You've been watching from the sidelines. Months, maybe years. Waiting for the right moment - a dip, a clearer signal, a steadier economy, some mythical day when the world feels less uncertain. I'm going to tell you something that might sting a little: that day doesn't exist. It never has.

There is no morning when markets feel obviously safe and prices feel obviously right and the decision to invest feels obvious. That's not a bug in the system. It's the system. Uncertainty is the permanent condition of financial markets, and if you wait for it to lift, you will wait forever.

What this guide gives you is the framework to act intelligently despite that uncertainty. How to choose your approach, open the right account, pick stocks systematically (or decide not to pick them at all), place orders without overpaying, and dismantle the six myths that keep otherwise smart people permanently frozen on the sidelines.

Step 1: Determine Your Investing Approach

Before opening an account or buying anything, answer one honest question: how much of your life do you actually want to spend thinking about investments? Be ruthlessly honest here. Your answer determines everything that follows, and the wrong answer leads to a strategy you'll abandon the first time things get ugly.

None of these is inherently better than the others. The best approach is whichever one you'll actually stick with when markets get ugly - and they will get ugly. A dead-simple strategy held for 30 years consistently beats a sophisticated strategy abandoned the first time the S&P drops 25%. Commitment beats complexity. Every time.

Step 2: Know Your Money Rules

This is the section people skip because they're eager to start buying. Don't skip it. The stock market is absolutely no place for money you might need in the next five years. Getting this boundary wrong is how people end up selling at a 35% loss because they needed cash for a down payment. That's not bad luck. That's bad planning.

- Your emergency fund (3–6 months of living expenses)

- Near-term education or tuition payments

- A house down payment you need within 2–3 years

- Money for planned major purchases in the next 12 months

- Any funds you cannot afford to see decline 30–40%

Why? Because 20% drawdowns in a single year aren't unusual - they happen roughly once a decade, sometimes more. And 40%+ declines, while rarer, absolutely do occur. If you're forced to sell during one of those because you need the money for rent or a medical bill, you've just converted a temporary paper loss into a permanent, real one. The whole "time in the market" thing only works if you can actually stay in the market. Money you might need soon can't afford that risk.

For money that IS investable - meaning you genuinely won't touch it for five-plus years - use the Rule of 110 as a starting allocation guide. Subtract your age from 110. That's roughly your stock percentage. Everything else goes into bonds, CDs, or cash equivalents.

| Age | Equity % | Bonds / Fixed Income % | Interpretation |

|---|---|---|---|

| 25 | 85% | 15% | Long horizon - maximum growth emphasis |

| 35 | 75% | 25% | Still growth-oriented, beginning to build stability |

| 45 | 65% | 35% | Balanced - growth and preservation in equal measure |

| 55 | 55% | 45% | Shifting emphasis toward capital preservation |

| 65 | 45% | 55% | Income and preservation - growth is secondary |

Step 3: Open the Right Account

Not all accounts are created equal, and this is one of those decisions that looks boring now but has massive consequences 30 years from now. The account type you choose determines how much of your gains you keep versus hand to the IRS. Getting this right from the start can genuinely save tens of thousands of dollars. Getting it wrong is expensive and hard to fix.

| Account Type | Tax Treatment | Withdrawal Rules | 2026 Limit | Best For |

|---|---|---|---|---|

| Standard Brokerage | Taxed on gains & dividends annually | Withdraw anytime, no penalty | No limit | Flexibility, general wealth building |

| Roth IRA ★ | After-tax contributions; growth & qualified withdrawals tax-free | Contributions anytime; gains after 59½ | $7,000 ($8,000 if 50+) | Young investors building tax-free retirement wealth |

| Traditional IRA | Contributions may be deductible; gains taxed on withdrawal | Penalty-free after 59½; RMDs at 73 | $7,000 ($8,000 if 50+) | Investors wanting immediate tax deductions |

| 401(k) / 403(b) | Pre-tax contributions; taxed on withdrawal (Roth 401k: after-tax, tax-free growth) | Penalty-free after 59½; RMDs at 73 | $23,500 ($31,000 if 50+) | Employer-sponsored retirement; especially with matching |

Step 4: How to Choose Stocks

This is where people tend to overthink things into paralysis. You do not need to read 10-K filings or build a discounted cash flow model before buying your first share. But you do need a few guardrails to keep you from doing something expensive and preventable. Five rules. That's it.

-

1

Invest in businesses you actually understand Start with companies whose products you use and whose business model you can explain in two sentences. If you can't describe how a company makes money, you have no business owning its stock. Understanding breeds conviction, and conviction is what stops you from panic-selling during the inevitable 20% drawdown.

-

2

Diversify across 25+ companies and multiple sectors Spread your money across technology, healthcare, financials, consumer staples, energy, industrials - the works. Or just buy a total market index fund like VTI and skip the individual stock-picking entirely. It holds thousands of companies for basically nothing. Honestly, for most people, that's the better answer right there.

-

3

Learn the basics of valuation P/E ratio tells you how much you're paying per dollar of earnings. EPS growth shows whether the business is actually expanding or just treading water. Revenue growth and profit margins tell you about competitive strength. You absolutely do not need to master all of this before your first purchase - but even a surface-level understanding of these four numbers will make you a dramatically better investor over time.

-

4

Stay away from meme stocks until you know what you're doing Speculative and meme stocks feel exciting. That's the problem. A stock that swings 20% per week is impossible to evaluate rationally - you're not investing at that point, you're gambling with a brokerage app. Build your skills on boring, stable, established companies first. The exciting stuff can wait until you've survived your first real downturn and know how you react.

-

5

Penny stocks are a trap. Just don't. Stocks trading below $5 are almost always there for a reason: terrible fundamentals, fraud risk, or a business that's circling the drain. The low price per share creates a seductive illusion of affordability - "I can buy 1,000 shares!" Great, you just bought 1,000 shares of a company that might not exist next year. Penny stocks have destroyed more beginning investors than any bear market in history.

Steps 5 & 6: Order Types & Placing Your Trade

A stock order is your instruction to the broker: what to buy, at what price, under what conditions. Most people never need anything beyond a market order, but understanding the menu prevents expensive mistakes during volatile sessions when prices are jumping around.

| Order Type | How It Works | Guaranteed Fill? | Best Used For |

|---|---|---|---|

| Market Order | Buy immediately at the best available current price | Yes - price may shift slightly | Buy-and-hold investors; liquid large-cap stocks |

| Limit Order | Only buy if price reaches or falls below your specified maximum | Only if price is reached | Setting a price target; avoiding overpaying in volatile sessions |

| Stop-Loss Order | Automatically sells your position if price falls to a trigger level | Yes - at or near stop price | Protecting profits; limiting downside on volatile holdings |

| Stop-Limit Order | Triggers at stop price, then places a limit order - gives price control after trigger | Not guaranteed if market gaps past limit | When you want both a trigger and price control on exit |

| Trailing Stop | Stop level moves up as stock rises; triggers only on reversal | At or near trigger level | Locking in gains on winners without a fixed exit target |

The actual process takes about 30 seconds: search the ticker on your broker's platform (e.g. AAPL), hit Buy, pick your order type, enter the dollar amount or share count, and confirm. Market orders execute in seconds. And here's the thing - for most buy-and-hold investors, a plain market order is all you'll ever need. Whether you paid $50.10 or $50.25 per share is completely irrelevant over a 10-year holding period. Don't overthink this step.

Step 7: Dollar-Cost Averaging - The Strategy That Beats Timing

You've made your first purchase. Now comes the part that actually builds wealth: automating regular contributions so your money goes in whether you feel like it or not. This strategy - dollar-cost averaging - removes emotion from the process and consistently produces results that beat every market-timing approach I've ever seen data on.

The mechanic is almost insultingly simple. Invest a fixed dollar amount on a set schedule - monthly, bi-weekly, whatever works - regardless of what the market is doing. When prices are low, your fixed amount buys more shares. When prices are high, it buys fewer. Over time, your average cost per share ends up below the average market price. You didn't need any skill or analysis to achieve that. The math just works.

| Month | Share Price | Amount Invested | Shares Purchased |

|---|---|---|---|

| January | $50.00 | $200 | 4.00 |

| February (market dip) | $40.00 | $200 | 5.00 |

| March | $45.00 | $200 | 4.44 |

| April (market rally) | $55.00 | $200 | 3.64 |

| May | $60.00 | $200 | 3.33 |

| Totals / Averages | Avg market price: $50.00 | $1,000 invested | 20.41 shares - avg cost $49.00/share |

Your average cost ($49.00) came in below the average market price ($50.00) - simply because you bought more shares during the dip and fewer during the rally. No forecasting. No analysis. No gut feelings. Multiply that mechanical advantage over 20-30 years and the impact is massive. As Buffett puts it: "You don't need to do extraordinary things to achieve extraordinary results." Broad index funds, regular contributions, decades of patience. That's it.

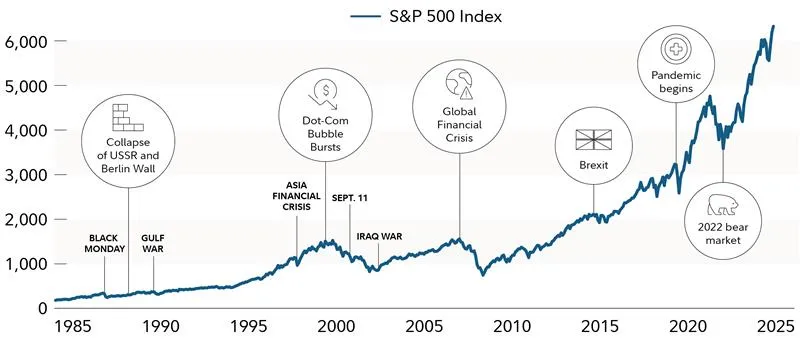

What S&P 500 History Actually Shows

If you're nervous about getting in, this section is the antidote. The S&P 500 has survived two world wars, the Great Depression, stagflation, the dot-com bubble, 9/11, the financial crisis, a global pandemic, and whatever we're calling the current situation. Through every single one of those, the long-term trend has been up.

What this chart makes viscerally clear: every "worst time to invest in history" - 1929, 1987, 2000, 2008, 2020 - looks, with any distance at all, like a buying opportunity rather than a catastrophe. The people who held didn't just recover their losses. They built substantial wealth on the other side. Every single time.

And here's a stat that should permanently cure your timing impulse: missing just the 10 best trading days in an entire decade cuts your long-term returns dramatically. Not 10 best years. Ten best days. And those best days almost always cluster right around the worst days - during the exact crisis volatility when everyone is running for the exits. So the investors who flee to cash during downturns don't just miss the pain. They miss the snapback that follows it. Staying invested, even at a bad time, outperforms most attempts to time the market over any 20-year stretch.

6 Timing Myths - Busted

These six beliefs have collectively kept millions of otherwise capable people from ever investing. Each one sounds reasonable on the surface - that's exactly why they're so effective at keeping you stuck.

Benefits vs. Risks of Stock Investing

Stocks have delivered the highest long-run returns of any major asset class. That's the good news. The bad news is that those returns come with real, sometimes stomach-churning risks. Understanding both sides - honestly, without sugarcoating either one - is how you build the conviction to stay in when things get rough.

- Long-run returns: Major stock averages have historically returned 9-12% annually over multi-decade periods. Nothing else - not bonds, not real estate, not gold - has consistently matched that over long stretches

- Inflation protection: Company revenues and profits tend to rise with prices, which makes stocks one of the best inflation hedges available. Your purchasing power grows instead of eroding

- Dividend income: Plenty of established companies pay growing quarterly dividends - passive income that compounds quietly in the background, year after year

- Liquidity: You can sell stocks at full market value any time the market is open. Try doing that with real estate or a private equity stake

- Real ownership: Each share is actual equity in a business that employs people, generates revenue, and creates economic value. This isn't a bet on a number - it's ownership of productive assets

- Short-term volatility: 10% swings in a given year are completely normal. 20-40% drawdowns happen roughly once a decade. Without a long time horizon, this is genuinely dangerous to your goals

- Company-specific risk: Individual stocks can go to zero. Ask anyone who held Lehman Brothers, Enron, or SVB in a concentrated position. Diversification isn't optional

- Behavioral risk: You. Panic selling during downturns is the single most expensive mistake investors make - locking in losses days or weeks before the recovery begins

- Interest rate risk: When rates rise, stock valuations get compressed - especially for high-growth companies whose earnings are years in the future. The more speculative the stock, the harder it gets hit

6 Mistakes New Investors Make

Wealth in the stock market isn't built by finding the next Amazon before everyone else. It's built by consistently avoiding the mistakes that blow up everyone else's portfolio. The bar for success is lower than you think - you mostly just have to not do these six things.

Buying when stocks are soaring because your coworker just bragged about his gains, then selling when they're falling because it "feels safer." This is literally buy high, sell low - the exact opposite of every investing principle ever written. And it's the single most common reason everyday investors underperform the very indices they invest in. Your feelings are the worst financial advisor you have.

The research on this is brutal. A Brazilian study found 97% of day traders who persisted for more than 300 days lost money. Ninety-seven percent. Short-term price movements are noise dressed up as signal, and the people trying to profit from that noise are playing a game where the house - in the form of commissions, spreads, and taxes - always wins. An index fund beats the vast majority of day traders with zero effort.

Borrowing money to buy stocks is a loaded gun pointed at your own portfolio. A 30% decline on a position held with 2x leverage wipes out 60% of your capital. And you still owe interest on the money you borrowed. Margin has a legitimate place for experienced traders in specific tactical situations. For someone building long-term wealth, it is a fast track to a margin call and a hard lesson.

Even the best-researched stock on the planet can drop 70-90% in a crisis. It happened to GE. It happened to Meta. It nearly happened to Netflix. Position sizing and sector diversification protect you from the scenario where you're right about the market direction but catastrophically wrong about one company's fate. No single position should make or break your portfolio.

This one is pure money left on the table. Short-term capital gains (positions held under a year) are taxed at ordinary income rates - 22-37% for many investors. Long-term gains (over a year) drop to 0-20%. The simple act of waiting 366 days instead of 364 to sell a winner can save you thousands of dollars on a single trade. It's the easiest optimization in all of investing and most beginners don't even know it exists.

Options involve time decay, leverage, and payoff structures that are deeply counterintuitive until you've really studied them. They're not just "cheaper stocks" - they're a completely different instrument with completely different risk characteristics. New investors who trade options before understanding basic equity investing lose money with remarkable consistency. Build the foundation first. The options aren't going anywhere.

4 Core Strategies Every Long-Term Investor Needs

No shortcuts here. No hot tips. These four strategies are what professional and successful long-term investors actually do - across every market cycle, in every economic environment, decade after decade. They're boring. They work.

-

1

Buy and Hold - The Foundation Find quality businesses at reasonable valuations. Buy them. Then hold them for as long as the underlying business remains strong. That's it. This strategy beats most active approaches because it minimizes trading costs, defers capital gains taxes, and eliminates the psychological errors that come with frequent trading. Warren Buffett's preferred holding period is "forever." He's not joking.

-

2

Dollar-Cost Averaging - The Engine Fixed amount, fixed schedule, regardless of price. Automate it so it doesn't require willpower - because willpower fails exactly when you need it most, during drawdowns. Over decades, DCA consistently builds more wealth than most active strategies by taking emotion out of the two decisions that matter most: when to buy and how much. Remove yourself from the equation. You'll do better.

-

3

Tax Optimization - The Multiplier Put income-generating assets (dividend stocks, REITs, bond funds) in tax-advantaged accounts like your Roth IRA or 401(k) where that income is sheltered. Keep growth stocks and non-dividend ETFs in your taxable brokerage where unrealized gains compound without annual tax drag. Hold winners longer than a year for the long-term rate. The tax code is one of the few things in investing you can actually control - make it work for you instead of against you.

-

4

Rebalancing - The Maintenance Once a year, look at your portfolio. If any position or asset class has drifted significantly from your target allocation - say your 80/20 stock-bond split has become 90/10 after a strong equity year - trim the winners and redeploy into the underweight areas. It feels counterintuitive to sell what's working, but rebalancing enforces discipline, manages drift risk, and consistently improves risk-adjusted returns over decades. Ten minutes a year. That's all it takes.

PolyMarket Investment, Research Team, July 2025