McKinsey projects companies will invest $7 trillion in computing capability over the next five years. Not a typo. The AI arms race has created a silicon demand environment that has no real modern precedent - and the semiconductor industry sits right at the center of it, supplying the picks and shovels for a transformation every sector of the global economy is simultaneously racing to fund.

Here's the problem with calling it "the semiconductor sector" as if it were one investment: that's like calling healthcare a single investment. The label covers completely different business models that happen to share a supply chain. ASML and NVIDIA are both semiconductor companies. So are Entegris and Intel. Their risk profiles, margin structures, competitive dynamics, and sensitivity to the AI cycle are entirely distinct from each other. The investor who made 39% on NVIDIA this year and the investor who watched Intel bounce 80% from its April low? They were not investing in the same thing, even if both call it "a chip stock."

This piece maps the full value chain - all six sub-sectors - identifies where the structural advantages actually sit, which companies are capturing them, and what the forward setup looks like for an industry that the global economy simply cannot function without.

The AI Arms Race and What It Means for Silicon

The AI spending narrative has gotten repetitive at this point - but the numbers underneath it remain genuinely unprecedented. Every hyperscaler - Microsoft, Amazon, Google, Meta - has publicly committed to multi-year, multi-hundred-billion-dollar capex programs for data center buildout. And the primary bottleneck is always the same thing: chips. Advanced GPUs for training and inference, high-bandwidth memory to feed them, and the custom silicon increasingly sitting alongside them to handle networking, storage, and proprietary workloads. More AI means more chips. That's essentially it.

The global semiconductor market is tracking toward roughly $700 billion in sales in 2025. What the industry calls a "multispeed recovery" - AI and data center growing explosively while consumer electronics, automotive, and industrial segments claw back from the 2023 inventory hangover more gradually. That bifurcation is the whole investment point. An undifferentiated sector position captures the explosive parts and the sluggish ones at the same time. Knowing which sub-sector you're actually in changes the return profile dramatically.

"The AI inflection has turned the semiconductor sector into a six-ring map where the investment merits are completely different in each ring. NVIDIA dominates GPU compute. TSMC manufactures what nobody else can. ASML sells the only tool that makes TSMC possible. EDA software companies design the pipeline for all of it. Understanding which ring you're buying - and what it's worth - is the entire analytical challenge. The investors who fail are the ones who buy 'semiconductors' without that map."

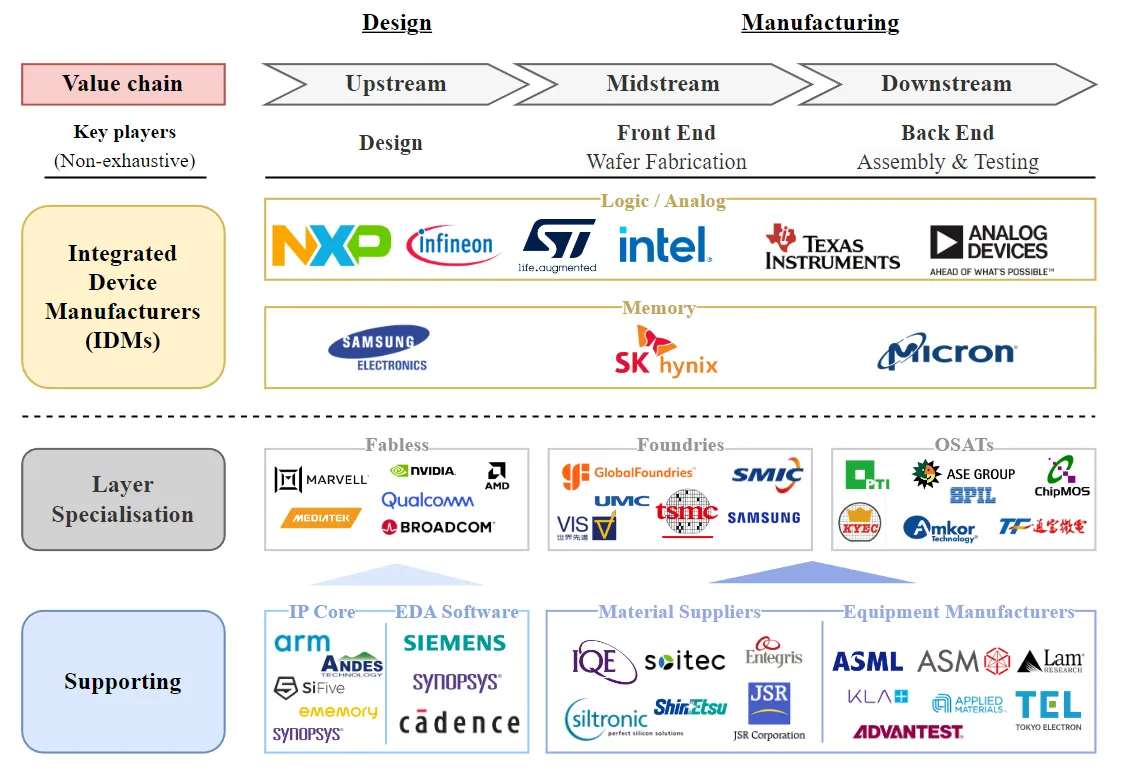

The Value Chain: A Reference Map

Before looking at individual companies, anchor yourself in the physical structure of how a chip gets made. The competitive dynamics at each stage are completely different. The structural advantages that make certain companies genuinely irreplaceable only become legible once you understand exactly where they sit in the chain.

The diagram surfaces a structural insight most retail investors miss entirely: the companies with the best long-term returns are frequently not the largest or most recognizable names. ASML, a Dutch equipment company most people couldn't name, is arguably the single most important company in the entire semiconductor supply chain. Without its EUV lithography machines, nobody manufactures chips at 5nm or below. Period. Synopsys and Cadence - barely known outside the industry - collectively control the design software without which chip production at any leading node is flatly impossible. They are not supporting characters. They're chokepoints. And chokepoints are where pricing power lives.

Six Sub-Sectors: Where the Advantages Sit

Equipment Suppliers

The companies that build the machines that build the chips. New fab: $15-20 billion. Every new process node triggers a new equipment cycle. Recurring demand every 2-3 years as chip complexity keeps advancing. Oligopolistic structure with moats that are essentially unassailable - you cannot substitute ASML's EUV machines with anything else that exists on earth.

Foundries & Fabs

The factories that manufacture what chip designers create. TSMC controls over 60% of the world's advanced-node production - a concentration that is simultaneously the sector's greatest single asset and its most significant geopolitical risk. AI demand is driving a real capacity crunch, and foundries are pricing accordingly. Supply can't keep up with demand. That's not going to change quickly.

Integrated Device Manufacturers

Companies that both design and manufacture their own chips. Intel is the defining example - a company whose struggles and potential recovery define one of the most debated investment questions in the sector right now. Meanwhile, Texas Instruments quietly compounds in analog. STMicro serves automotive. Different stories, same category label.

Fabless Designers

No fabs. Pure IP. The biggest winners of the AI era, broadly speaking. They design chips that TSMC manufactures - capturing the upside of silicon demand without the $20 billion capital burden of running a fab. NVIDIA and Broadcom are the defining names. AMD and Qualcomm are the challengers, each with their own distinct narrative and their own ceiling.

EDA & IP Tools

Before any chip gets designed, somebody builds the software to design it. Synopsys, Cadence, and Siemens effectively run a near-monopoly on EDA tools. ARM's processor IP runs in virtually every smartphone on earth and is aggressively expanding into data centers. High margins. High switching costs. Low capital intensity. Structurally, the most attractive business model in the entire sector - which is why most people never talk about it.

Materials & Speciality Suppliers

Ultra-pure silicon wafers, specialty gases, photoresists, filtration chemicals - the consumables without which every fab stops dead. These companies fly completely under the radar but benefit from every capacity expansion regardless of who wins the chip wars. Shin-Etsu is the world's largest silicon wafer supplier. Entegris dominates ultra-pure chemical delivery. Demand is directly tied to fab buildout. Simple as that.

The Titans: Company Profiles with 2025 Data

NVIDIA Corporation

The undisputed leader in AI accelerated computing

NVIDIA's financials in 2025 read less like an earnings report and more like a resource survey - each quarter revealing the deposit goes deeper than previously mapped. Q3 FY2025 revenue hit $35.1 billion, up 94% year-over-year. Data Center alone generated $30.8 billion, up 112%. The stock reached an all-time high near $187 in early October 2025, building on a 208% surge in the prior year. Conventional valuation frameworks don't handle numbers like this well, frankly. They reflect a company that found itself at the precise intersection of every major capex cycle happening simultaneously across every major economy on earth.

The product roadmap keeps compounding the advantage. Hopper GPU demand is still extraordinary. Blackwell systems are ramping into a market that has been waiting for them impatiently - supply constraints on High Bandwidth Memory were the primary throttle on Blackwell production, not demand. Not even close to a demand problem. NVIDIA's $26 billion data center infrastructure commitment and its $5 billion investment in Intel (securing a 4% stake, guaranteeing a domestic manufacturing partner) show a company thinking in decades, not quarters. China export controls - Blackwell AI GPUs restricted from sale there - remain an overhang. Bank of America analyst Vivek Arya's framing nails it: "The daily noise around China restrictions is unhelpful but irrelevant to the near/medium financial estimates." The TAM outside China is already too large to need it.

Advanced Micro Devices

NVIDIA's most credible challenger in AI accelerators

AMD's 2025 narrative is genuinely interesting - a company that is legitimately competitive with NVIDIA in AI accelerators but cannot yet command NVIDIA's pricing power or ecosystem lock-in. Q2 2025 revenue of $7.7 billion was up 32% year-over-year, with Data Center contributing $3.2 billion. AMD projects $9.5 billion in AI-related revenue for 2025, driven by the MI300X series and the upcoming MI350. The 108% rally from the April 2025 low reflects both the fundamental delivery and a growing market recognition that hyperscalers genuinely want a second AI chip vendor - they don't want to be permanently dependent on one supplier for infrastructure this critical.

CPU business is still strong - AMD keeps taking server market share from Intel. The risk is essentially the mirror image of NVIDIA's position: AMD needs the MI350 to compete credibly at the highest tier of AI workloads, and its software ecosystem (ROCm) still lags CUDA meaningfully in developer adoption. Export controls on MI308 China shipments add geopolitical complexity on top. But the core thesis hasn't changed and still holds. Hyperscalers will not accept a world with only one AI GPU vendor. AMD is the primary beneficiary of that structural imperative.

Taiwan Semiconductor Manufacturing

The irreplaceable bottleneck of the global chip supply chain

TSMC is the company that makes all of this possible. Apple's A-series chips, NVIDIA's H100 and Blackwell GPUs, AMD's Ryzen and Instinct processors, Qualcomm's Snapdragon - every one of the semiconductor industry's most consequential products runs through TSMC's fabs. The 30.6% Return on Investment in 2025 reflects a business that is both structurally dominant and physically struggling to keep up with AI demand that keeps surprising to the upside. TSMC is doubling its CoWoS (Chip-on-Wafer-on-Substrate) advanced packaging capacity in 2025, with NVIDIA set to get 50% of the incremental supply. And even that expansion is expected to fall short of demand.

The strategic picture is more complicated. TSMC's $40 billion Arizona facility - pushed to 2028 due to construction complexity - and $6.6 billion in CHIPS Act funding reflect a US government that has figured out it cannot accept having the world's most critical technology concentrated in a geopolitically sensitive location. TSMC's Taiwan location is the single most discussed risk factor in the sector. The investment thesis on TSMC is not really about financial performance - that's already exceptional, and nobody disputes it. It's about whether geopolitical risk is adequately priced into the valuation. For most periods since 2022? The answer has been no.

Broadcom Inc.

Custom AI silicon and networking - the strong second player

Broadcom has quietly put together the most compelling AI infrastructure story outside of NVIDIA. Its custom AI ASIC business - designing application-specific chips for hyperscalers who want alternatives to NVIDIA's off-the-shelf GPUs - is growing at 63% year-over-year and generated $5.2 billion in Q3 FY2025 alone. A new $10 billion custom chip agreement with OpenAI has been announced, signaling that the largest AI labs are actively diversifying their silicon strategies. And Broadcom's networking chips - which move data between the thousands of GPUs inside a modern AI cluster - represent a chokepoint in the hyperscaler buildout that is arguably as important as the GPUs themselves. Arguably.

What makes Broadcom particularly interesting is the breadth. The VMware acquisition (completed 2023) added a significant enterprise software revenue stream - recurring subscription cash flows that smooth out the cyclicality baked into semiconductor hardware. Custom AI silicon plus networking infrastructure plus enterprise software. That combination is genuinely unusual. The market has recognized it: up 47% year-to-date in 2025, and management's description of the company as the "strong second player" to NVIDIA in AI is getting validated by the revenue line every single quarter.

Micron Technology

HBM leadership - the memory story AI can't tell without

The memory industry's 2025 revival is being driven by a product that barely existed at commercial scale three years ago: High Bandwidth Memory. HBM is the stacked DRAM that sits directly on every high-end AI GPU, feeding it data at speeds conventional memory cannot get anywhere near. Without HBM, the H100 and Blackwell systems that power modern AI training simply don't function. Micron, SK Hynix, and Samsung are the only three companies on earth that manufacture it - and all three are running at full capacity. Micron's Q3 FY2025 revenue of $9.30 billion (up 37% year-over-year) was propelled by HBM nearly doubling sequentially, with data center revenue more than doubling year-over-year to a quarterly record.

Micron's competitive position is structurally strengthening. The company expects its HBM market share to reach its overall DRAM share by H2 2025 - a major gain relative to SK Hynix's current dominance in that specific segment. The $30 billion US investment plan, partially funded by CHIPS Act support, sets up a multi-year capacity expansion cycle. The risk is memory's notorious cyclicality: when AI investment eventually moderates, HBM oversupply can compress margins very quickly. But the demand runway ahead of this particular cycle is longer and more durable than previous memory upcycles, which were mostly driven by consumer electronics. AI training demand is a different animal entirely.

The Hidden Compounders: EDA, Equipment, and Materials

The most analytically interesting part of the semiconductor value chain is not the companies most investors talk about. It's the three sub-sectors sitting upstream of chip manufacturing itself: equipment suppliers, EDA software, and materials. These businesses share a structural characteristic that is genuinely rare in any industry: they benefit from every dollar of capex without bearing the full execution and cyclical risk of whoever is doing the spending. They get paid regardless of who wins.

ASML - The Only Game in Town

ASML Holding is the only manufacturer of Extreme Ultraviolet (EUV) lithography machines in the world. The only one. EUV enables chip production at 5nm, 3nm, and below - the nodes on which every leading AI chip is manufactured today. A single EUV system costs over $150 million and requires years of lead time to deliver. The order book consistently grows. EUV adoption remains in relatively early stages despite decades of development. ASML's competitive position isn't "strong" or "leading" - it is physically unique. No other company can threaten it in its core market because the barriers to replication are measured in decades of accumulated engineering knowledge, not capital. You cannot build what ASML builds by throwing money at the problem. The recent pullback from 2024 highs has been flagged by multiple analysts as a compelling entry point for a business with this caliber of structural moat.

Synopsys, Cadence & ARM - The Invisible Pipeline

Before NVIDIA can tape out a Blackwell chip, engineers spend 18-24 months designing it using Synopsys and Cadence's EDA software. These tools simulate, verify, and optimize every circuit before a single silicon wafer gets touched. Without them, modern chip design at any advanced node is simply not possible. Both companies run high-60s to mid-70s gross margins, recurring subscription revenue, and switching costs that are measured in years. Chipmakers don't swap EDA vendors mid-project. Usually not between projects either. ARM goes further: its processor designs run in virtually every smartphone on earth and are rapidly expanding into data center servers via the Neoverse platform. Each ARM-based chip that ships generates a royalty. The total addressable market for ARM's architecture has genuinely never been larger than it is right now.

The Bloomberg Research framing captures it well: EDA companies have "some of the biggest benefits of what made fabless designers so successful - low overhead costs and high margins - while being crucial enablers of the AI revolution." That's exactly right. These are software businesses with semiconductor sector growth exposure, not semiconductor businesses that happen to have software-like margins. That distinction matters. And it's worth paying for.

Intel: The Turnaround Question

Intel is the semiconductor sector's most complex investment case, and it's been that way for three years now. After losing over 60% of its value in 2024 - persistent manufacturing missteps, market share losses in consumer and server CPUs, failure to develop a credible AI GPU business - Intel started a recovery in 2025 that frankly surprised most people who'd been watching it. The stock rallied from an April 2025 low of $17.67 to roughly $35-36 by early October. Near-80% gain. Substantially outperformed every other major semiconductor name over that period.

What drove it? External validation and internal restructuring, combined in a way the market had stopped expecting. NVIDIA's $5 billion investment in Intel - securing a 4% stake - was the most consequential single signal. It tells investors that the company with the deepest understanding of advanced semiconductor manufacturing believes Intel's foundry capability is real and worth backing. That's not nothing. Substantial CHIPS Act funding provides a multi-year runway. Workforce reductions targeting $8-10 billion in annual savings by end of 2025 are beginning to show up in the income statement. The foundry thesis - Intel as a domestic manufacturing alternative to TSMC - remains unproven at commercial scale. But NVIDIA's investment makes it look considerably less theoretical than it appeared in 2024.

Intel - The Bear Case Remains

The recovery is real. The challenges are not resolved. Q3 2024: EPS of -$0.46 on $13.3 billion in revenue. Full-year 2024 produced a net loss of $11.6 billion - the direct cost of running fabs that aren't fully utilized. Intel Foundry Services still has no marquee external customer to validate its technology claims at leading-edge nodes. The foundry business unit is expected to remain loss-making through at least 2026. Investors buying Intel here are betting the turnaround completes - which could be an excellent trade at the right price, but requires accepting substantial execution risk in an industry where the margin for error on technology roadmaps is essentially zero. It always has been.

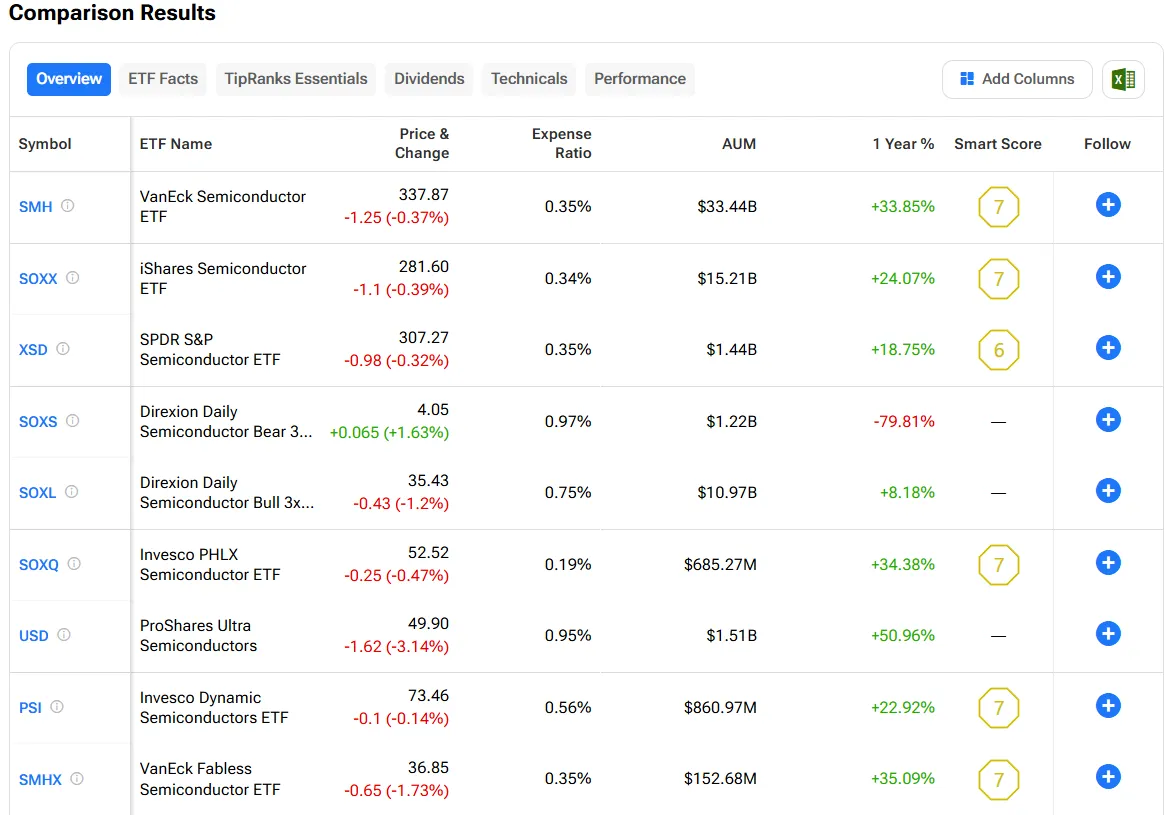

ETF Vehicles: Capturing the Sector

For investors wanting sector exposure without the concentration risk of individual stocks, two ETFs dominate the landscape. Their structural differences matter more than the names suggest.

Choosing between SMH and SOXX is a philosophy decision. SMH holds 26 names with its top 10 positions representing 76% of assets - a concentrated bet on the sector's best-known winners. SOXX holds a broader basket with its top 10 at 60% of assets, giving more exposure to mid-cap names like Credo Technology (its biggest winner, at 1.97% of holdings) that may carry higher growth potential but less established track records. SMH's outperformance over the past year (+33.85% vs +24.07%) reflects the market rewarding concentration in quality. Not always the case. But it was this time.

SMH's net flows of $1.19 billion month-over-month and SOXX's $837.77 million make clear that institutional money is actively building semiconductor exposure - these are not retail-driven inflows. The sector's trailing P/E of 58.6x (5-year average: 41.4x) is a real valuation concern, but it reflects earnings growing fast enough that forward multiples look considerably more reasonable. The question for any new position is simple: do you believe the AI capex cycle continues? If yes, the valuation argument against semiconductors largely dissolves. If you don't believe it continues - well, that's a different conversation.

Geopolitical Risk: Taiwan, Export Controls, and the CHIPS Act

No semiconductor analysis is honest without a direct engagement with the geopolitical architecture of the industry. It is the most significant non-financial risk factor - and the one most commonly glossed over in anything bullish on the sector.

Taiwan Concentration

TSMC manufactures over 60% of the world's advanced semiconductor production from facilities concentrated in Taiwan. Any disruption - military, political, natural disaster - would halt AI infrastructure buildout globally within weeks. No alternative manufacturing base at equivalent technology nodes exists. None could be built in under five years. This risk is real, persistent, and probably underpriced in TSMC's current valuation at any given moment.

US-China Export Controls

The US government has progressively restricted exports of advanced AI chips (H100, Blackwell, MI300) and the equipment needed to manufacture them (ASML EUV machines) to China. This limits revenue across every major US semiconductor company and is simultaneously accelerating China's domestic chip development via SMIC and Huawei Ascend. Escalation raises risk. Relaxation creates upside. The situation is fluid, politically driven, and changes faster than most financial models can account for.

CHIPS Act Execution Risk

$52 billion in US government funding is catalyzing domestic fab construction - TSMC Arizona, Intel Ohio, Micron Idaho. The investment is absolutely real. So is the execution risk. Fab construction in the US runs 50%+ more expensive than in Taiwan, timelines have already slipped (TSMC Arizona pushed to 2028), and the talent pipeline for semiconductor manufacturing engineering does not exist at the required scale. The capital is committed. Delivery is the open question. It will be for years.

China's Counter-Strategy

China is aggressively funding SMIC, YMTC, and Huawei's HiSilicon to reduce dependence on Western chip technology. Current state: SMIC is manufacturing at ~7nm (trailing TSMC's 3nm frontier), YMTC produces competitive NAND flash, Huawei's Ascend AI chips are deployed domestically. The pace of progress has been faster than Western analysts expected back in 2022. Mature node competition (28nm and above) is already intense. Advanced node is the key battleground for the next decade - and the outcome is genuinely uncertain.

Investment Framework: Where to Allocate and Why

The sector's complexity is simultaneously the investment challenge and the opportunity. Because most investors treat it as monolithic - "I own SMH, I'm in semis" - the sub-sector and company-level divergences create persistent mispricing that a more structured approach can actually exploit. The framework below maps more precisely to where the structural advantages actually sit.

| Sub-Sector | Best Vehicle | Structural Advantage | Key Risk | Allocation Logic |

|---|---|---|---|---|

| Equipment (ASML, AMAT, LRCX, KLAC) | Individual stocks | Near-monopoly positions; benefits every capex cycle | Lumpy revenue; capex slowdowns hit hard | Core long-term hold; ASML pullbacks are buying opportunities |

| EDA & IP (SNPS, CDNS, ARM) | Individual stocks | Software margins, extreme switching costs, recurring revenue | Regulatory risk (SNPS/Ansys merger scrutiny) | Highest quality business models in sector - underweighted by most |

| Fabless AI (NVDA, AMD, AVGO) | Individual stocks | IP ownership, AI demand cycle, no fab capex burden | High valuations, competition, geopolitical export limits | Core AI exposure; size based on valuation comfort |

| Foundries (TSMC) | TSM ADR | Irreplaceable manufacturing capability | Taiwan geopolitical risk, permanently priced in insufficiently | Own it, but size it with the geopolitical discount in mind |

| Memory (MU, SK Hynix) | MU for US access | HBM bottleneck for AI training | Memory cycles; oversupply risk when AI capex moderates | Cyclical position, not a permanent core |

| Broad Exposure | SMH ETF | Diversification, lower maintenance | P/E premium; diluted by underperformers | Starting point for less active investors; 20% of sector allocation |

The semiconductor sector's structural growth story is real and durable. But the $7 trillion AI compute buildout is not a rising tide that lifts all boats equally - it is a directed flow that rewards chokepoint ownership above everything else. ASML owns the only tool that makes advanced chips possible. Synopsys and Cadence own the design software. TSMC owns the manufacturing. NVIDIA owns the software ecosystem that makes its GPUs irreplaceable for AI workloads. These are not strong competitive positions - they are near-monopolies in specific niches of a $700 billion market. The investment case is straightforward once you see it: own those chokepoints at prices that don't fully reflect their irreplaceability. And be patient.

The Outlook: What Comes Next

Several catalysts will define semiconductor performance over the next 12-24 months. Q4 2025 earnings from the major players will be the first real test of whether Blackwell ramp-up actually met NVIDIA's production targets. AMD's MI350 availability and initial hyperscaler adoption data will determine whether competitive balance in AI accelerators shifts meaningfully - or whether NVIDIA's ecosystem moat holds. Intel's foundry external customer announcements (or lack thereof) will either validate or deflate the turnaround narrative. Those are the near-term things to watch.

On the structural side, TSMC's CoWoS capacity doubling is the most important single supply event in the near term. It's the packaging technology that makes AI chips work, and its availability constrains how fast the entire industry can scale. The CHIPS Act facilities coming online in 2027-2028 will begin to answer whether US domestic production is economically viable at scale. And China's semiconductor development trajectory will determine how long the current US export control regime is sustainable before it simply accelerates domestic Chinese alternatives past the point where the controls matter.

The longer-term picture involves architectural evolution: chiplets replacing monolithic designs, 3D stacking of memory and logic, neuromorphic computing for specific AI workloads, eventually quantum computing for certain applications. Each transition reshapes competitive positions and creates new chokepoints. The companies that have demonstrated they can navigate technological transitions - ASML, TSMC, NVIDIA - have earned their premium valuations precisely because execution in this industry is extraordinarily rare. Most companies can't do it consistently. These three have.

Analytical Conclusion

The semiconductor sector in 2025 is going through a structural transformation driven by AI demand that is unlikely to reverse on any horizon relevant to most investment frameworks. The sector P/E of 58.6x is high relative to history - but history doesn't contain a $7 trillion compute investment cycle either. You can't use 2015 comps to evaluate 2025 AI infrastructure spending.

The analytical discipline required here is not "should I own semiconductors" - the answer is probably yes - but "which layer of the value chain, and at what price?" Equipment and EDA companies have the most structurally attractive positions: near-monopoly businesses that benefit from every dollar of capex without bearing the full risk of any individual product cycle. Fabless designers at the AI frontier are the highest-growth plays with the highest valuations and highest competition risk. Foundries are indispensable but geopolitically complicated. Memory is cyclical leverage on AI demand - useful sometimes, dangerous others.

The sector is not monolithic. The map matters. Use it.

Research Desk, PolyMarkets Investment, November 2025