There is a moment in every commodity cycle when the destruction of value becomes so complete, so thorough, and so emotionally exhausting that the last remaining investor either gives up or quietly doubles down. Lithium in August 2024 is at exactly that moment. The metal that was trading at over $80,000 per metric ton in late 2022 - when every EV startup needed priority supply and every OEM signed long-term contracts in a panic - is now scraping $10,000 per metric ton. An 87% collapse in less than two years.

The company sitting at the epicenter of this collapse is Sociedad Química y Minera de Chile S.A. - known simply as SQM - a Chilean mining and chemical group that controls the world's most productive lithium brine operation in the Salar de Atacama. Its stock, which peaked near $110 in mid-2022, trades today around $37. The market has already priced in a great deal of permanent damage.

What the market has not priced in is this: SQM produces lithium at a cash cost of approximately $5,000 per metric ton - less than any other meaningful producer on the planet. At $10,000 spot, the company still makes money. Its Q2 2024 results show a 16.5% net margin, $213 million in net income for a single quarter, and record lithium sales volumes of 52,000 metric tons - even in the worst pricing environment in a decade. Meanwhile, the company just signed a partnership agreement with state miner Codelco that locks in its rights to operate the Salar de Atacama until 2060. The license risk - the single biggest long-term uncertainty overhanging this stock for years - has been resolved.

Lithium prices will not stay at $10,000 per metric ton. The math is simple: most new projects globally are unprofitable at these levels. Higher-cost capacity is being shut down. SQM is taking the opposite approach - holding production steady and gaining market share while peers retreat. When demand from the secular EV transition catches up to today's oversupply, SQM will be positioned better than it has ever been. The entry zone of $36–$38 is not a trade on tomorrow's lithium price. It is a position on where the world will be in 12 to 18 months.

SQM at a Glance

Sociedad Química y Minera de Chile S.A. is one of the world's largest producers of lithium, iodine, potassium nitrate, and specialty plant nutrients. Its flagship operation is the Salar de Atacama in northern Chile - the world's most productive lithium brine deposit, sitting at over 4,500 meters of altitude in the driest desert on earth. Unlike hard-rock lithium mining, which involves crushing spodumene ore and intensive chemical processing, SQM's brine operation uses the desert sun to evaporate naturally occurring lithium-rich saltwater into progressively concentrated pools - a vastly simpler and cheaper process. That geological accident is the source of SQM's structural cost advantage and its dominant position in the global supply chain.

SQM is not a pure-play lithium miner. Its iodine business - where Chile commands over 60% of global supply - has been delivering double-digit revenue growth in 2024, driven by demand from X-ray contrast media and LCD manufacturing. Its potassium nitrate segment for specialty agriculture is quietly resilient. These businesses provide a critical revenue floor when lithium prices are suppressed. In the second quarter of 2024, iodine revenues rose 22% year-over-year. That is not what a company in crisis looks like.

The Anatomy of the Collapse

To understand why SQM is interesting at $37, you need to understand why lithium did what it did - because the story of the 2022–2024 collapse is a textbook commodity cycle, not a structural technology problem.

It began with genuine, extraordinary demand. Electric vehicle sales accelerated sharply through 2021 and 2022, driven by government incentives, falling battery costs, and a surge in post-pandemic consumer spending. Lithium carbonate spot prices - sitting at roughly $7,000 per metric ton in early 2021 - hit over $80,000 per metric ton by November 2022. A tenfold increase in under two years.

At those prices, every lithium project that was economically marginal suddenly looked like a gold mine. Miners everywhere - in Chile, Argentina, Australia, China - rushed capital into capacity expansion. Meanwhile, EV growth rates, which had been extraordinary, began to normalize. Europe's EV sales slipped as government incentives were reduced in Germany and France. US growth slowed to a 7% quarterly rate in early 2024. China continued to grow strongly, but not fast enough to absorb the incoming supply wave.

The result was a spectacular oversupply. Prices that peaked above $80,000 declined to roughly $10,000 by mid-2024 - a 87% collapse. The narrative shifted from "lithium shortage crisis" to "lithium glut." Company revenues cratered. SQM's revenue fell 37% year-over-year in Q2 2024. Albemarle announced plans to shut half its Australian processing capacity. The pendulum had swung all the way to the other extreme.

"The cure for low prices is low prices."

- Classic commodity market principle, observed in oil, copper, coal - and now lithiumThis is the pattern. High prices attract excessive investment. Oversupply drives prices down. Low prices make new investment uneconomical and force existing capacity offline. Demand, still growing on the secular EV trend, eventually catches up to reduced supply. Prices recover. The cycle resets. It happened in oil in 2015–2016. It happened in iron ore. It will happen in lithium - the only question is the timing.

What makes SQM particularly compelling in this moment is precisely what makes commodity cycle investing difficult: you are buying maximum pessimism. The market is pricing SQM as though the oversupply is permanent, EV growth has peaked structurally, and the lithium cycle will not recover. Every one of those assumptions deserves serious scrutiny.

Profit at the Trough - Reading the Numbers

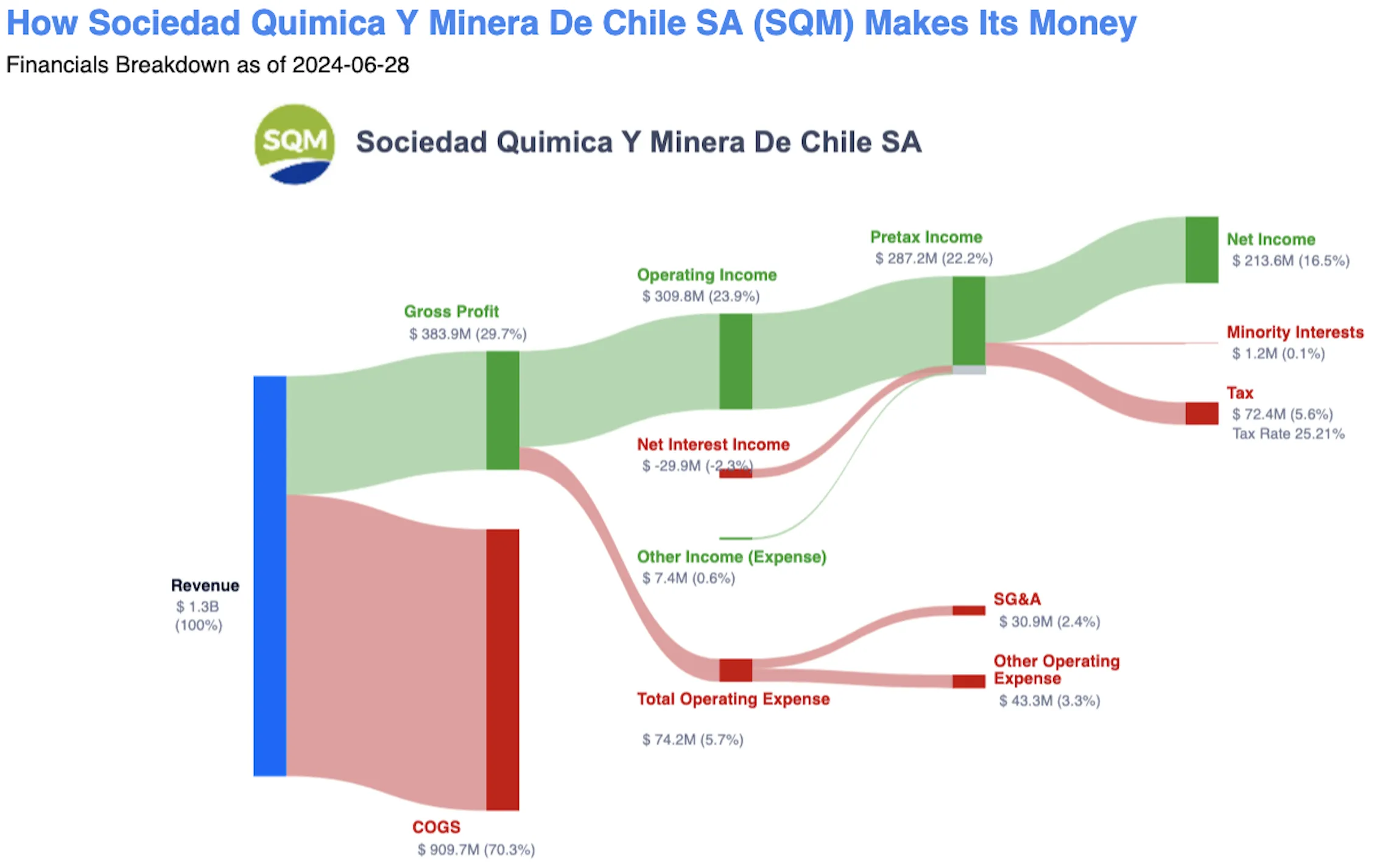

The most revealing thing about SQM right now is not that it is struggling. It is how little it is struggling at these conditions. The Q2 2024 profit flow diagram tells that story precisely.

At first glance, the picture appears stressed: COGS consumes 70.3% of revenue ($908.7M), a significantly elevated ratio compared to the boom-era margins SQM enjoyed when lithium was at $50,000+ per metric ton. But read the numbers more carefully and a different story emerges.

Even after that elevated cost ratio - which directly reflects the compressed lithium price environment - SQM generates gross profit of $383.9M, an operating income of $309.8M (23.9% margin), and ultimately net income of $213.6M at a 16.5% net margin. This is not a company bleeding cash. This is a company running profitably at the bottom of its worst pricing cycle in a decade.

The tax line ($72.4M, 25.21% rate) is now normalized following the one-time $1.1 billion accounting adjustment in Q1 2024 related to the Chilean lithium mining tax from prior years. That Q1 distortion - which had no significant cash impact (most of it was already paid in previous years) - caused an alarming headline net loss of $870 million. That overhang is gone. Q2 demonstrates what SQM's ongoing earnings power looks like: approximately $200M+ per quarter in net income at trough lithium pricing.

Now ask yourself: if SQM earns $213M in a single quarter when lithium is at $10,000 per metric ton and COGS is running at 70% of revenue, what do those numbers look like when lithium recovers to $20,000? The Sankey diagram shows you the mechanical leverage: the cost base is largely fixed - brine evaporation is solar-powered and the Atacama doesn't charge rent. Revenue dollars above $10,000 per ton flow through at dramatically higher margins. A doubling of the lithium price could more than triple SQM's earnings per share.

The Atacama Moat - Cost Advantage & Market Position

Not all lithium is created equal. The global lithium supply chain runs from world-class brine deposits in South America's lithium triangle to hard-rock spodumene mines in Western Australia to direct lithium extraction projects that remain largely experimental. SQM's position at the top of the Atacama brine system is, from a cost standpoint, essentially unassailable. No competitor produces lithium as cheaply.

| Producer | Primary Source | Cash Cost ($/MT LCE, est.) | Cost Position | Response to Low Prices |

|---|---|---|---|---|

| SQM | Atacama brine (Chile) | ~$5,000 | Lowest | Holding / gaining share |

| Albemarle (ALB) | Mixed brine + hard rock | ~$8,000–$10,000 | Mid | Cutting capacity (Australia) |

| Ganfeng Lithium | Mixed global sources | ~$9,000–$12,000 | Higher | Project delays |

| Australian spodumene (avg.) | Hard rock mining | ~$15,000–$20,000 | High | Uneconomical at spot; curtailing |

The strategic calculus here is important. Management was direct on the Q2 earnings call: SQM does not intend to cut production. In fact, the company produced 210,000 MT of lithium carbonate equivalent in 2024 guidance while selling around 190,000 MT - intentionally building inventory in anticipation of stronger demand. This is not recklessness. It is the classic low-cost producer strategy: outlast the competition, gain market share while peers retreat, and be positioned when prices recover.

Consider what Albemarle is doing. The company announced plans to "shut half its processing capacity in Australia and put an expansion there on hold." Albemarle is not doing this because it wants to - it is doing it because it has to. At $10,000/MT lithium, higher-cost operations are unprofitable or near-breakeven. SQM, by contrast, is still generating double-digit margins and choosing to stay in the game aggressively. When this cycle turns, SQM will have a larger piece of a recovering market.

"We are very clear that the price will be different in the future. That's why we have a clear plan of investment in lithium. We are really committed to that. And we are a very low-cost producer. That's why we will continue to do our investment."

- Mark Fones, CEO of SQM International Lithium, Q2 2024 Earnings CallBeyond lithium, SQM's other businesses are quietly delivering. Iodine revenues rose 22% year-over-year in Q2 2024, with management guiding for record iodine sales volumes exceeding 14,500 MT in 2024 - a 7% growth year driven by X-ray contrast media and LCD/LED screen applications. Potassium revenues rose 10%. These segments act as a financial buffer and are rarely discussed in the lithium-obsessed narratives that dominate coverage of SQM.

The Codelco Equation

For years, the single most persistent overhang on SQM's stock was not lithium prices - it was the question of what would happen in 2030, when SQM's existing lease agreement with CORFO (Chile's state development agency) for the Salar de Atacama was due to expire. Would Chile nationalize the asset? Would SQM be forced into unfavorable terms? Would production continuity be guaranteed?

In June 2024, that uncertainty ended. SQM and Codelco - Chile's state copper mining giant - signed a formal partnership agreement establishing a joint venture to operate the Salar de Atacama from 2025 through 2060. The terms are complex, but the headline is simple: SQM gets 35 more years of certainty in the world's best lithium deposit.

What the Market Fears

- Chile will effectively nationalize SQM's lithium operations

- State (Codelco) takes majority control - diluting SQM shareholders

- 85% of operating margin flows to the Chilean state from 2031

- Codelco becomes general manager in 2031 - execution risk

- Indigenous consultation process could delay or derail the deal

- Additional conditions precedent may not be met by H1 2025

What the Deal Actually Means

- SQM retains full operational management and commercial control through 2030

- JV structure lets SQM consolidate joint venture results on its balance sheet

- License risk completely removed - operations now secured to 2060

- Production target set at 300,000 LCE additional capacity 2025–2030

- New production uses technology to trend toward water balance - ESG benefit

- The ~50,000 MT/yr legacy quota at 6.8% fixed royalty rate now active from 2024 - a meaningful cost advantage vs new production

The state receiving 85% of the operating margin post-2031 sounds alarming in isolation. But it is worth contextualizing: that 85% applies to the margin of the joint venture's new production capacity. SQM still participates in that margin via its consolidated share, and the structure rewards the company for growing production. The alternative - having no license to operate the Salar after 2030 - was a far worse outcome that is now off the table entirely.

One important analytical gap warrants disclosure: the specific equity split between SQM and Codelco in the JV governing new Atacama production has not been publicly confirmed in final form as of August 2024. This matters because SQM's percentage ownership of the JV determines its actual economic interest in the remaining 15% of JV operating margin - and therefore the true impact on SQM's consolidated financials. Investors should monitor official announcements of the final JV structure and update their financial models accordingly. The thesis remains intact as long as SQM's consolidated economics reflect meaningful participation in Atacama production economics beyond 2030 - but the precise ownership split is a variable that, once confirmed, may require adjusting the valuation framework.

Ricardo Ramos, SQM's CEO, called the Codelco agreement "a pivotal moment for both SQM and for the future of the lithium industry in Chile." The partnership is not without its complications - conditions precedent, regulatory approvals, community consultations - but the trajectory is clear. SQM trades today as though this agreement either doesn't exist or doesn't matter. At $37, investors are getting the resolution to the company's greatest long-term uncertainty essentially for free.

Catalysts - What Drives the Recovery

Understanding the thesis is different from understanding the timing. SQM is a sound long-term position. But for the stock to move from $37 toward $64–$74, specific catalysts need to materialize. Here is how the pathway looks from this vantage point in August 2024.

Technical Picture - Reading the Chart

The technicals tell the same story as the fundamentals: maximum pessimism, compressed into a zone that historically marks cycle lows in quality commodity names.

The weekly chart is unambiguous in its narrative. SQM peaked near $110 in mid-2022 - almost exactly when lithium carbonate spot prices reached their all-time highs. What followed was a relentless, 26-month decline that erased nearly 66% of the stock's value by August 2024. No meaningful recovery attempts held. Each bounce was sold into.

As of the week of August 19, 2024, the key technical read is:

- Price action: Open $37.26, High $38.64, Low $36.48 - the daily range sits precisely within our entry zone of $36–$38, a striking alignment between the technical structure and the fundamental valuation floor.

- Bollinger Bands (20,2): Lower band at $34.35. The stock is trading near the lower band but not yet beyond it, suggesting compression rather than capitulatory blow-off. Historically in commodity stocks, prices do not sustain below the lower Bollinger for more than a few weeks before mean-reverting.

- Moving averages: MA(20) at $42.73, MA(50) at $47.57, MA(100) at $63.82, MA(200) at $63.92. Every major moving average sits above the current price. The stock is extended to the downside relative to all key averages. The MA(200) at $63.92 is notable - it effectively coincides with the lower end of our $64-$74 target zone. Long-term mean reversion toward the MA(200) alone would represent a 73% recovery from entry, establishing the floor of what we consider a conservative target range.

- Horizontal major support: A significant support zone exists at $49.45 - visible as a prior consolidation area. Breaking back above this level on the recovery would be the first signal that a genuine trend reversal is underway.

- Volume: Elevated volume in August 2024, consistent with distribution exhaustion or early capitulation - the kind of volume profile that often precedes bottoms in fundamentally sound names.

The technical picture is not a "buy signal" in the traditional sense - there is no moving average crossover or trend reversal confirmed at this point. What it does show is that the stock is deeply oversold by every medium and long-term measure, and is sitting at the lower end of an extreme compression zone. For a position with an 18-month horizon, these are the conditions under which commodity cyclicals historically offer their best entries.

Recovery Math - Three Scenarios

The core variable driving SQM's earnings - and therefore its valuation - is the lithium price. The following scenarios model what the stock could be worth in 12–18 months under three distinct price recovery paths, based on analyst EPS consensus and historical EBITDA multiple ranges.

◆ Bear Case

EV slowdown extends through 2025. Chinese producers resist curtailment. Lithium prices remain stuck at $8K–$12K/MT. SQM's 2025 EPS lands around $2.50–$3.50. The stock drifts lower toward Bollinger support ($34), potentially breaking below $30 if sentiment worsens further. Long-term thesis intact but recovery delayed 2+ years. New project delays eventually force supply discipline.

◆ Base Case

Capacity cuts from Albemarle and others reduce supply additions through H2 2024. China's EV market continues growing and energy storage demand accelerates. Lithium prices stabilize then recover to $15K–$20K/MT by mid-2025. SQM's 2025 EPS recovers toward $5–$6. At 10–11× earnings - the historical norm - the stock re-rates toward $55–$65. Codelco JV conditions completed, removing license risk premium entirely.

◆ Bull Case

Supply curtailment accelerates faster than expected. China's EV and energy storage demand surprises to the upside - China has already been driving EV penetration to record highs in 2024. Lithium prices recover to $22K–$30K/MT by late 2025. SQM's 2025 EPS exceeds $7–$8. Coupled with a valuation re-rating toward 10× forward EBITDA and the resolution of Codelco uncertainty, the stock moves toward $68–$74. Mt. Holland first production and continued record lithium volumes add further upside optionality.

Wall Street's current consensus price target of $57.33 - representing a 54% upside from the $37 entry - is consistent with the base case. Several analysts have intrinsic value estimates closer to $61 (Simply Wall St DCF model). Our target zone of $64–$74 represents a bull-to-upper-base-case outcome, reflecting recovery toward the 200-week moving average, which also sits at $63–$64. That is not an aggressive target for a company with 20% global lithium market share, the world's lowest cost base, and a newly secured 35-year operating license.

Risk Register

This is a high-quality asset at a depressed valuation, but it is not a risk-free position. The risks are real and worth understanding before committing capital.

The Trade

The entry zone, target, and structural thesis are clear. Here is how this position is framed in terms of risk and expected return.

Trade Parameters - SQM / NYSE

The broader framing on SQM in August 2024 is this: the market is offering a position in the world's cheapest lithium producer - with 20% global market share, a secured 35-year operating license, resilient iodine and potassium businesses, and record production volumes - at a price that implies the worst of the lithium cycle is permanent. The cycle, as always, is not permanent.

There is no precision in the timing. Cycles turn when they turn. But the entry at $36–$38 provides meaningful margin of safety relative to a wide range of reasonable lithium recovery scenarios. The risk-reward at approximately 1:4.5 - risking $7 to the stop to earn $32 to the midpoint target - reflects a patient, conviction-based position rather than a short-term trade.

The Atacama Desert has been producing lithium for nearly three decades. The Salar de Atacama sits on the world's richest lithium brine deposit, operated by a company that has navigated cycles, nationalization threats, price collapses, and political upheaval across that entire period. The world is not about to stop building batteries. Someone has to supply the lithium. At $5,000 per metric ton cash cost, SQM will still be here when the cycle turns - and it will be larger, more efficient, and better positioned than most of its competitors. That is the thesis. The entry zone is the price you pay for that certainty.

Market Research Team,

PolyMarkets Investment Strategies

Important Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. Past performance does not guarantee future results. All investments carry risk, including the possible loss of principal. Sociedad Química y Minera de Chile S.A. (NYSE: SQM) is subject to commodity price risk (lithium, iodine, potassium), emerging market risk, geopolitical and political risk related to Chilean government policy, currency risk (CLP/USD), regulatory risk including the Codelco JV conditions precedent, environmental and community consultation risk, and general market risk. Lithium prices are highly volatile and dependent on global EV adoption rates, Chinese economic policy, and new supply developments that are difficult to predict. The Codelco partnership terms, particularly the state's 85% operating margin share from 2031, may affect future shareholder returns in ways that differ from historical patterns. The Tianqi shareholder dispute represents an ongoing legal uncertainty. SQM's dividend payments depend on net income conditions as determined by the Board; there is no guarantee of dividend continuity during trough earnings periods. Valuation estimates, price targets, and EPS forecasts are based on publicly available analyst consensus and independent research as of August 2024 and may differ materially from actual outcomes. The technical analysis provided is for context only and should not be the sole basis for any investment decision. Always conduct your own thorough due diligence and consult a qualified financial advisor before making any investment decision.