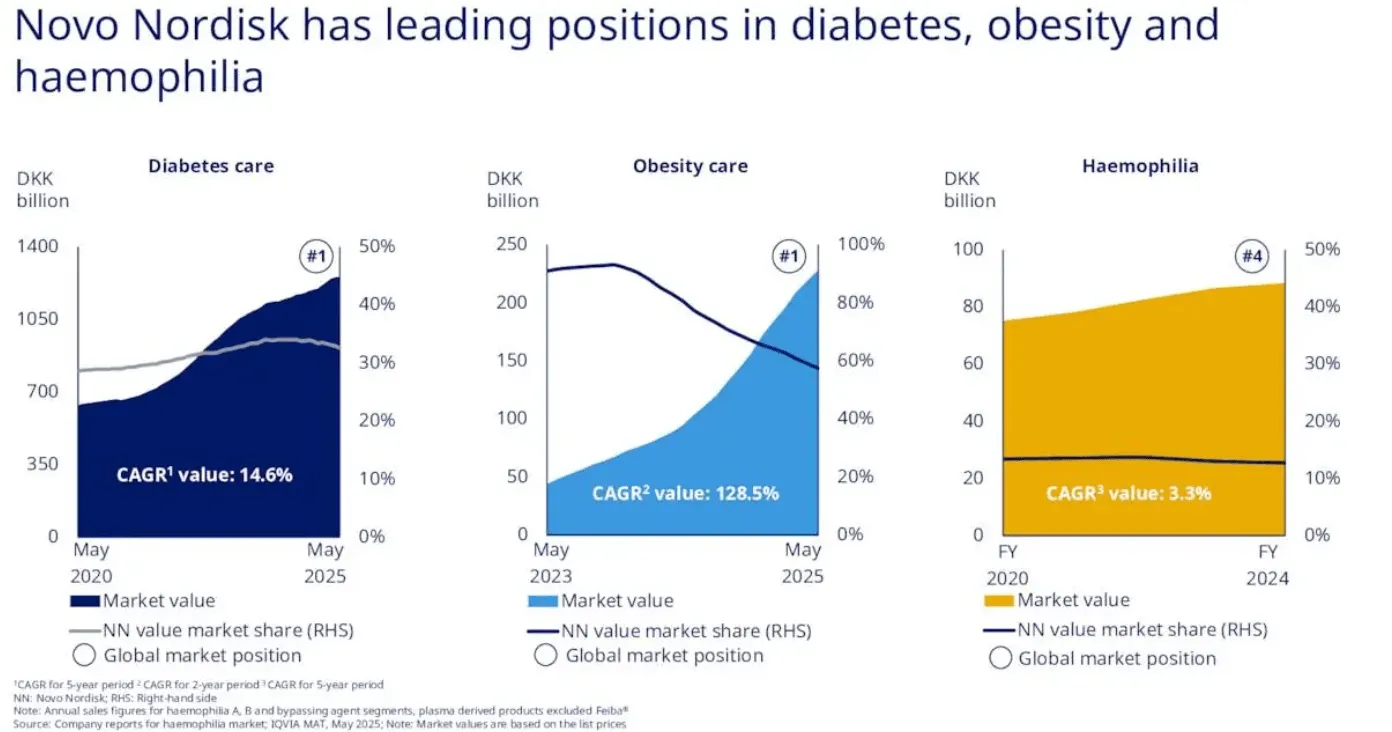

Novo Nordisk is the specialist. Founded in Copenhagen in 1923, the Danish company has spent a century building its identity around metabolic disease. Diabetes and obesity care account for roughly 94% of its revenue, with its GLP-1 franchise alone representing 54% of total sales. This concentration is both its greatest strength and its most significant vulnerability. Novo's flagship drugs - Ozempic for diabetes, Wegovy for obesity, and Rybelsus as an oral diabetes option - are household names. Ozempic has transcended pharmaceutical marketing to become a cultural phenomenon, referenced in everything from celebrity interviews to late-night comedy. That kind of brand equity is worth billions and cannot be easily replicated.

But Novo's narrow focus means it lives or dies by the GLP-1 cycle. When clinical results disappoint - as they did with CagriSema, which achieved 15.7-22.7% weight loss versus the 25% target - the stock gets punished disproportionately. When guidance gets cut - as happened twice in 2025, most recently to just 8-14% sales growth from the original 13-21% - there's no oncology division or Alzheimer's drug to cushion the blow. The company recently replaced its CEO, with veteran Maziar Mike Doustdar taking the helm in August after the surprise departure of Lars Fruergaard Jørgensen. Novo's market cap has shrunk to roughly $241 billion - down from over $600 billion at its peak.

Eli Lilly is the diversified powerhouse. Founded in Indianapolis in 1876, Lilly operates across diabetes, oncology, immunology, and neuroscience. Its GLP-1 franchise - led by Mounjaro for diabetes and Zepbound for obesity - represents about 20% of total revenue, with diabetes care more broadly at 52.5%. The remaining 48% comes from oncology (Verzenio, Jaypirca), immunology (Olumiant), neuroscience (Emgality), and crucially, the Alzheimer's drug Kisunla (donanemab), approved in May 2024 and projected to generate $10 billion or more in peak sales. Lilly sells into 95 countries with production hubs across the US, Europe, and Asia.

This diversification gives Lilly a financial cushion that Novo lacks. When Lilly's oral weight loss candidate orforglipron underwhelmed with 12.4% weight loss at 72 weeks - below the 15% expectations - the stock fell 13%, but the broader business absorbed the shock. Lilly's market cap remains north of $620 billion, and its position as a US-based company gives it a strategic advantage in the current tariff and "onshoring" political environment.

Novo Nordisk at a Glance

Market Cap: ~$241B | Founded: 1923 (Denmark)

Revenue Mix: Diabetes 75% / Obesity 19% / Rare Disease 6%

GLP-1 as % of Revenue: 54% (concentrated)

Key Identity: The metabolic disease specialist - a century of insulin and GLP-1 expertise

Eli Lilly at a Glance

Market Cap: ~$629B | Founded: 1876 (USA)

Revenue Mix: Diabetes 52.5% / Obesity 20.1% / Oncology 15.4% / Immunology 8.3%

GLP-1 as % of Revenue: ~20% (diversified)

Key Identity: The diversified giant - GLP-1s, Alzheimer's, oncology, and neuroscience

The Drug Showdown: Beyond the Headlines

Ask Wall Street which company has the better drug, and the reflexive answer is Lilly. Tirzepatide - the molecule behind Mounjaro and Zepbound - is a dual GLP-1/GIP receptor agonist that produces 20-22% average weight loss, compared to semaglutide's 15-17%. That 3-5 percentage point gap has driven much of Lilly's market share momentum and valuation premium.

But efficacy measured in percentage points of weight loss is only part of the picture. Novo's semaglutide carries something Lilly doesn't yet have: proven cardiovascular outcome data. The landmark SELECT trial demonstrated a 20% reduction in major adverse cardiovascular events - heart attacks, strokes, and cardiovascular death - in obese patients without diabetes. That data didn't just make headlines; it fundamentally changed prescribing behavior and, more importantly, insurance coverage. Over 70% of private insurance plans now cover Wegovy when prescribed for cardiovascular risk reduction, compared to roughly 35-40% for obesity alone. Physicians trust the safety profile that comes with extensive real-world evidence accumulated since Ozempic's launch in 2017.

Lilly's cardiovascular outcomes trial (SURPASS-CVOT) for tirzepatide remains ongoing, with data expected in 2026. If positive - and most analysts expect it will be - it could neutralize Novo's last major clinical advantage. But until that data arrives, Novo retains a meaningful prescribing moat, particularly among cardiologists and primary care physicians who prioritize proven CV reduction over incremental weight loss.

| Metric | Novo (Wegovy/Ozempic) | Lilly (Zepbound/Mounjaro) | Edge |

|---|---|---|---|

| Active Ingredient | Semaglutide (GLP-1 only) | Tirzepatide (GLP-1 + GIP dual) | - |

| Weight Loss (Avg) | 15-17% body weight | 20-22% body weight SUPERIOR | Lilly |

| CV Outcomes Data | SELECT: 20% MACE reduction PROVEN | SURPASS-CVOT pending (2026) | Novo |

| Side Effect Profile | Nausea 20%, discontinuation ~7% | Nausea 12%, discontinuation ~5% | Lilly |

| US List Price | $1,349/mo (self-pay: $499 via GoodRx) | $1,059/mo LOWER | Lilly |

| MASH Indication | FDA approved (Aug 2025) APPROVED | Phase 3 data positive, filing expected | Novo |

| First-Mover Status | Wegovy approved June 2021 | Zepbound approved November 2023 | Novo |

There's a subtlety the table doesn't capture. Novo recently received FDA approval for Wegovy in treating MASH (metabolic dysfunction-associated steatohepatitis) - a serious liver condition affecting roughly 5% of US adults. It's only the second FDA-approved treatment for MASH, alongside Madrigal Pharmaceuticals' Rezdiffra. Lilly has published strong mid-stage data for tirzepatide in MASH as well, but Novo got there first. This matters because MASH represents an under-penetrated market estimated at $16 billion by 2033, and early approval means early prescribing habits form around Novo's drug.

Meanwhile, Novo's aggressive pricing move - launching a $499/month self-pay option for Ozempic through GoodRx - signals a willingness to compete on accessibility, not just clinical data. It's a strategy that simultaneously expands the patient pool, counters criticism over high drug costs, and positions Novo favorably with an administration that has made drug pricing a signature issue. Lilly has responded with similar self-pay discounts on Zepbound, keeping both companies' effective pricing in a tighter band than the list prices suggest.

The Science Behind the Efficacy Gap

The fundamental difference is molecular design. Semaglutide (Novo) activates the GLP-1 receptor alone - reducing appetite, slowing gastric emptying, and improving glycemic control. Tirzepatide (Lilly) is a dual agonist that activates both GLP-1 and GIP receptors simultaneously. The GIP pathway enhances insulin secretion and may independently improve fat metabolism, which explains the additional 3-5 percentage points of weight loss.

However, one percent more efficacy in a clinical trial may not influence the average patient's decision. What matters more in practice are side effects, dosing convenience, insurance coverage, and price - areas where the competition is far closer than the efficacy headline suggests.

Financial Performance: The Valuation Disconnect

Here is where the story gets genuinely interesting for investors - and where the market's narrative diverges most sharply from the numbers.

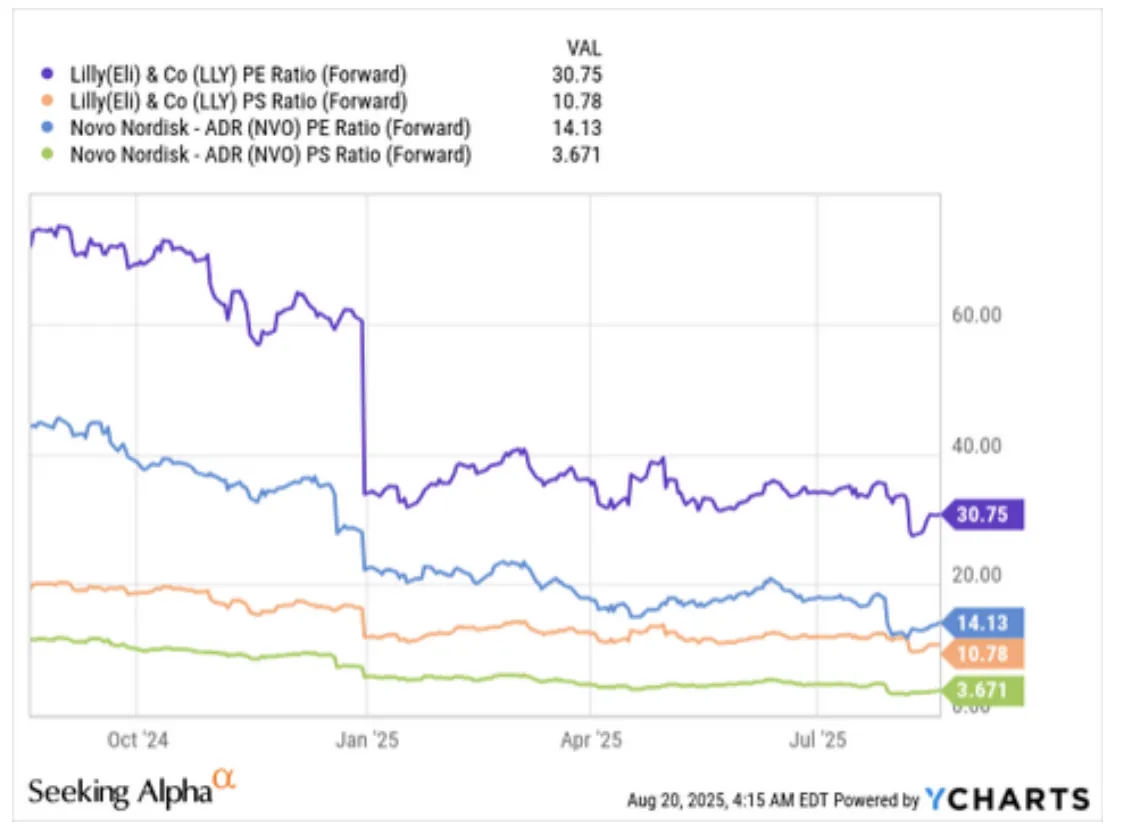

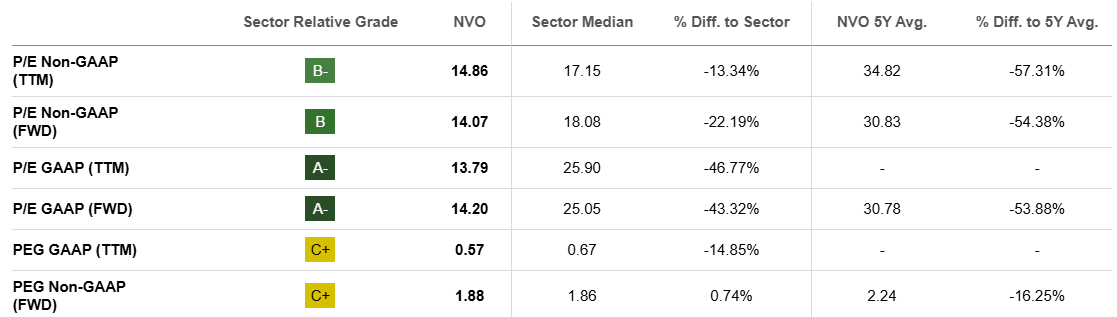

On the surface, Eli Lilly appears to be the clear winner. Its GLP-1 revenue is growing at 168% year-over-year versus Novo's 89%. Its consensus estimates are being revised upward while Novo's have been slashed. Analysts project Lilly's 3-year adjusted EPS growth at a CAGR of 42.4%, compared to Novo's 9.1%. The market has rewarded this with a forward P/E of roughly 31x for Lilly - more than double Novo's compressed 14x.

But valuation is not a growth contest. It's a question of what's already priced in. And when you run the numbers through a discounted cash flow model, the picture flips dramatically.

| Metric | Novo Nordisk | Eli Lilly | S&P 500 Avg |

|---|---|---|---|

| Market Cap | ~$241B | ~$629B | - |

| Fwd P/E (Non-GAAP) | 14.1x 57% BELOW 5Y AVG | 30.8x | ~22x |

| PEG Ratio (FWD) | 1.88 | 0.87 GROWTH BARGAIN | 2.0 |

| EV/EBITDA | 9.8x | 24.4x | ~15x |

| Price/Sales | 4.5x | 10.8x | ~3x |

| Operating Margin | 44-48% INDUSTRY BEST | 28-40% (improving) | - |

| Dividend Yield | 2.35% (rising) | 0.9% | 1.5% |

| Debt-to-Equity | 0.05 (fortress) | 0.82 (moderate leverage) | - |

The DCF Reality Check

A discounted cash flow analysis reveals the most striking finding in this entire comparison. Using conservative assumptions - Novo's 2025 guidance of $49 billion in revenue, a 44% EBIT margin (its four-year average), a 76% EBIT-to-FCF conversion rate, and a 9% WACC with 3.5% perpetuity growth - Novo Nordisk needs to grow revenue at just 1% per year from 2026 to 2032 to justify its current market capitalization. One percent. For a company operating in the fastest-growing pharmaceutical segment in history, with drugs launched in 80+ countries and a $16 billion MASH market just opening up.

Eli Lilly, by contrast, must deliver 18% annual revenue growth through 2032 to support its current $629 billion market cap. That's not impossible - Lilly's 2025 guidance of $61 billion in revenue suggests momentum is strong - but it requires near-flawless execution across manufacturing buildouts, clinical trials, and market share expansion for the better part of a decade. Even a weighted-average growth estimate of 15.8% across all of Lilly's segments produces a DCF-implied valuation roughly 11% below the current stock price.

What the Market Is Pricing In

Novo at $56/share: The market is pricing in near-zero growth and significant competitive erosion. At a forward P/E of 14x - versus its own 5-year average of 31x - investors are treating Novo as though it has already lost the GLP-1 war. Even conservative growth assumptions of 10-11% annually (weighting its diabetes, obesity, and rare disease segments) produce a fair value market cap of $427 billion - implying up to 77% upside from current levels.

Lilly at ~$700/share: The market is pricing in continued dominance, flawless execution, and 18%+ growth for seven years. Lilly's PEG ratio of 0.87x (well below its 5-year average of 2.09x) makes it look attractive on a growth-adjusted basis - but this assumes consensus growth rates hold. Any meaningful stumble - a clinical trial miss, manufacturing delay, or pricing pressure - and the premium compresses quickly.

Revenue Segments: Concentration vs. Diversification

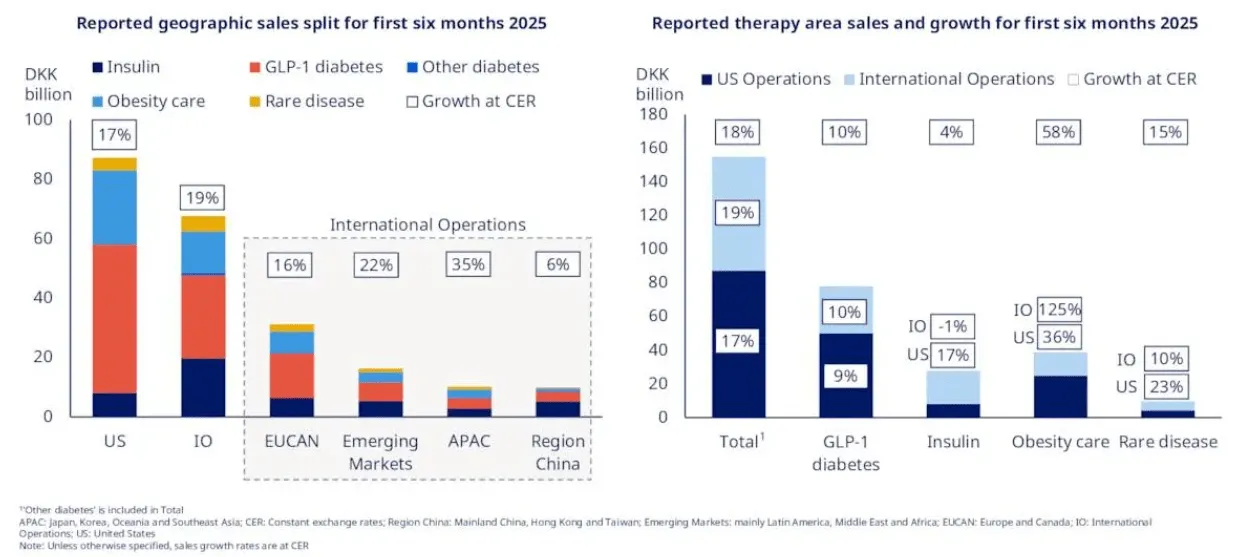

The revenue composition tells you everything about each company's risk profile. Novo generates 75% of revenue from diabetes care and 19% from obesity - meaning 94% of the business rides on the GLP-1 and insulin franchise. Lilly's diabetes care (52.5%) and obesity (20.1%) combine for 72.6%, with the remaining 27.4% spread across oncology, immunology, and neuroscience. That structural diversification is worth something - it provides Lilly with a margin of safety that Novo simply doesn't have.

On profitability, however, Novo is the clear winner. Its 44-48% operating margin is industry-leading, driven by decades of manufacturing expertise and a lean cost structure focused on a single therapeutic area. Novo's gross margin runs above 83%, and the company expects operating profit growth to outpace revenue growth by one to two percentage points annually as R&D and SG&A costs moderate relative to scale. Lilly's margin, while improving rapidly from 28% toward 40%, still reflects the higher cost base of a diversified portfolio and aggressive R&D spending (22% of revenue vs. Novo's 13%).

Pipeline: The Oral Revolution and Beyond

The next chapter of the GLP-1 war won't be fought with weekly injections. It will be fought with pills. And this is where the competitive dynamics could shift in ways the market hasn't fully appreciated.

The Oral Gambit: Why Pills Change Everything

Research consistently shows that the vast majority of patients prefer oral medication over injections. Surveys indicate that 62% of patients favor oral delivery, a ratio that jumps to nearly 78% in English-speaking cultures. Goldman Sachs Research estimates that oral GLP-1 pills will capture roughly 25% of the total anti-obesity medication market by the end of the decade - implying an oral-specific TAM of approximately $23.75 billion by 2030.

This is Novo's potential equalizer. The company's oral semaglutide for obesity - already approved for diabetes as Rybelsus and launched in more than 40 countries - is expected to receive US FDA approval for the obesity indication in late 2025 or early 2026. Novo has been explicit about wanting to "launch the product as close to approval as possible," and the organization is being readied for a rapid commercial rollout. Early data shows 13.1% weight loss at 12 weeks - a strong trajectory that could reach 15%+ at longer durations.

Lilly's oral candidate, orforglipron, stumbled. The highest dose achieved 12.4% weight loss at 72 weeks - below the 15% market expectation and slightly inferior to Novo's oral candidate at a much shorter measurement window. According to Lilly's CEO David Ricks, the company's goal "was to create an oral pill that was convenient and can be made at a huge scale, really, for the mass market, and had weight loss that was competitive with other single-acting GLP-1s." That's an honest framing, but it's also a concession that orforglipron won't match injectable efficacy. About 10.3% of patients on the highest dose discontinued due to side effects - a tolerability concern that Pfizer's failed oral candidate danuglipron demonstrated can be disqualifying (Pfizer abandoned its program in October 2025 after 40%+ dropout rates).

If Novo launches its oral obesity pill ahead of Lilly - which current timelines suggest - it would mark the first time in this competitive cycle that Novo has the timing advantage in a new product category. For a stock trading at 14x earnings, that optionality is barely priced in.

Next-Generation Molecules: The Triple Agonist Race

Beyond orals, both companies are developing next-generation injectable candidates that target 25%+ weight loss - approaching what was previously only achievable with bariatric surgery.

Novo's CagriSema - a combination of semaglutide with the amylin analogue cagrilintide - was expected to be the company's breakthrough candidate. Phase 2 data had shown promise for 25%+ weight loss. But Phase 3 results disappointed, delivering 15.7-22.7% weight loss over 68 weeks - essentially matching Lilly's existing tirzepatide rather than leapfrogging it. The market punished Novo severely for this miss, but the narrative may be overblown: 22.7% at the high end is still a competitive result, and the drug could find its niche in patients who plateau on semaglutide alone. Target launch remains 2027.

Novo's Amycretin - a GLP-1/amylin dual agonist - showed a more encouraging 13% weight loss at just 12 weeks in Phase 1, an early trajectory that could yield substantially higher results at longer durations. It has advanced to Phase 3. And then there's Novo's most speculative but potentially transformative bet: semaglutide for Alzheimer's disease. A large Phase 3 clinical trial is expected to deliver results in late 2025. There is currently no meaningful treatment for Alzheimer's - only symptom management. The market is estimated at $5.5 billion and growing at 15% annually. Even modest efficacy would generate a multi-billion dollar opportunity and fundamentally change Novo's diversification narrative.

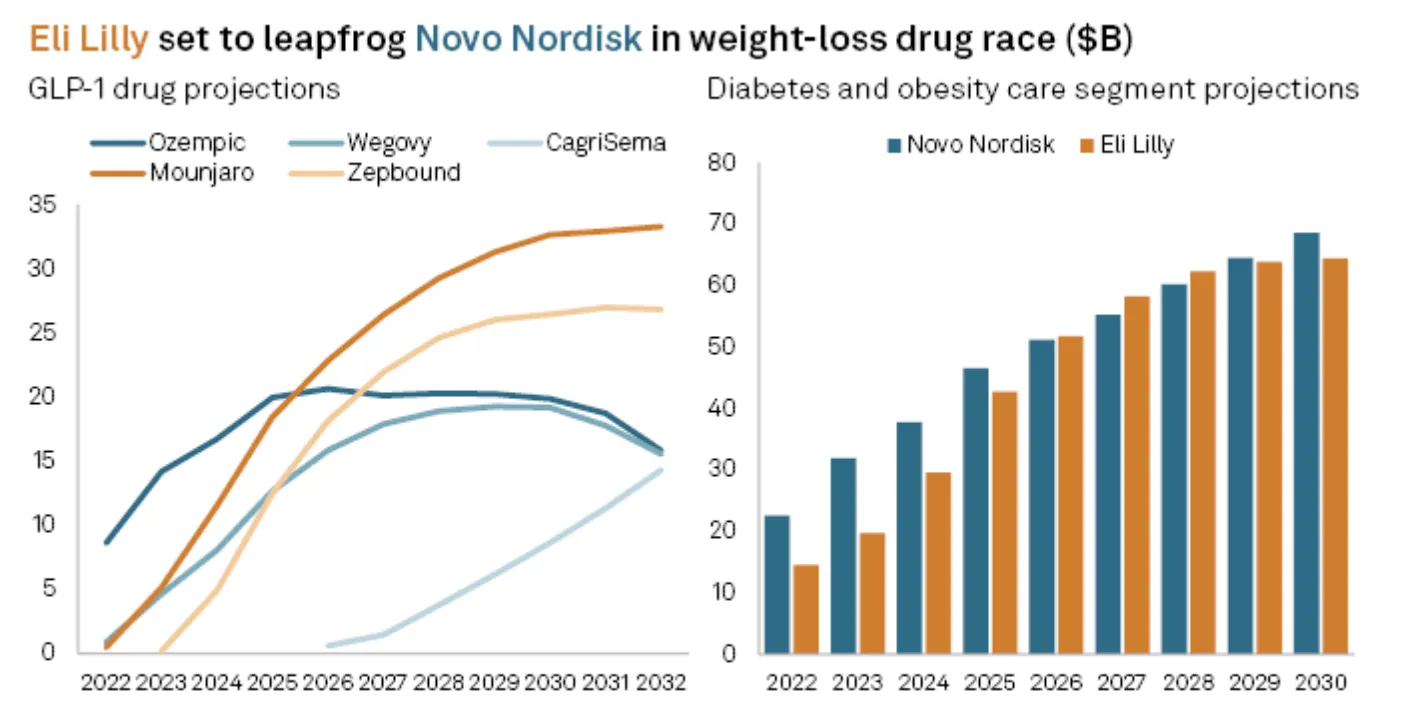

Lilly's Retatrutide - a triple agonist targeting GLP-1, GIP, and glucagon receptors simultaneously - produced 24% weight loss at 48 weeks in Phase 2 trials. If this holds in Phase 3 (data expected 2027), retatrutide could become the most effective anti-obesity drug ever approved. Lilly is also pursuing expanded indications for tirzepatide: the sleep apnea trials completed successfully in May 2025, opening another market, and high-dose formulations (15mg and 20mg) showing 25%+ weight loss could receive separate approval for severe obesity.

Pipeline Verdict

Both pipelines are deep and competitive. Lilly has the edge on next-gen injectable efficacy (retatrutide at 24%), while Novo has the edge on oral timing and the Alzheimer's wildcard. Neither company faces a pipeline gap - the risk is execution, not innovation. The market, however, is pricing Lilly's pipeline at a significant premium while treating Novo's optionality as nearly worthless. That asymmetry is the opportunity.

Manufacturing: The War You Don't See

In most pharmaceutical competitions, the better drug wins. In the GLP-1 market of 2025-2027, the winner is determined by something far more prosaic: whoever can produce the most doses. Demand has consistently outstripped supply since Wegovy launched in 2021, and both companies are engaged in the largest manufacturing buildout in pharmaceutical history to close the gap.

GLP-1 drugs aren't simple small molecules you can stamp out in a generic facility. They require complex biologic production - protein fermentation, sterile fill-finish lines, intricate cold-chain logistics, and quality control processes that take years to validate. Building a new GLP-1 production plant from scratch takes 4-7 years. This is the real moat protecting the Novo-Lilly duopoly, and it's why new entrants - however promising their molecules - face a manufacturing barrier that money alone can't solve quickly.

Novo Nordisk is spending more in absolute terms: approximately $25 billion in CapEx over 2024-2027, spread across three new plants in Denmark (including the massive Kalundborg 2.0 expansion at $6.5 billion), the Chartres fill-finish expansion in France, a $4.1 billion facility in North Carolina to establish a US production base, and expansions in Brazil and China. The company's CapEx guidance for 2025 alone is DKK 55-65 billion (~$8-9.5 billion). Novo's advantage here is institutional: decades of experience with high-volume production on API and mammalian cell platforms creates economies of scale that are difficult to replicate.

Eli Lilly is spending less ($18 billion) but growing faster - targeting 5-6x capacity expansion by 2027 versus Novo's 3-4x. The key differentiator is Lilly's modular approach. The LEAP Innovation Center in Indiana ($4.5 billion) uses plug-and-play manufacturing pods that can scale more rapidly than traditional facilities. Lilly also gained instant capacity through the $2.7 billion Boehringer Ingelheim Alzey plant acquisition in Germany, bypassing the years-long construction timeline entirely. As a US-based company, Lilly's domestic manufacturing investments also position it favorably in the current political environment of tariff threats and onshoring directives.

| Metric | Novo Nordisk | Eli Lilly |

|---|---|---|

| Total CapEx (2024-2027) | ~$25 billion | ~$18 billion |

| Capacity Increase Target | 3-4x by 2027 | 5-6x by 2027 FASTER |

| Key Strategy | Scale existing expertise (Denmark core) | Modular pods + acquisitions (US-centric) |

| US Manufacturing Base | North Carolina ($4.1B, 2026-2029) | Indiana ($8.2B across 2 sites) LARGER |

| Current Supply Status | Constraints easing; Wegovy 2.4mg improved | Zepbound 15mg now readily available |

The supply picture is improving for both companies. Novo's Wegovy availability has materially improved through 2025, and Lilly's Zepbound - previously back-ordered for months in higher doses - is now readily available in its 15mg formulation. By late 2026, the consensus expectation is that Lilly will close the supply gap and potentially achieve manufacturing parity or a slight advantage. But Novo's higher absolute production base means it will likely remain the volume leader through 2027, even as Lilly grows faster in percentage terms.

For investors, the manufacturing build-out creates a paradox. The spending is necessary to meet demand, but it also compresses free cash flow in the near term. Novo's EBIT-to-FCF conversion ratio dropped from 87% (2022) to 55% (2024) as CapEx surged - though it's expected to normalize back to 76% by 2026 as the largest plant investments complete. Lilly faces a similar dynamic. The companies that spend the most now will produce the most later - but the market is discounting Novo's spending as a weakness while rewarding Lilly's as a sign of ambition.

Market Share: The Shifting Balance of Power

The most visible measure of this competitive battle is prescription market share - and here, the trend has been unmistakable. Eli Lilly has been gaining ground relentlessly.

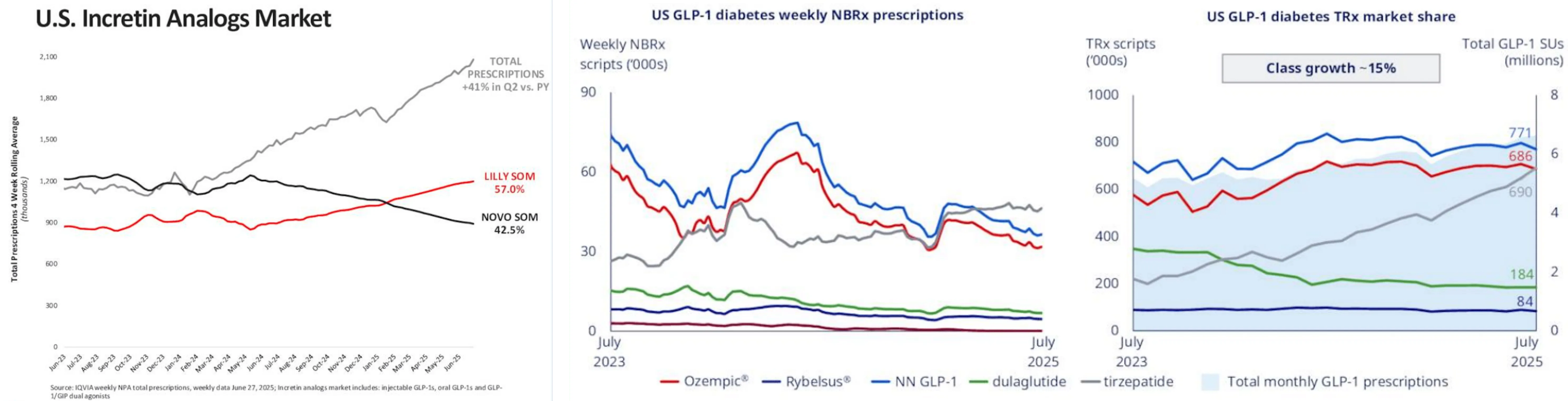

As of Q2 2025, Lilly commands approximately 57% of the US incretin analogs market (including both diabetes and obesity indications), compared to Novo's 42.5%. Total prescriptions in the incretin category rose 41% quarter-over-quarter, but Lilly captured the lion's share of that growth. In the US obesity segment specifically, Zepbound's weekly prescriptions now exceed Wegovy's by over 100,000 scripts. Wall Street consensus estimates place Lilly overtaking Novo in total GLP-1 drug revenue by 2025, with Mounjaro sales forecast at $18.4 billion and Zepbound at $12.5 billion - for a combined $30.9 billion versus Novo's GLP-1 portfolio of roughly $24-26 billion.

But the US isn't the whole story. Novo's international operations have been a bright spot that the headline market share numbers obscure. Wegovy launched in around 35 countries (including India) with additional rollouts expected in H2 2025, and international obesity care revenue surged 125% year-over-year. Ozempic is now available in approximately 80 countries, and Rybelsus has launched in more than 40. In Europe, Canada, and Asia, where Lilly's presence is smaller and its drugs launched later, Novo retains significant leadership. And here's a strategic nuance: Novo's lower international pricing - Ozempic at approximately $93 versus Mounjaro's lowest dose at £129 (roughly $174 equivalent) - makes it the more competitive option in price-sensitive markets, particularly as Lilly raises international prices to comply with the Trump administration's "Most Favored Nation" directive.

The Political Wildcard: Trump, Tariffs, and Drug Pricing

The GLP-1 market now operates in an explicitly political environment, and both companies are navigating unprecedented regulatory pressure.

In early August 2025, President Trump sent letters to 17 major pharmaceutical company CEOs - including both Novo and Lilly - demanding they extend "Most Favored Nation" pricing to US consumers, effectively requiring companies to offer American patients the lowest price they charge in any peer country. The companies were given 60 days to comply, with Trump warning he would "deploy every tool in our arsenal" if they refused. This followed his May executive order directing HHS to produce price targets within 30 days.

The practical implications differ for each company. Lilly, as a US-based firm with expanding domestic manufacturing, is better positioned to navigate onshoring requirements and may benefit from a political environment that pressures foreign competitors more heavily. Novo, headquartered in Denmark with its primary production base in Europe, faces a more complicated calculus - though its $4.1 billion North Carolina facility investment signals a recognition that US manufacturing presence is now a strategic necessity, not just an operational convenience.

Both companies have already moved toward lower consumer pricing, with self-pay options around $499/month through pharmacy benefit programs. Analysts expect oral versions, when launched, to be priced in the $400-600 range. The pricing pressure is real, but it's worth noting that even at $499/month, the unit economics remain highly profitable given Novo's 83%+ gross margins and Lilly's improving cost structure.

The Coverage Gap: Medicare and the $45 Billion Catalyst

The single largest market expansion catalyst for both companies isn't a new drug - it's a change in law. Current US legislation (dating to 2003) explicitly excludes weight loss drugs from Medicare Part D coverage, locking out 65 million Americans from the fastest-growing therapeutic category in pharma.

The bipartisan "Treat and Reduce Obesity Act" would eliminate this exclusion, treating obesity as a chronic disease eligible for Medicare coverage. If passed, the impact would be transformational: an estimated 15-20 million new patients covered, roughly $45-60 billion in additional annual market size by 2030, and an immediate stock price catalyst of 15-25% for both Novo and Lilly. The bill has bipartisan support but faces budget concerns - the most likely outcome is phased coverage with cost-sharing requirements, similar to the Medicare Part D insulin cap.

| Coverage Type | Wegovy (Novo) | Zepbound (Lilly) |

|---|---|---|

| Medicare Part D | Not covered (obesity exclusion) | Not covered (obesity exclusion) |

| Private Insurance (Obesity) | ~40% of plans | ~35% of plans |

| CV Risk Reduction | 70%+ coverage SELECT DATA | Pending SURPASS-CVOT (2026) |

| Self-Pay Price | $499/mo (GoodRx partnership) | ~$499/mo (direct program) |

There's one coverage advantage Novo holds today that is often underappreciated. Because Wegovy has proven cardiovascular benefit data from the SELECT trial, over 70% of private insurance plans cover it when prescribed for cardiovascular risk reduction - not just weight loss. This is a meaningful commercial advantage: doctors can prescribe Wegovy to obese patients with cardiovascular risk factors and bill insurers under a covered indication, even though the patient's primary motivation may be weight loss. Lilly will likely match this advantage once SURPASS-CVOT data arrives in 2026, but for now, Novo has an 18-month head start in building prescribing relationships with cardiologists and insurers.

Investment Analysis: The Asymmetric Opportunity

We've laid out the competitive dynamics - efficacy, pipeline, manufacturing, market share, politics. Now the question that matters most to investors: where is the asymmetry? Where has the market priced in too much pessimism, and where has it not priced in enough risk?

The Patent Clock: A Structural Divergence

One factor that doesn't get enough attention in the headline comparison is patent protection - and here, the difference between the two companies is stark. Novo Nordisk's core patent protection for Ozempic and Wegovy (semaglutide) in the US and EU extends to 2031/2032. In key international markets - Canada and China - protection is already expiring as soon as 2026. This creates a finite window for Novo to maximize its branded franchise before biosimilar competition begins eating into revenues post-2031. The consensus revenue revision chart tells this story bluntly: analysts project Novo's revenue declining from 2031 through 2033 as patent cliffs bite.

Eli Lilly's tirzepatide patent extends to at least 2039 in the United States - giving it seven to eight additional years of branded exclusivity beyond Novo's semaglutide. That's an eternity in pharmaceutical investing. It means Lilly can amortize its $18 billion manufacturing investment over a longer revenue runway, and it explains much of the valuation premium the market assigns to Lilly's growth story.

However, Novo has counter-moves. The company holds competitive advantages over biosimilars that aren't easily replicated: decades of R&D in-house expertise, strict EU regulatory requirements for biologics, complex drug and device manufacturing know-how, and large fragmented target audiences that favor established brands. Novo's next-generation candidates - amycretin, oral semaglutide for obesity - would carry their own fresh patent protection well into the 2030s, partially offsetting the semaglutide cliff. And if the Alzheimer's trial succeeds, it would create an entirely new patent-protected revenue stream using the existing semaglutide molecule.

The Competitive Moat: Who Threatens the Duopoly?

Both companies benefit from a moat that is often underestimated: the sheer difficulty of entering the GLP-1 market. Manufacturing barriers alone require 4-7 years to overcome. But several challengers are advancing, and the timeline matters.

The nearest-term threats are Viking Therapeutics (VK2735), a small biotech with strong Phase 2 data whose injectable showed 15.7% weight loss at 13 weeks, and Amgen's MariTide, a monthly-dose antibody-based GLP-1/GIP dual agonist in Phase 3. Viking is projected to begin generating revenue from 2028, while Amgen's candidate - if Phase 3 succeeds - could launch by the end of the decade. Further out, Metsera's MET-233i targets 2029, and Roche's oral CT-388 and Structure Therapeutics' GSBR-1290 won't arrive before the next decade. Innovent Biologics' mazdutide has launched in China but faces a long path to US/EU approval.

Critically, Pfizer's exit from the oral GLP-1 space - abandoning danuglipron in October 2025 after 40%+ discontinuation rates - validates how difficult it is to bring a competitive product to market. The Novo-Lilly duopoly will likely hold at 80%+ combined market share through at least 2028, and potentially longer.

The Investment Case: Side by Side

Novo Nordisk - The Deep Value Case

Novo at $56 is trading at a forward P/E of 14x - a 57% discount to its own 5-year average of 31x. The stock needs just 1% annual growth to justify its current valuation. Even conservative estimates of 10-11% revenue growth produce a fair value of $60-68 per share, with bull-case scenarios (involving oral obesity launch, Alzheimer's success, and eventual valuation normalization toward the 10-year P/E mean of 24.7x) pointing to price targets of $114 or higher - a potential doubling from current levels.

The dividend yield has risen to 2.35% - well above the 5-year average of 1.77% - and consensus estimates project steady dividend growth from $1.89 in 2025 to $2.11 by 2027. With near-zero debt (D/E of 0.05), industry-leading margins, and a balance sheet that can absorb $25 billion in CapEx without strain, Novo offers genuine downside protection alongside substantial upside optionality.

Fair Value Range: $60 - $68 (base) | $114+ (bull, normalized P/E)

Eli Lilly - The Growth Premium Case

Lilly at ~$700 trades at a forward P/E of 31x - elevated versus the S&P 500 but actually below its 5-year average of 43.6x. The PEG ratio of 0.87x - well below the 5-year mean of 2.09x - suggests the market is actually underpricing Lilly's growth relative to historical norms. Consensus projects 42% EPS CAGR through 2027, driven by tirzepatide momentum, retatrutide Phase 3 data, and Kisunla (Alzheimer's) revenue ramp.

The key advantage is diversification and patent runway. Lilly's tirzepatide protection to 2039 provides nearly a decade of additional branded exclusivity versus Novo. Its Alzheimer's franchise alone could generate $10B+ in peak sales. Insiders were buying at the $620s in August 2025, signaling confidence from those closest to the business. But the valuation assumes 18% annual growth for seven years - any meaningful stumble compresses the multiple sharply.

Price Target: $1,050 (based on FY2027E EPS of $37.50 × ~28x P/E)

What Could Go Wrong: The Risks That Matter

No investment thesis is complete without an honest assessment of what could break it. Both companies face overlapping and company-specific risks that deserve frank discussion.

For both companies: Medicare's refusal to cover obesity drugs would constrain the addressable market by an estimated 40%. Drug pricing legislation - while unlikely to pass in its most aggressive form - could cap profit margins. Long-term GLP-1 safety data is still accumulating; rare but serious side effects (thyroid concerns, pancreatitis, bowel obstruction reports) could emerge at scale and trigger regulatory action or litigation. And the compounded GLP-1 market - which Novo's previous CEO described as "equal size to our business" at "much lower price points" - represents a persistent threat that neither company has fully neutralized despite aggressive legal action.

For Novo specifically: the risk is continued downward estimate revisions. The company has already cut 2025 guidance twice, and each cut has triggered double-digit sell-offs. If Novo fails to stabilize growth expectations - particularly if oral semaglutide approval is delayed or international expansion decelerates - the stock could test the $40-44 level again, which would represent a PEG-ratio bear case. The new CEO must demonstrate "speed and ambition" quickly, or the leadership transition itself becomes a risk factor.

For Lilly specifically: the risk is execution on an $18 billion manufacturing buildout while simultaneously running Phase 3 trials for retatrutide, expanding Kisunla, and navigating international price increases. A clinical trial failure - particularly for the SURPASS-CVOT cardiovascular outcomes study - would remove a major expected catalyst and likely trigger a sharp multiple compression from 31x toward the mid-20s. Lilly's higher leverage (D/E of 0.82) also means less financial flexibility in a downturn.

The Verdict

The market has set up a seductive narrative: Lilly is winning, Novo is losing, buy the winner and sell the loser. Reality is more nuanced. Both companies are dominant. Both have deep pipelines. Both will benefit from a market that's still in its first inning of penetration. The question isn't which company is better - it's which stock is better priced.

By almost every valuation metric, Novo Nordisk offers the more compelling risk-reward at current levels. A company trading at 14x earnings in the fastest-growing pharmaceutical market in history, needing 1% growth to justify its price, with up to 77% upside to fair value - that's not a falling knife, that's a mispricing. Novo's risks are real (concentration, patent cliff, guidance cuts), but the market has priced in a worst-case scenario that the fundamentals don't support.

Eli Lilly is the higher-quality business by most measures - better efficacy, longer patents, greater diversification. But quality has a price, and at 31x forward earnings requiring 18% growth for seven years, Lilly's margin of safety is thinner. The stock is likely to outperform if everything goes right. Novo is likely to outperform even if some things go wrong.

"Own both. But the asymmetry favors Novo Nordisk at current prices. A company doesn't need to win the GLP-1 war to be a great investment - it just needs to not lose it. And at 14x earnings, the market is pricing Novo as though it already has."

- PolyMarkets Investment, Research Team

Scorecard: Where Each Company Leads

| Dimension | Leader | Why It Matters |

|---|---|---|

| Injectable Efficacy | Lilly | 20-22% vs 15-17% weight loss drives prescribing preference |

| Cardiovascular Data | Novo | SELECT trial = 70%+ insurance coverage advantage (for now) |

| Oral Drug Timeline | Novo | Oral Wegovy launching ahead of orforglipron; 62-78% patient preference for pills |

| US Market Share | Lilly | 57% vs 42.5% and gaining ~2-3% per quarter |

| International Reach | Novo | Ozempic in 80 countries, Wegovy in 35; 125% international growth |

| Profitability | Novo | 44-48% operating margin vs 28-40%; 83%+ gross margin |

| Patent Runway | Lilly | Tirzepatide protected to 2039 vs semaglutide 2031/32 |

| Diversification | Lilly | Alzheimer's, oncology, immunology reduce single-therapy risk |

| Manufacturing Ramp | Lilly | 5-6x capacity growth vs 3-4x; modular approach scales faster |

| Valuation / Risk-Reward | Novo | 14x P/E (57% below 5Y avg) vs 31x; 77% upside to fair value |

The Bottom Line

The GLP-1 revolution is real, massive, and still in its earliest innings. Of the 890 million adults globally living with obesity, barely 1-2% are currently treated with these drugs. The market will grow for decades as manufacturing scales, prices decline, insurance coverage expands, and oral formulations make treatment accessible to hundreds of millions more patients. Both Novo Nordisk and Eli Lilly will be major beneficiaries of that secular trend.

But the stocks are not the same investment. Lilly is the consensus pick - the company with superior efficacy, faster growth, longer patents, and broader diversification. That consensus is reflected in its 31x forward P/E and $629 billion market cap. Nothing about that thesis is wrong. It's just already in the price.

Novo is the contrarian pick - the company the market has left for dead. Down 61% from its highs, trading at half the multiples of its own history, with a new CEO, trimmed guidance, and an eroding US market share. All of that is true. But so is this: Novo needs 1% growth to justify its valuation. It operates in a $150 billion market growing at 25% annually. It has the leading oral obesity candidate, a potential Alzheimer's breakthrough, 44% operating margins, and zero meaningful debt. When the fear fades - and it will - the re-rating could be substantial.

We recommend owning both. But at today's prices, the asymmetric opportunity is in Novo Nordisk. Not because it's the better company. Because the gap between what the market is pricing and what the fundamentals support has never been wider.

"Be fearful when others are greedy, and greedy when others are fearful. The market is fearful on Novo Nordisk. The math says it shouldn't be."

- PolyMarkets Investment, Research Team

⚠️ Investment Disclaimer

This article is for educational purposes only and does not constitute financial or medical advice. Pharmaceutical stocks are volatile. Clinical trial failures, regulatory setbacks, or manufacturing issues can cause sharp declines. GLP-1 drugs have known side effects and are not appropriate for all patients.

Do your own research. Consider your risk tolerance and investment timeline. Consult a financial advisor before making investment decisions. Past performance does not guarantee future results.

Research Desk, PolyMarkets Investment, August 29, 2025