1 The Trillion-Dollar Question

Between August 2024 and August 2025, Novo Nordisk's market capitalization fell by roughly two-thirds from its all-time highs, erasing nearly all the value created during its historic GLP-1 expansion. Over the same period, Eli Lilly's share price gained approximately 40%, and the company became the first trillion-dollar pharmaceutical company in history. By late summer, Lilly was valued at roughly four times Novo's market cap - despite producing only modestly higher net income and, at times, lower operating cash flow.

For anyone willing to spend three hours with both companies' financial statements over the last three years, it is genuinely difficult to reconcile that gap. Whatever setbacks Novo endured, and whatever advantages Lilly gained, the financial performance of the two companies - from revenues to margins to balance sheets - does not justify a trillion-dollar company standing across from a two-hundred-billion-dollar one.

This analysis argues that the market has mistaken Novo Nordisk's temporary setbacks for permanent impairment. The move below $50 was driven less by erosion of business fundamentals than by prevailing narrative, market psychology, and price momentum. The question for investors is not which company "wins" a single quarter's headline - it is whether both remain essential to the largest chronic disease market in history. We believe they do. And one of them is dramatically mispriced.

2 Semaglutide: The Drug That Built an Empire - and Then Nearly Destroyed Its Creator's Stock

To understand how a pharmaceutical company growing revenues at 18% per annum, marketing what may be the world's most consequential prescription drug, could lose 65% of its share price in twelve months, we need to start with what semaglutide actually is and what it has actually achieved.

Semaglutide is a GLP-1 receptor agonist approved to treat type 2 diabetes (brand name Ozempic, December 2017) and obesity (brand name Wegovy, June 2021). The drug's ability to achieve 15–20%+ weight loss at various doses was, prior to its arrival, something the scientific community had not believed was pharmacologically possible. Its unique mechanism - stimulating insulin release, reducing glucagon, slowing gastric emptying, and suppressing appetite - proved genuinely groundbreaking.

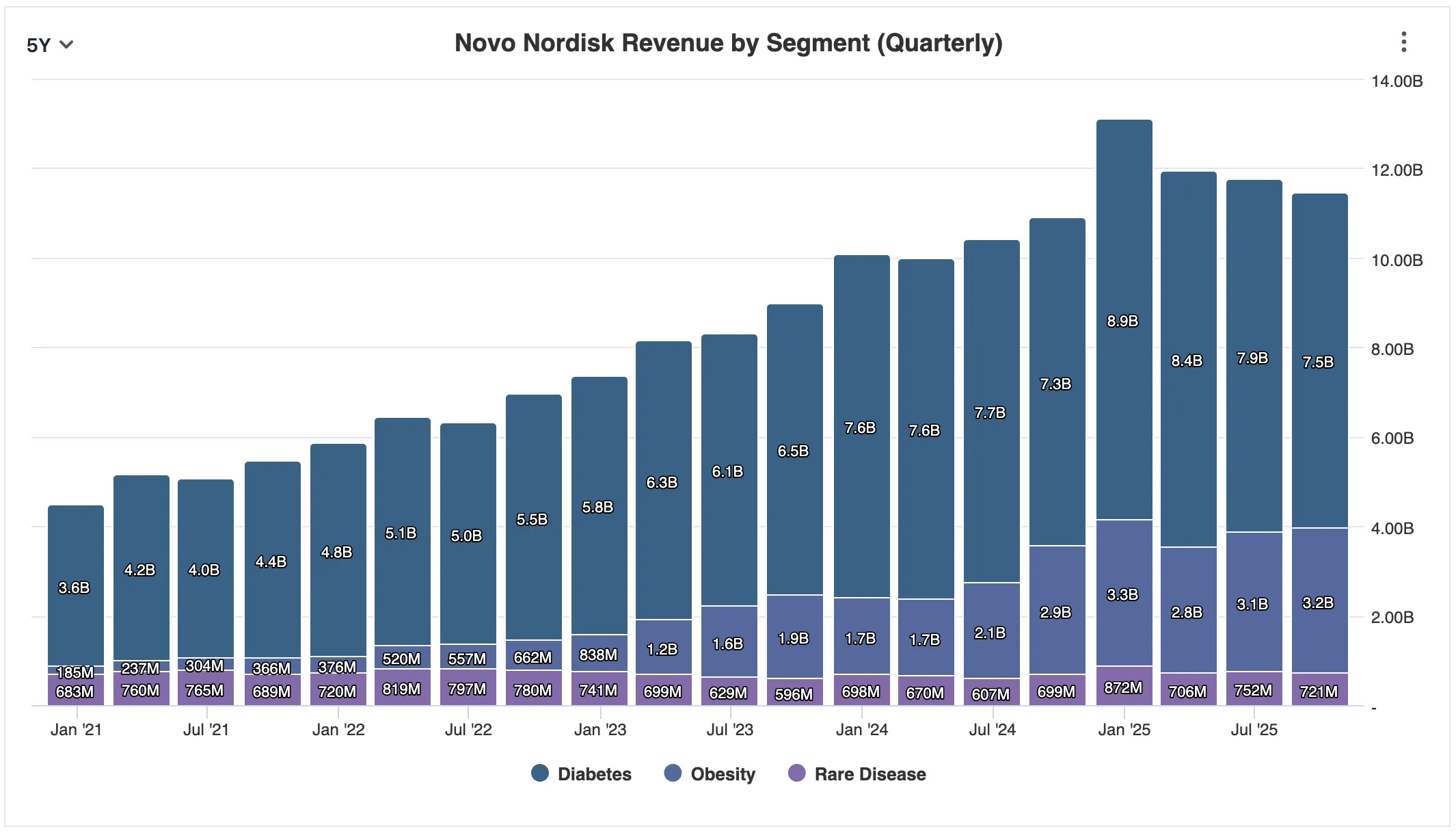

The commercial trajectory has been equally extraordinary. In 2022, Ozempic earned approximately $8.3 billion and Wegovy $860 million. By 2025, based on performance through Q3, Ozempic is on pace for approximately $19.6 billion in annual revenue and Wegovy approximately $11.8 billion - together accounting for roughly 66% of Novo's estimated $48 billion total revenue. Wegovy sales are up 45% year-over-year. Ozempic is up 17%. Analysts estimate semaglutide could achieve close to $60 billion in peak annual revenues by 2031.

Novo Nordisk's revenue is overwhelmingly concentrated in its diabetes and obesity segments, which generated $10.7 billion in Q3 alone - dwarfing the $0.72 billion from rare diseases. The question is not whether this concentration is a strength or a vulnerability. It is both. What matters is whether the market that semaglutide serves is large enough, and growing fast enough, to justify that concentration. The answer, by any reasonable measure, is yes.

So: crisis, what crisis? How does a company with this trajectory lose two-thirds of its market value? The answer lies in a collision of genuine setbacks, narrative momentum, and the structural dynamics of modern equity markets.

The underwhelming Phase III data for CagriSema - Novo's next-generation triple agonist that management had promised would deliver 25%+ weight loss - was one trigger. Trump-era tariff threats against pharmaceutical imports were another. The departure of longstanding CEO Lars Fruergaard Jørgensen in May 2025 added uncertainty. And throughout it all, the relentless advance of Eli Lilly and its tirzepatide molecule (Mounjaro/Zepbound) provided a clear alternative narrative: Lilly was winning, and Novo was finished.

In the modern U.S. equity market, increasingly shaped by retail participation and narrative-driven momentum, valuation spreads between "winners" and "disappointments" do not merely widen. They overshoot in both directions. Eli Lilly became a symbol stock: headlines of explosive growth and uninterrupted upward price action became mutually reinforcing. Capital did not simply reallocate - it crowded. Temporary setbacks began to look permanent. Momentum begat momentum.

3 Novo Is Not a U.S.-Only Story - and the Market Priced It as If It Were

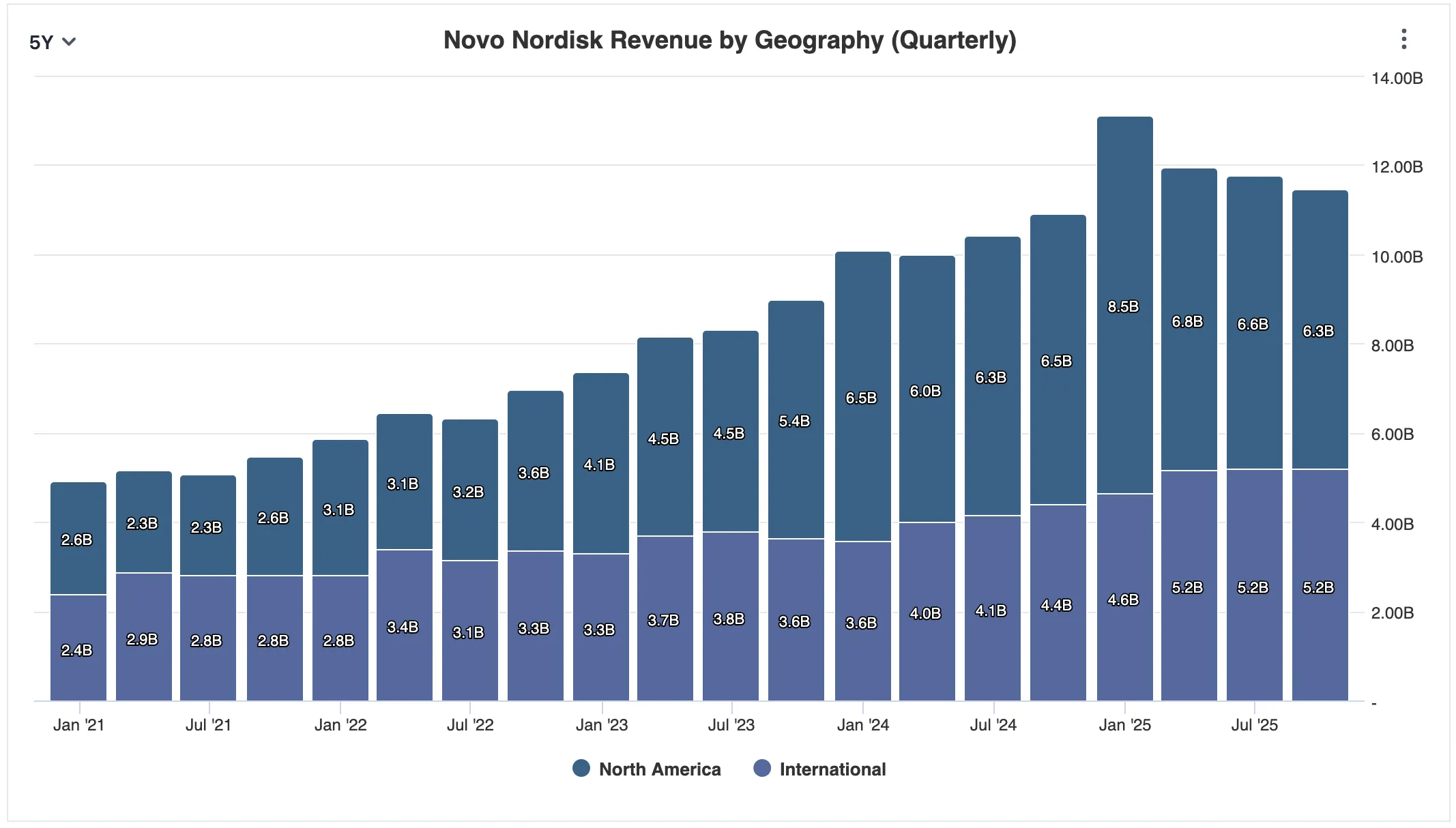

Most of the Novo-versus-Lilly narrative over the last two years has been filtered through a U.S. lens: declining U.S. market share, regulatory challenges from Washington, pricing pressure from compounders exploiting loopholes through platforms like Hims & Hers. That emphasis is understandable. The United States is the most profitable pharmaceutical market in the world.

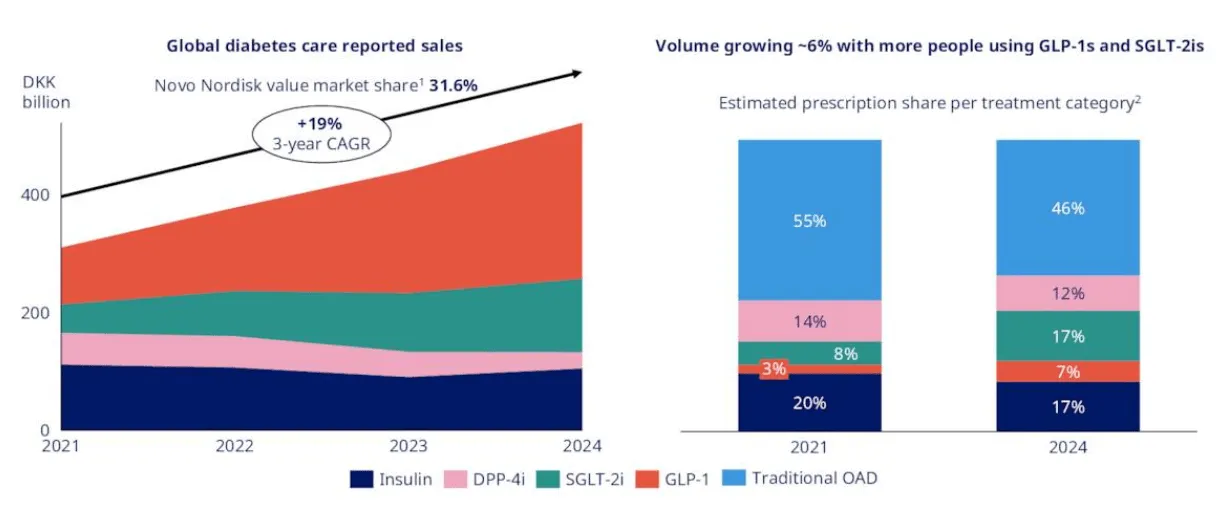

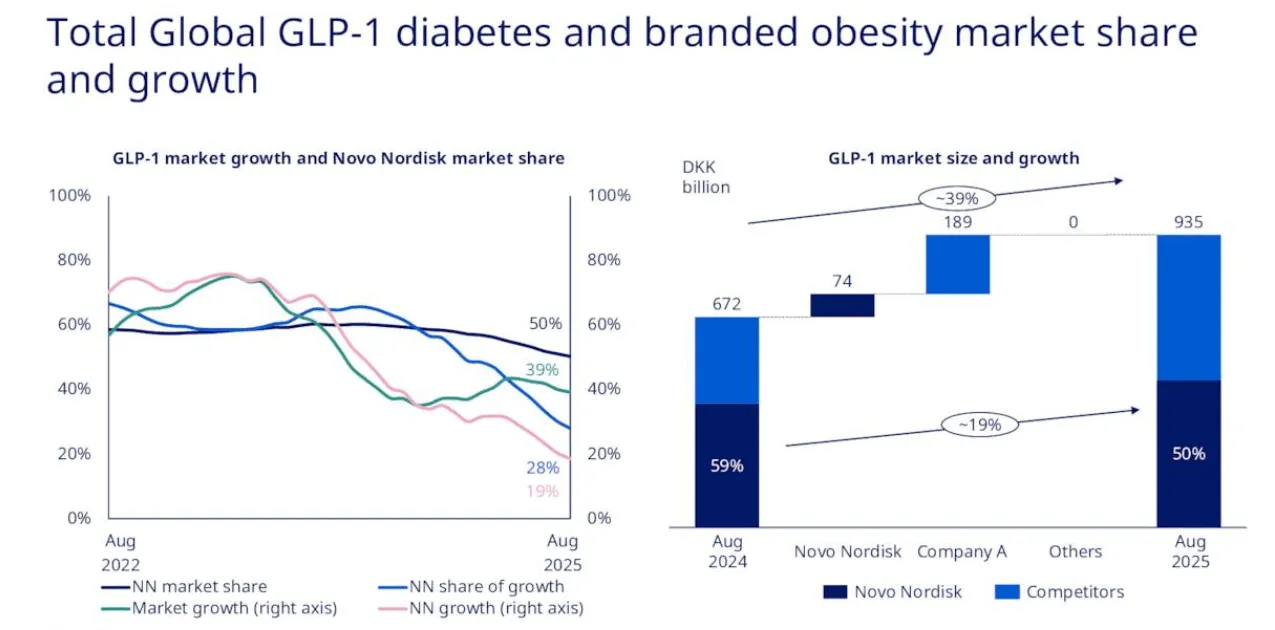

But although the U.S. accounts for roughly half of Novo's revenue - and approximately two-thirds of Lilly's - Novo is arguably the least U.S.-dependent major pharmaceutical company in existence. Long before GLP-1 drugs became headlines, Novo spent decades building dominant insulin and diabetes franchises across Europe, Latin America, the Middle East, and Asia. In many of those markets, Novo is the institutional default - the top name on short lists of long-standing suppliers to public health systems, national formularies, and hospital networks. In its 2024 annual report, the company declared itself "the global market leader in the GLP-1 segment with a 55.1% value market share," as well as "the global market leader with a volume market share of 70.4% of the branded obesity market."

In Q3 alone, international revenue topped $5.2 billion against $6.3 billion from the U.S. In previous years, ex-US revenue was nearly equal to U.S. revenue, however past 2 years, this proportion shifted reflecting the market success of Ozempic and Wegovy. That matters because obesity pharmacotherapy is not spreading only through compounders and social media in the U.S. It is spreading through health systems across the globe. And 95% of the world's population lives outside the United States - where Novo has cultivated relationships for decades.

At the January JPMorgan Healthcare Conference, Novo's new CEO, Maziar Doustdar, emphasized this point repeatedly. He framed Novo not as a U.S.-centric drug company, but as a global metabolic franchise serving a patient population approaching two billion people worldwide. Outside the U.S., prescription penetration remains extremely low. The United States may be in the first inning. Most of the world has not yet come to bat.

However, when investors decided Lilly was "winning" based largely on U.S. data, Novo was punished as if global metabolic markets were either irrelevant or already decided. That view quietly assumed Novo's manufacturing prowess, regulatory expertise across dozens of jurisdictions, and distribution networks built over a hundred years barely mattered. It is hard to sustain that conclusion when you actually look at the numbers.

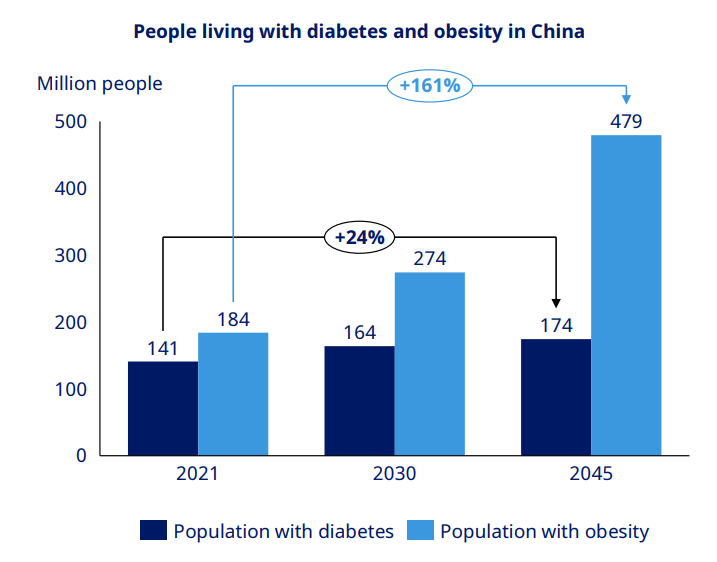

In China, Novo currently estimates a near-80% market share for GLP-1 agonists. TTM revenue from the region was approximately $2.96 billion, representing about 6% of total revenue. Generic competition is intensifying - 15 to 16 Chinese companies are developing semaglutide equivalents, and Novo recently cut injectable Wegovy prices across Chinese provinces by up to 50%. But the market itself is enormous (148 million adults with diabetes, potentially 65% of the population overweight or obese by 2030) and still fundamentally in its infancy. The competitive landscape is as much about growth as it is about defense.

4 The Oral Pill Changes the Competitive Psychology

One of the central arguments against Novo over the past year has been that Lilly was winning the injectable race - that tirzepatide's marginally superior weight loss numbers (20–22% versus semaglutide's 15–17%) represented an enduring competitive advantage. The debate had narrowed to injectable trial percentages, as if obesity pharmacotherapy were a single-dimension sprint.

On December 22, 2025, the FDA approved Novo Nordisk's oral version of Wegovy - the first FDA-approved oral GLP-1 treatment for obesity. The OASIS-4 trial showed that 25 mg of oral semaglutide taken daily reduced weight by 16.6% on average, with one in three patients experiencing 20% or greater weight loss. Oral Wegovy reached over 3,000 patients in its first week on the market, and more than 18,000 prescriptions in the first full week of availability.

This is not merely a new formulation. It is a paradigm shift. Injectables primarily capture highly motivated, insured, and medically engaged patients. A pill opens the door to the mass market. There are billions of overweight or obese individuals worldwide who will never self-inject unless a physician urges them to. Oral therapy normalizes weight-loss treatment. It shifts obesity management closer to statins and antihypertensives - routine medication, free from stigma.

OASIS-4 Weight Loss

Pivotal Trial Weight Loss

There is also the practical matter of refrigeration. Injectable Wegovy and Zepbound require cold-chain storage. A pill does not. For patients who travel, who live in rural areas, or who simply find the logistics of weekly injections burdensome, this is a material improvement in quality of life - and a significant reduction in barriers to adherence.

At the JPMorgan conference, CEO Doustdar drove this home with characteristic directness: his father-in-law had been wanting a GLP-1 treatment but refused to inject. A friend in Montana wanted to switch from Lilly's injectable because he was "simply too nervous about keeping the medication in cold chain" while traveling. These are not edge cases. They represent the vast middle of the addressable market that injectables alone cannot reach.

Eli Lilly's oral candidate, orforglipron, has had its FDA decision pushed back to April 10th. Its pivotal data showed mean weight loss of 7.9% - a respectable result, but roughly half of oral Wegovy's 16.6%. Lilly's tolerability profile is also weaker: in clinical trials, approximately 22–24% of patients at the highest orforglipron dose discontinued due to adverse events, compared with just 7% for oral Wegovy.

The Dosing Controversy: What Lilly's Head-to-Head Trial Actually Shows

In September, Eli Lilly published a head-to-head trial comparing oral semaglutide (7 mg and 14 mg) with orforglipron (12 mg and 36 mg). On the surface, orforglipron appeared to outperform on both blood sugar control and weight loss. But these results obscure a critical fact: the semaglutide doses Lilly chose (7 mg and 14 mg) were significantly lower than the 25 mg dose Novo used in its pivotal OASIS-4 trial.

This is the equivalent of testing England's reserve squad against Spain's first team and declaring Spain superior. Why did Lilly not trial orforglipron against the 25 mg dose that Novo has used since 2023? The company cited "approved label instructions," but earlier Lancet-published studies had already established 25 mg and 50 mg as the clinically relevant doses. As Novo's CEO put it with pointed understatement at JPMorgan: "The world, in my opinion, has a little bit misread this."

The ATTAIN-MAINTAIN trial, published in early January, added further concern: patients switching from Zepbound to orforglipron gained back 5 kg - approximately 20% of original weight lost - compared with just 0.9 kg for those switching from Wegovy. Discontinuation rates were also higher (7.2% vs 4.8%). This data suggests orforglipron may be an inferior product to the injectable it is meant to replace.

5 Airbus vs. Boeing: The Right Framework for This Rivalry

The Novo-Lilly rivalry has often been framed as if it were a single fateful duel - one company will win, the other will lose. That framing is wrong. Properly understood, this is a duopoly that will play out over decades, not quarters.

A better analogy is the rivalry between Airbus and Boeing. Over time, each has suffered execution crises, regulatory setbacks, and public embarrassment. Each has won some cycles and lost others. Neither disappeared. The structure of global commercial aviation does not permit a single supplier. No airline, no government, and no regulator will entrust their entire fleet to one manufacturer.

Cardiometabolic medicine is no different. No government, insurer, or health system will entrust its obesity and diabetes care needs to one company. Pricing leverage, supply chain risk, and geopolitical considerations all conspire to guarantee an enduring multi-supplier environment. The investment question, therefore, is not who captures the next headline. It is whether both remain essential - and which, at present, offers the more attractive entry point.

Buying Boeing stock below $150 during its 737 MAX crisis did not require believing Boeing would dominate Airbus. It required believing Boeing would remain indispensable - and solvent. That was enough. Similarly, the case for Novo below $50 did not require believing Novo would defeat Lilly. It required believing Novo would, in the foreseeable future, remain one of the two foundational suppliers to one of the largest chronic disease markets in history. Solvency has never been in doubt.

Where the Analogy Breaks: Generics and Patent Cliffs

There is one critical difference. No one has ever seen a generic Boeing 747. But the world will soon see generic GLP-1 drugs. Dr. Reddy's has already won Indian approval for a generic Ozempic. Fifteen Chinese companies are developing semaglutide equivalents. Patent cliffs are the inescapable long-term risk for both Novo and Lilly, and they mean the duopoly probably will not last as long as the one between Boeing and Airbus. This is why valuation discipline matters - and why Novo's current discount to Lilly is significant.

6 The New CEO: A Commercial Operator With Something to Prove

In August 2025, Novo appointed Maziar "Mike" Doustdar as CEO. He is a company lifer who joined in 1992 as an office clerk in Vienna and rose through the ranks to oversee Novo's entire international business. Under his watch, international operations grew into a franchise generating well over $15 billion annually.

His JPMorgan Healthcare Conference fireside chat in January may prove to be the most consequential interview given by any pharmaceutical CEO in 2026. Three things stood out:

First, he narrowed the focus. Where previous management had chased adjacencies and over-promised on CagriSema, Doustdar was explicit: Novo's core is diabetes and obesity, and that core serves two billion people with enormous unmet need. As he told the audience: "Those couple of things have 2 billion people suffering from those conditions. We are only touching the surface when it comes to treatment of these individuals." The implication was clear: stop worrying about what Novo doesn't do, and focus on what it does better than anyone else.

Second, he admitted mistakes. CEOs at large companies rarely do this. Doustdar was candid about Novo's failure to understand the U.S. insurance landscape, about the gap between theoretical coverage (55 million insured patients) and the reality of pre-authorizations and access barriers. He acknowledged the company needed to meet patients where they are, announcing partnerships with Ro, LifeMD, Amazon, WeightWatchers, and Costco to build direct-to-consumer channels. "Us and Lilly combined have probably 10 million, 15 million patients. What about the other 85 million? We need to get to them."

Third, he took the fight directly to Lilly. On tolerability: "Some 7% of our trial participants left due to tolerability issues. When you look at my competitors, it was around 22% to 24% at the highest dose." On dosing strategy: "Our company is a bit conservative when it comes to these things… when you are second to market and you're designing your trials, you tell yourself, I've got to go all the way up to 15 milligrams to get there." The subtext was unmistakable: Lilly achieved its headline weight-loss numbers by pushing dosing higher, while Novo took a more conservative approach and still delivered a superior oral product.

The Leadership Risk

Doustdar is widely regarded as a capable commercial operator. But his training is in international business, not science. Drug companies are not consumer goods companies - they are long-cycle research organizations whose most consequential decisions involve allocation of capital across uncertain clinical programs. A CEO with relevant scientific background conveys a long-term advantage to Big Pharma. This does not disqualify Doustdar - many successful pharma CEOs were not scientists - but it places greater weight on the strength and independence of Novo's R&D leadership to make the right strategic decisions. The board will need to ensure the science does not become subordinate to the commercial instinct.

7 Manufacturing: The Race Within the Race

Drug efficacy matters, but in 2025–2026, the winner may ultimately be determined by whoever can produce the most doses. Both companies are engaged in the largest manufacturing buildout in pharmaceutical history - collectively committing over $43 billion in capital expenditure.

Novo Nordisk - $25B+ CapEx

- Kalundborg 2.0 (Denmark) - $6.5B, 2.5x current output, phased 2024–2027

- Chartres (France) - $2.9B, fill-finish +150%, Q3 2026

- Clayton (North Carolina) - $4.1B, US production base, 2026–2029

- Odense (Denmark) - $1.8B, oral semaglutide focus, late 2025

- Montes Claros (Brazil) - $320M, Latin America supply, Q2 2026

Capacity increase: 3–4x by 2027

Eli Lilly - $18B+ CapEx

- Lebanon Gigafactory (Indiana) - $3.7B, injectable biologics, 2025–2028

- LEAP Innovation (Indiana) - $4.5B, modular pods, 2026–2030

- Concord (North Carolina) - $800M, oral GLP-1, Q4 2025

- Limerick (Ireland) - $1.8B, Europe API, 2026–2027

- Alzey Acquisition (Germany) - $2.7B, instant capacity, 2025

Capacity increase: 5–6x by 2027

Lilly arguably has the lead in terms of capacity growth rate, driven by its modular LEAP facility design and the instant capacity provided by the Boehringer Ingelheim acquisition. However, in a post-tariff world, Lilly's concentration of $27 billion in U.S.-based manufacturing could prove costly if international trade dynamics shift. Novo's more globally distributed footprint - Denmark, France, Brazil - provides geographic diversification that may prove strategically valuable. And Novo's Odense expansion specifically targets oral semaglutide manufacturing, giving it an uncontested supply advantage in a product category where Lilly has no approved offering.

8 The Numbers That Matter: Why Novo Looks Mispriced

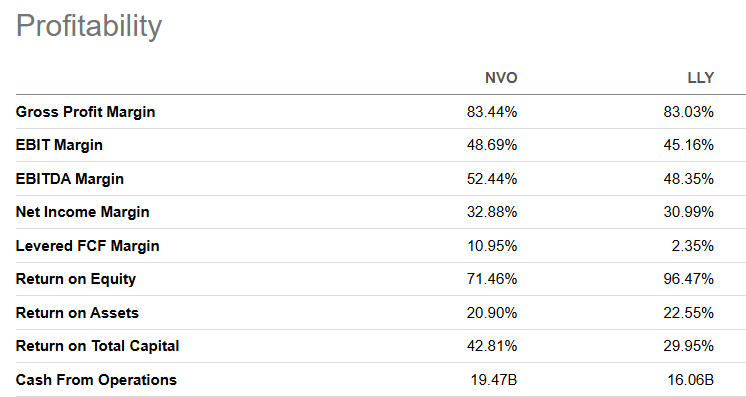

Novo Nordisk holds cash and equivalents of $5.02 billion, current assets worth $28.03 billion, and total assets valued at $78.94 billion. Total debt stands at $15.59 billion, of which only $1.85 billion is due within the next 12 months - easily covered by quarterly free cash flow of $5.0 billion and $10.17 billion over the trailing twelve months. The debt-to-equity ratio of 0.6 represents a comfortable burden. The company rewards shareholders through dividends and buybacks, with a total shareholder yield of 3.75%.

Profitability: NVO vs LLY

What makes the valuation gap so puzzling is that Novo is not merely competitive with Lilly on profitability - it is superior on most metrics:

| Metric | NVO | LLY |

|---|---|---|

| Gross Profit Margin | 83.44% | 83.03% |

| EBIT Margin | 48.69% | 45.16% |

| EBITDA Margin | 52.44% | 48.35% |

| Net Income Margin | 32.88% | 30.99% |

| Levered FCF Margin | 10.95% | 2.35% |

| Return on Equity | 71.46% | 96.47% |

| Return on Assets | 20.90% | 22.55% |

| Return on Total Capital | 42.81% | 29.95% |

| Cash From Operations | $19.47B | $16.06B |

The Valuation Disconnect

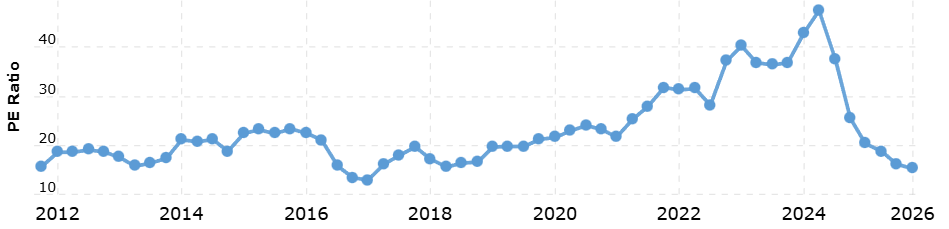

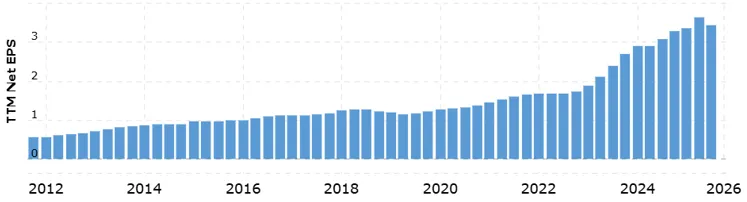

And yet Novo trades at approximately 17x earnings while Lilly trades at approximately 51x. On a price-to-sales basis, Novo is at roughly 5.6x versus Lilly's 16x. Novo's stock is at its lowest P/E ratio in seven to eight years - one of the lowest in its history. Is this a value trap?

Given consistently rising EPS over the last fourteen years - with recent acceleration driven by the GLP-1 franchise - a value trap looks extremely unlikely. The earnings trajectory has not broken. What broke was sentiment.

Yes, Lilly has a wider and more diverse product range - its Alzheimer's drug Kisunla adds meaningful revenue diversification. But make no mistake: Lilly's 400%+ share price gains over five years have been driven almost exclusively by tirzepatide, a drug that is far more similar to semaglutide than it is differentiated. For the market to assign a 3x valuation premium to one company over the other, when both are powered by the same drug class, serving the same patient population, with comparable profitability - that requires an extraordinary level of conviction that one company will permanently dominate and the other will permanently decline. The evidence does not support that conviction.

9 Catalysts, Risks, and What Could Go Wrong

Key Risks for Both Companies

Short-term: Novo's stock has already partially priced in the oral Wegovy approval and strong early commercial performance. Any disappointment in rollout pace or Q4 earnings could send shares back down. Lilly's orforglipron delay to April creates an overhang; weaker-than-expected data would be punished severely at current valuations.

Intermediate-term: Pricing pressure is inevitable. Both companies have agreed to drop U.S. prices from ~$1,300/month to ~$350 via the Trump Administration's pricing deals. Manufacturing capacities may strain. Competition will intensify - Amgen, Roche, Viking Therapeutics, and multiple Chinese companies are all pursuing GLP-1 opportunities, and at least some of them will succeed.

Long-term: Patent cliffs are the inescapable risk for both. Blockbuster GLP-1 drugs will inevitably face generic competition. Dr. Reddy's has already won Indian approval for generic Ozempic. This is not a theoretical future risk - it is an imminent and material one.

Emerging Challengers Worth Monitoring

Amgen (Maritide): Monthly dosing GLP-1/GIP dual agonist. 14.5% weight loss at 12 weeks in Phase 2. Potential 2027 approval. Viking Therapeutics (VK2735): 15.7% weight loss at 13 weeks. More likely an acquisition target than independent competitor. Pfizer (Danuglipron): Discontinued October 2025 due to 40%+ adverse event dropouts - a reminder that oral GLP-1 development is genuinely difficult, which makes Novo's oral Wegovy achievement more impressive.

Despite these challengers, the duopoly is likely to hold 80%+ combined market share through at least 2028. New entrants lack the 4–7 years needed to build GLP-1 manufacturing at scale, and comprehensive patent estates provide protection through the early 2030s.

10 Conclusion: Two Companies, Two Prices, One Market

Here is what we know. Novo Nordisk, a 103-year-old company that essentially created the global market for metabolic disease treatment, is trading at a valuation that implies its best days are behind it. Eli Lilly, a company whose recent success has been driven almost entirely by a single drug class that Novo pioneered, is trading at a valuation that implies perfection for the next decade.

The clinical data does not support the narrative that Lilly has permanently won the GLP-1 race. Oral Wegovy appears to be the superior oral product by a significant margin. The ATTAIN-MAINTAIN data raises legitimate questions about orforglipron's ability to retain patients switching from Zepbound. Novo's global infrastructure, particularly outside the United States, provides growth levers that U.S.-focused analysts are systematically underweighting.

This is not a recommendation to sell Lilly and buy Novo. Lilly remains a formidable company with a diversified pipeline, faster-growing manufacturing capacity, and strong U.S. execution. What this analysis suggests is that the market has mispriced the relative positioning of the two companies - that the narrative has oversimplified a complex rivalry into a simple "Lilly wins" story.

"Luckily, in the obesity space, it is not the case that you must buy Novo and sell Lilly, or sell Novo and buy Lilly. You can own both, and they may even be good for one another, as Pepsi's rivalry with Coke is arguably good for both companies. Under its new CEO, Novo is taking the fight to Lilly in a way it was unable to do last year. The world, in our opinion, has a little bit misread how to value Novo Nordisk's business - but we expect this to change in 2026."

- PolyMarkets Investment Strategies, Research TeamThe central argument of this analysis is specific and falsifiable: the market is pricing Novo as if it were a structurally impaired business - implying near-zero long-term growth in a reverse-DCF framework - while pricing Lilly as if tirzepatide's current U.S. dominance is permanent and uncontested. A 17x-versus-51x earnings gap between two companies generating comparable margins, in the same drug class, serving the same global patient population, is not a measured judgment about competitive positioning. It is an overreaction. Duopolies do not require one competitor to collapse for the other to thrive. Airbus did not need Boeing to disappear. Pepsi does not need Coke to go bankrupt. The convergence trade here is not about Novo "winning" - it is about the market recognizing that it does not need to.

The Boeing/Airbus analogy, however, breaks at a critical point - and understanding where it breaks clarifies the actual risk. Boeing's manufacturing crises were reputational and regulatory. Novo's is purely operational: it cannot yet produce enough doses to satisfy global demand. These are different risk categories. A moat problem - where a competitor's drug is genuinely superior across all dimensions - would be structural and slow to reverse. A manufacturing problem, by contrast, has a known resolution mechanism: capital expenditure, time, and execution. Novo has committed the capital. The risk is execution and timeline, not competitive obsolescence.

The thesis weakens materially under two conditions. First, if semaglutide loses U.S. formulary position faster than current trends suggest - driven by Lilly's aggressive PBM contracting or orforglipron's commercial launch outperforming expectations. Second, if Lilly's SURPASS-CVOT data demonstrates tirzepatide superiority in cardiovascular outcomes, extending its clinical edge beyond obesity and into cardiology, where Novo's SELECT trial data currently gives it the stronger evidence base. Either development would shift the duopoly calculus away from relative parity.

The leading indicators to monitor are narrow: Novo's quarterly manufacturing capacity additions against its own stated targets, and U.S. formulary access negotiations for 2026 - specifically whether oral Wegovy secures preferred tier placement against orforglipron. If capacity scales on schedule and formulary position holds, the valuation gap has no durable justification.

Investment Disclaimer

This article is for educational and analytical purposes only and does not constitute financial or medical advice. Pharmaceutical investments carry significant risks including clinical trial failures, regulatory delays, patent challenges, and manufacturing setbacks. GLP-1 drugs have known side effects and long-term safety data is still being collected.

Market projections are estimates based on consensus data and may differ materially from actual results. Medicare coverage, competitive dynamics, and pricing pressures could significantly impact forecasts. Consider consulting a financial advisor before making investment decisions based on this analysis.

PolyMarkets Investment Strategies, Market Research, January 23, 2026