There is a company in Veldhoven, Netherlands, that builds machines so complex, so capital-intensive, and so irreplaceable that every leading-edge semiconductor chip on Earth - every AI accelerator, every 2-nanometer logic wafer, every HBM memory stack - must pass through its technology before it exists. That company is ASML. It does not compete. It enables.

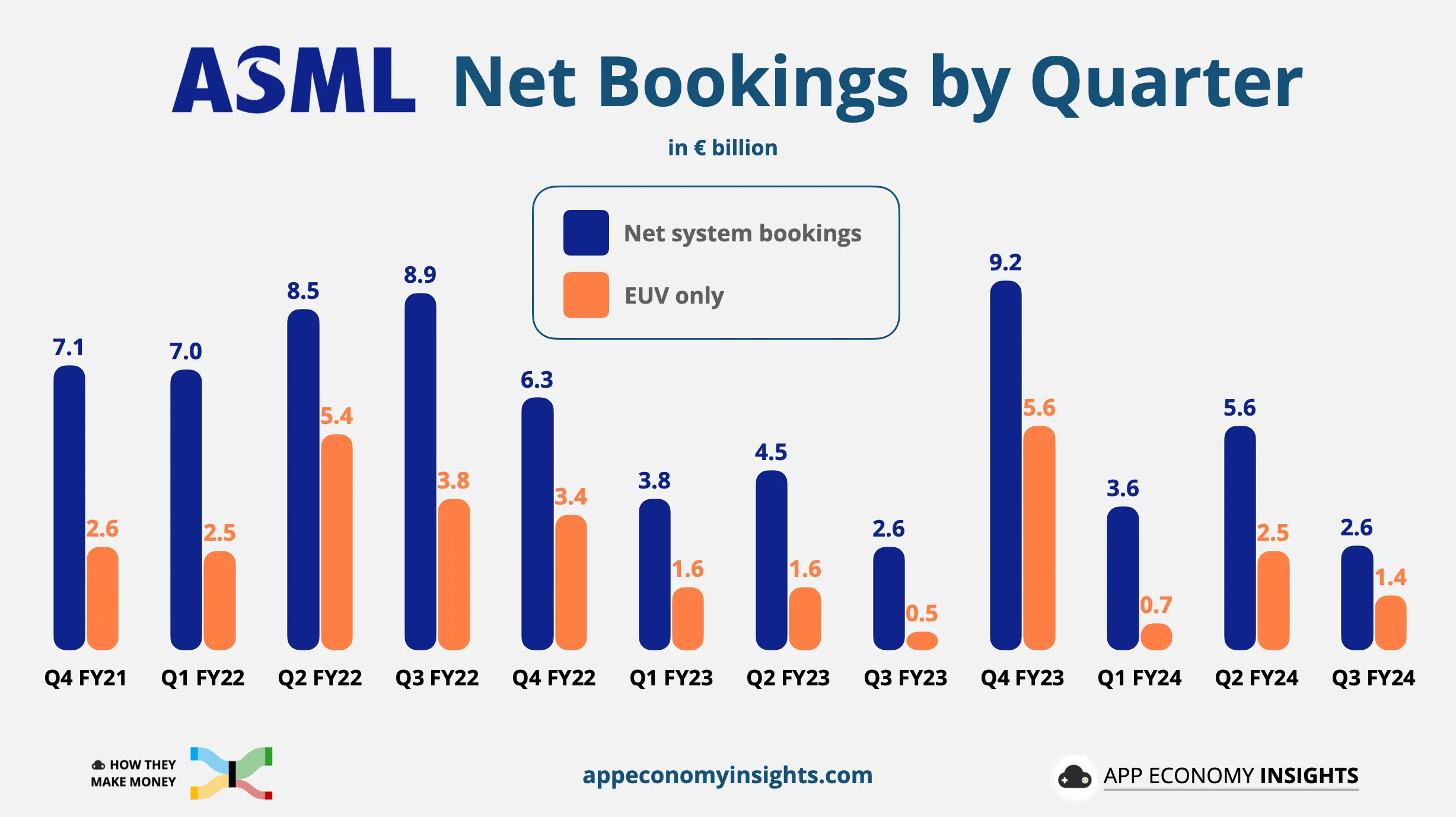

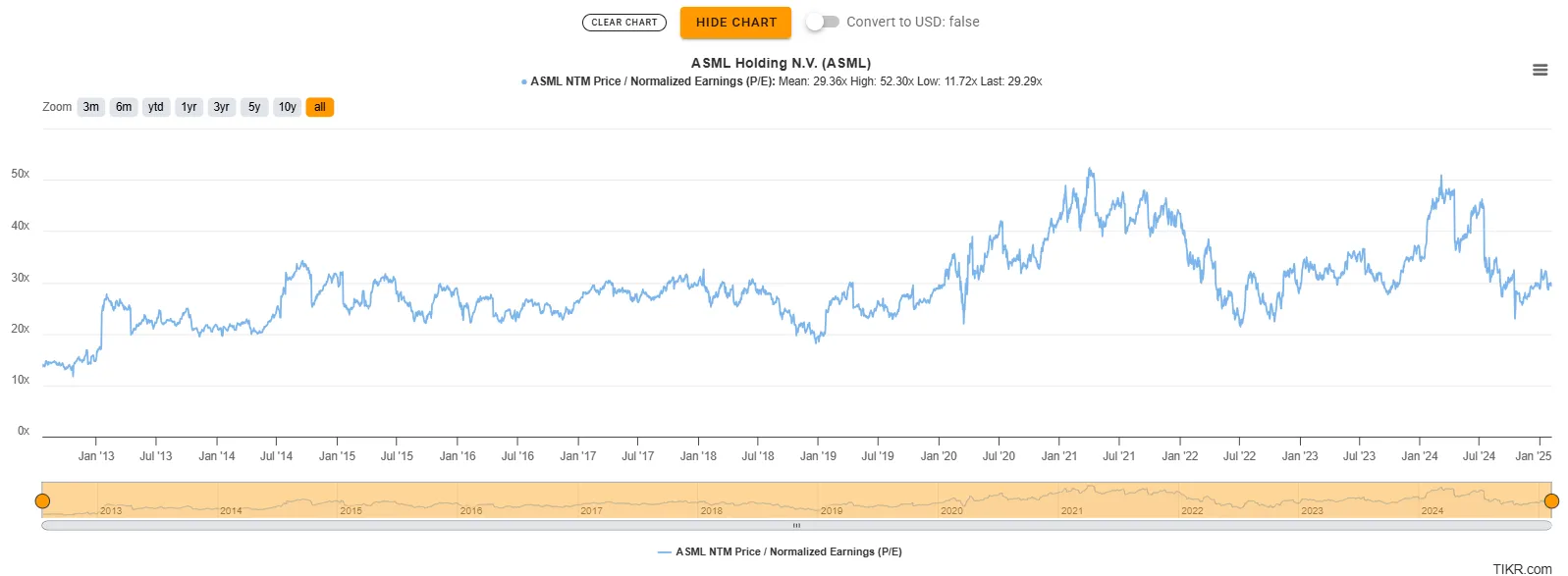

Two days ago, ASML reported Q4 2024 earnings that exceeded the high end of guidance, posted EUR 7.1 billion in net bookings against a consensus of EUR 3.5 billion, and confirmed a systems backlog of approximately EUR 36 billion. The stock sits at roughly $739, trading at 29.3x forward normalized earnings - precisely its long-term average since 2012. The question is not whether ASML is a good company. The question is whether the market has fully absorbed what the next three years look like when every hyperscaler on Earth is simultaneously building out AI compute capacity that depends entirely on ASML's machines.

We believe it has not. This is our thesis.

Start with the moat, because it is unlike anything else in technology. ASML holds a 100% monopoly on extreme ultraviolet (EUV) lithography - the technology required to manufacture chips at 7nm and below. There is no alternative supplier. There is no Chinese substitute. There is no startup in stealth mode threatening disruption. The barriers are not just high; they are, in any practical sense, impassable.

An EUV lithography system contains over 100,000 individual components, weighs approximately 180 tonnes, and requires multiple 747 cargo planes to ship. The light source alone - a CO2 laser that fires 50,000 droplets of molten tin per second, each struck twice to produce 13.5nm wavelength light - took Carl Zeiss SMT and ASML over two decades to commercialize. The mirrors inside the system are polished to atomic-level flatness; if scaled to the size of Germany, the largest imperfection would be less than one millimeter tall.

This is why ASML trades at a premium. A premium to the semiconductor sector median P/E of 31.65x, a premium to the sector median P/S of 3.37x (ASML's current P/S is 9.49x). But that premium is not valuation excess - it is the market's recognition that ASML's competitive position is closer to a natural monopoly than to a typical tech company. What the market has yet to fully price, we believe, is the volume and duration of the demand cycle now unfolding.

Context matters here. In Q3 2024, ASML posted net bookings of just EUR 2.6 billion against expectations of EUR 5.6 billion. The stock dropped approximately 20% in a single session - one of the worst single-day declines for a European large-cap in years. The narrative shifted overnight: the AI demand cycle was peaking, customers were pulling back, ASML's guidance range of EUR 30-35 billion for 2025 looked like a ceiling rather than a floor.

Then Q4 happened.

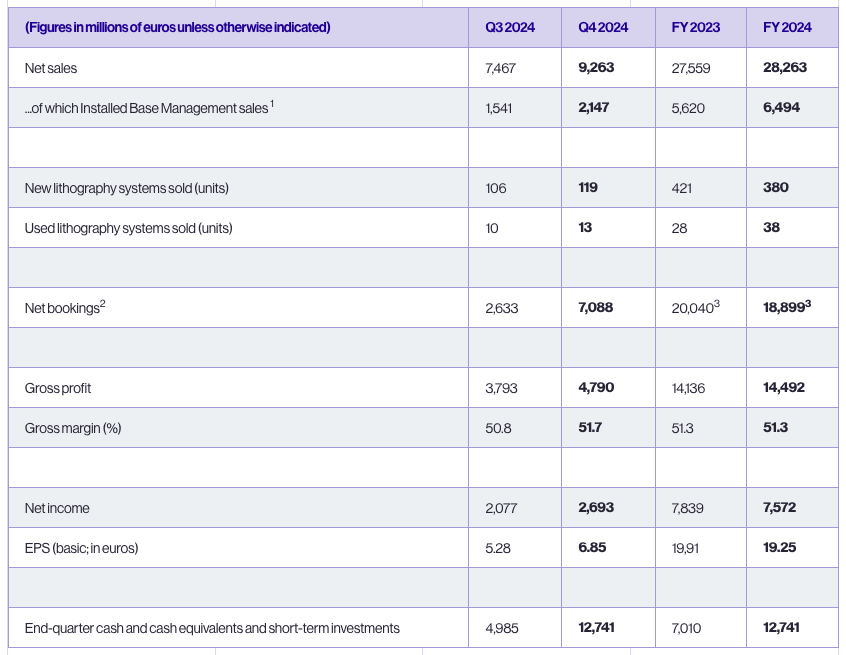

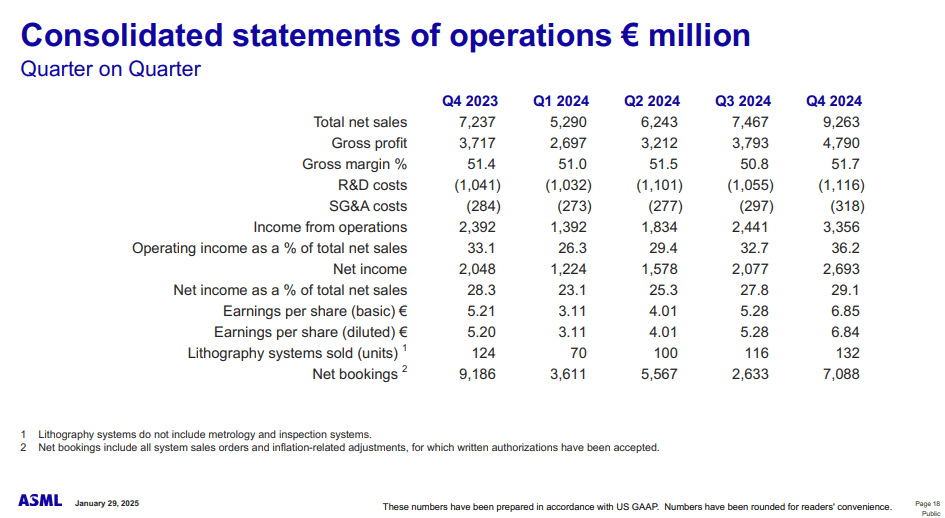

Net sales came in at EUR 9.263 billion, above the high end of guidance. That is not a marginal beat. It is a company telling the market "our numbers will be between X and Y" and then exceeding Y - in a quarter where installed base revenue contributed an outsized EUR 2.1 billion (reflecting upgrade business that exceeded internal plans). Gross margin printed at 51.7%, up from 50.8% in Q3, driven partly by lower-than-planned costs on High-NA system introductions - a signal that the new technology is maturing faster than ASML's own financial models assumed.

But the real headline was bookings. EUR 7.088 billion in net system bookings - EUR 3 billion of that in EUV, EUR 4.1 billion in non-EUV - against a consensus expectation of approximately EUR 3.5 billion. This was a 2x beat on bookings. The message from customers was unambiguous: they are ordering. They are building. The demand is real.

"Total net sales were EUR 9.3 billion, which is above the high end of our guidance primarily due to installed base revenue. Gross margin for the quarter was above guidance at 51.7% due to a combination of additional upgrade business and lower than planned costs associated with the new product introduction of High-NA systems in the field."

- Roger Dassen, EVP & CFO, ASML Q4 2024 Earnings CallFull-year 2024 revenue reached EUR 28.263 billion with a gross margin of 51.3%. Net income for the year was EUR 7.6 billion (EUR 19.25 per share), and free cash flow was EUR 9.1 billion. The company returned EUR 3 billion to shareholders through dividends and buybacks and declared a total 2024 dividend of EUR 6.40 per share.

The investment case for ASML does not begin with ASML. It begins with the companies writing checks - the hyperscalers whose capital expenditure plans have entered territory that, even two years ago, would have seemed implausible.

| Hyperscaler | 2024 CapEx | 2025 CapEx (Planned) | YoY Change |

|---|---|---|---|

| Microsoft | $55.55B | $80B | +44% |

| Alphabet | $52.54B | $75B | +43% |

| Amazon | $83B | ~$100B | +20% |

| Meta | $37.26B | $60-65B | +61-74% |

| TSMC | $29.1B | $38-42B | +31-44% |

Consider the chain. Microsoft, Alphabet, Amazon, and Meta collectively plan to spend approximately $315-320 billion on capital expenditure in 2025 - up from roughly $228 billion in 2024. Mark Zuckerberg has spoken of "hundreds of billions" in long-term AI infrastructure investment. This money flows to data center builders, who buy servers, which contain AI accelerators (NVIDIA, AMD, custom ASICs), which are fabricated by foundries (TSMC, Samsung, Intel), which cannot manufacture a single leading-edge wafer without ASML's EUV lithography systems.

TSMC alone has guided $38-42 billion in 2025 capital expenditure, with 70% allocated to advanced process technologies - the nodes that require EUV. This is up from $29.1 billion in 2024. Samsung and Intel, despite their respective challenges, remain committed to leading-edge node development and have active EUV installation programs. Every single one of these programs passes through ASML.

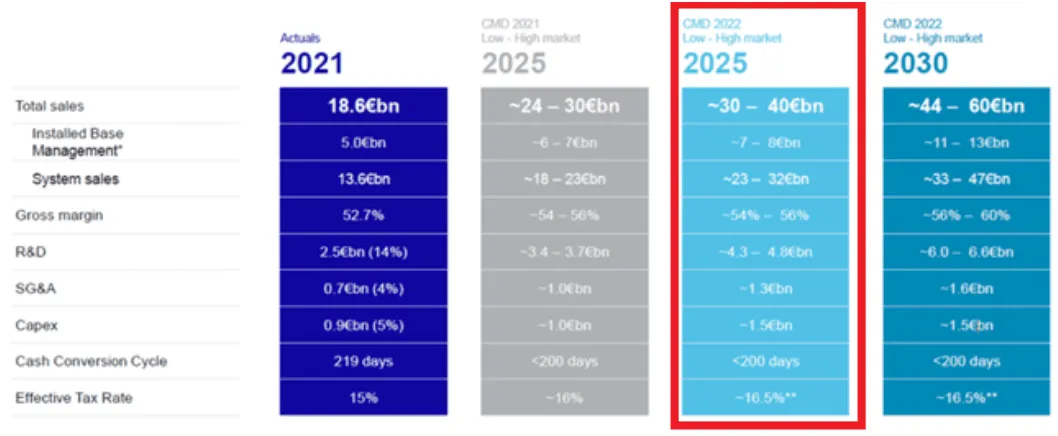

The semiconductor industry is projected to reach $1 trillion in revenue by approximately 2030, according to Gartner consensus data. If ASML achieves the midpoint of its own 2030 target (approximately EUR 52 billion, or roughly $54 billion), that represents about 5.4% of the total semiconductor market - a company that captures over 5% of the industry's total revenue despite making none of the chips itself. It makes the machines that make the machines. And there is no substitution available.

"We anticipate that an increased number of critical lithography exposures for these advanced Logic and Memory processes will drive increasing demand for ASML products and services."

- Christophe Fouquet, President & CEO, ASML

ASML is not a one-product company. Its technology portfolio spans four distinct layers, each contributing to revenue growth and margin expansion on different timelines. Understanding this stack is essential to understanding why the 2025-2030 growth trajectory has more structural support than the market is pricing.

The Low-NA EUV platform - the NXE:3800E - is now the workhorse of the semiconductor industry. In Q4, ASML demonstrated full system specifications at 220 wafers per hour with a new record overlay. The target is 400-500 wafers per hour by 2030. Since 2015, EUV productivity has grown 44% more than its price. This is a critical data point: ASML is not just raising prices; it is delivering accelerating value per dollar, which strengthens customer willingness to pay and supports the margin expansion trajectory toward 56-60% by 2030.

On High-NA EUV - the next generation - ASML completed installation and customer acceptance on two systems in Q4. Customers have processed over 10,000 wafers on High-NA systems, and the feedback, per CEO Christophe Fouquet, has been "very positive" with "major performance benefits in imaging, overlay and contrast which also provide significant cost reduction opportunities for both Logic and DRAM processes." A third High-NA system was shipped in Q4 and is undergoing installation - notably, this system is not going to the previously identified North American customer (widely assumed to be Intel), suggesting Samsung or TSMC is the recipient.

"On High NA EUV, we completed the installation and customer acceptance on two systems in Q4. Customers have now run over ten thousand wafers on High NA systems and their feedback has been very positive. They are seeing major performance benefits in imaging, overlay and contrast which also provide significant cost reduction opportunities for both Logic and DRAM processes."

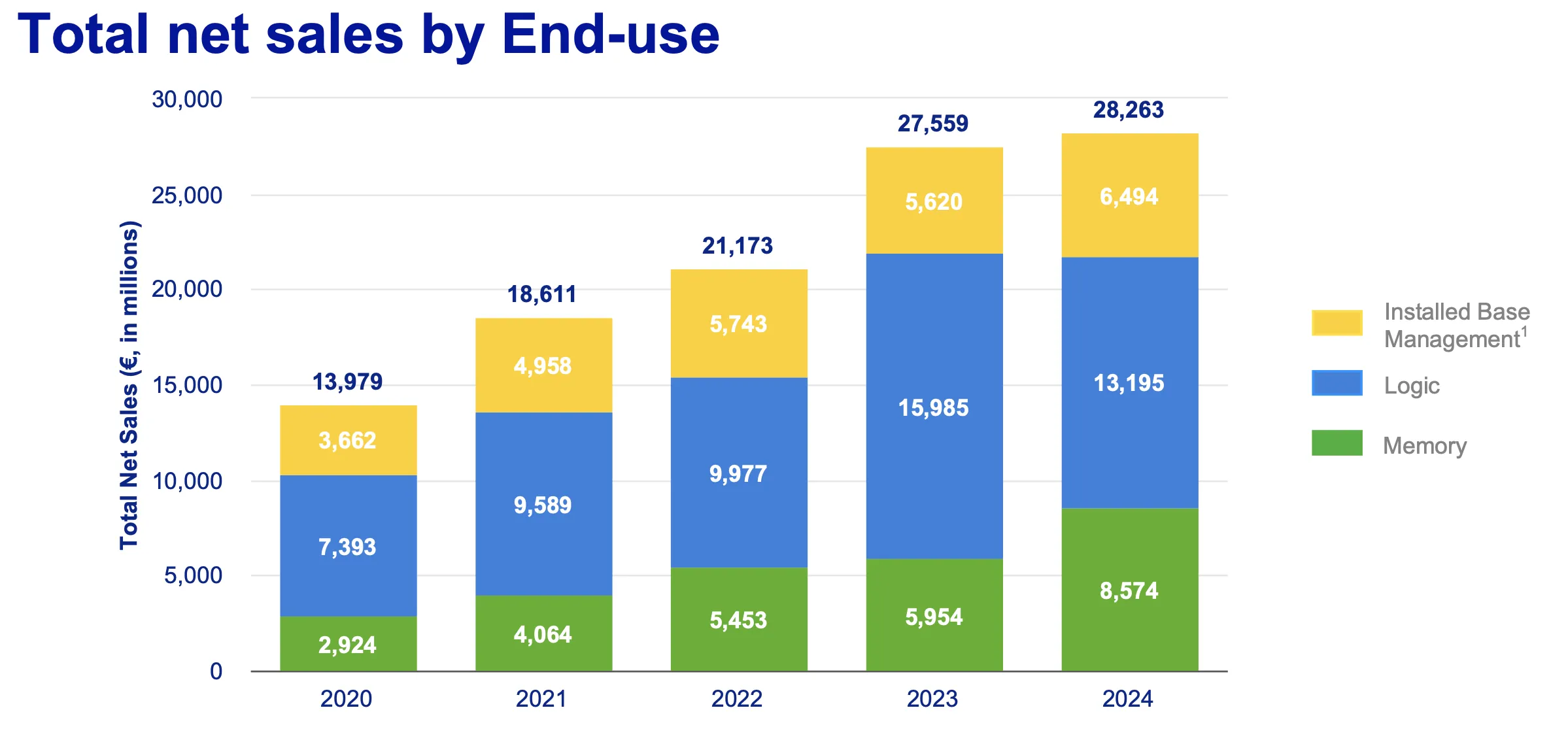

- Christophe Fouquet, CEO, ASML Q4 2024 Earnings CallIn the Installed Base Management segment, ASML generated EUR 6.5 billion in 2024, up 16% year-over-year, and is targeting EUR 7.5 billion for 2025. This business - essentially a service and upgrade annuity on the thousands of ASML systems operating worldwide - provides a recurring revenue floor that smooths cyclical volatility. By 2030, management targets EUR 11-13 billion from this segment alone. That single business line would make it larger than many entire semiconductor companies.

And there is a signal the market has underappreciated: the eScan 1100 multi-beam inspection system. ASML confirmed first revenue recognition after completing evaluations with multiple customers. This is an expansion into metrology and inspection - a market adjacent to lithography where ASML's deep process knowledge gives it a structural advantage.

On January 27, 2025 - just two days before ASML's Q4 report - the semiconductor sector experienced a sharp selloff triggered by DeepSeek, the Chinese AI lab that reportedly trained a competitive large language model for approximately $5.6 million. ASML dropped roughly 10% to $683. The fear was straightforward: if AI models can be built cheaply, maybe the hyperscalers do not need all those GPUs, and maybe TSMC does not need all those EUV machines.

This interpretation misunderstands the economics at every level.

First, the $5.6 million figure covers only the final training run of one model, not the total research expenditure, data preparation, or the compute used for experimentation. The full cost is substantially higher, and DeepSeek itself relied on NVIDIA H100 GPUs manufactured on TSMC's advanced nodes using ASML's EUV systems.

Second - and this is the critical insight - cheaper AI models do not reduce compute demand. They increase it. This is Jevons' Paradox applied to machine intelligence: when the cost per unit of AI inference drops, the total volume of inference explodes. More efficient models mean AI gets deployed in more applications, more edge devices, more languages, more modalities. The total compute envelope grows.

Third, look at what actually happened in the week following DeepSeek. Every major hyperscaler either confirmed or increased its 2025 CapEx guidance. Microsoft committed to $80 billion. Meta raised to $60-65 billion. Google Cloud missed revenue estimates not because demand softened, but because it could not meet demand - a capacity constraint, not a spending constraint. The market's initial panic was a gift.

"We see more upside than risk, at least with all the elements we have at hand."

- Christophe Fouquet, CEO, on AI demand outlook, ASML Q4 2024 Earnings CallThe most productive way to assess ASML's current pricing is to separate the market's surface-level narrative from the operational reality visible in the earnings data, the backlog, and management's commentary.

What the Market Sees

- FY24 EPS fell -3.3% YoY (EUR 19.25 vs EUR 19.91)

- China revenue normalizing from 41% to ~20%

- Q3 booking miss created crisis of confidence

- DeepSeek questions AI spending durability

- No share buybacks in Q4 when stock was near lows

- Bookings reporting ends after 2025 (opacity risk)

What the Fab Floor Shows

- Q4 bookings at EUR 7.1B - double consensus expectations

- Q1 2025 guidance: EUR 7.5-8.0B revenue, 52-53% margin

- 2025 revenue guide EUR 30-35B with upside if AI demand holds

- EUR 36B backlog = ~5.5 quarters of workload at clearing rate

- High-NA maturing faster than planned (lower NPI costs)

- Installed base revenue at EUR 2.1B in Q4 alone (above plan)

- 2026 positioned as a growth year per CFO Dassen

- 2nm ramp starting 2025, extending through 2027

The EPS decline in 2024 was real but misleading. Revenue grew 2.55% to EUR 28.263 billion while margins held steady at 51.3%. The EPS compression reflected elevated R&D spending - EUR 4.3 billion, or 15% of sales - invested in next-generation platforms including High-NA and the new DUV systems. This is the kind of "declining earnings" that precedes accelerating earnings: the investment is being made now; the revenue recognition comes in 2025-2027.

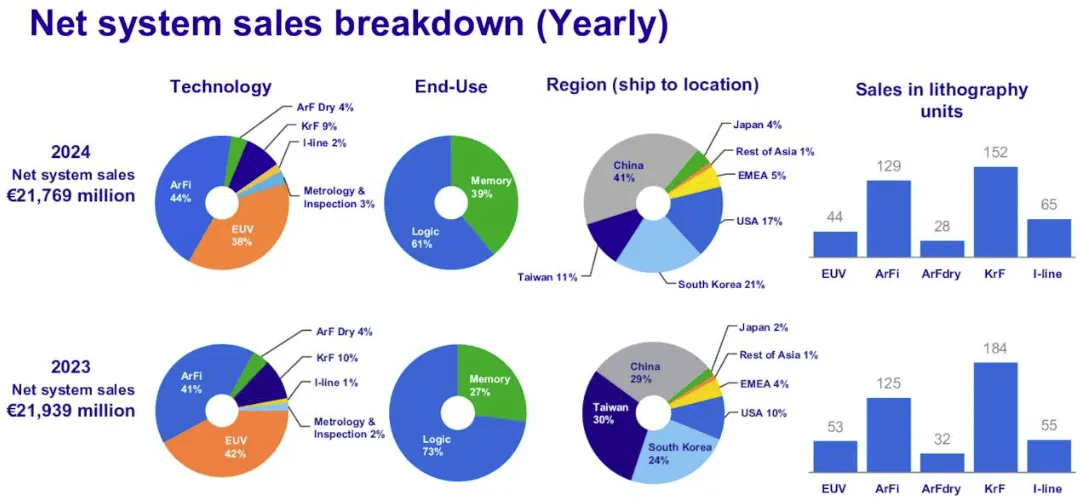

The China normalization is already well-understood. China represented 41% of ASML's revenue in FY2024, up from 29% in FY2023, as the company executed on a backlog built during periods of lower order fill rates. CFO Roger Dassen has been explicit: "We think that is a low 20% number that China will represent in 2025 in our total sales numbers." The decline in China from 47% in Q3 to 27% in Q4 shows the normalization is already well underway. (The full-year 41% sits between these quarterly snapshots because H1 2024 carried an even heavier China weighting - Chinese customers front-loaded orders ahead of anticipated export control tightening, skewing the annual average upward relative to where Q4 landed.) The important corollary: non-China, non-EUV business is expected to grow approximately 40% in 2025, on par with EUV growth. The China headwind is being offset by structural demand elsewhere.

"We needed about EUR 2 billion of EUV orders to get covered for EUV on the midpoint of 2025. So with the EUR 3 billion that we have in there, we've reached that point. Should continue to see good order intake in the first two quarters for 2026 coverage."

- Roger Dassen, CFO, ASML Q4 2024 Earnings CallThat last quote is worth lingering on. ASML is already EUV-covered for the midpoint of 2025 revenue guidance. The order intake in H1 2025 will be building coverage for 2026 - a year Dassen has described as "a potential growth year." The backlog provides an unusual degree of forward visibility for a cyclical company.

No honest ASML analysis can avoid the geopolitical dimension. China was ASML's largest market in 2024 at 41% of net system sales, up from 29% in 2023. The company has been executing on a DUV-heavy backlog from Chinese customers who cannot access EUV technology due to export controls. For 2025, management has guided China to normalize to the low 20% range.

The 41% FY2024 figure reflects the full four-quarter mix across a year of significant within-period variation. H1 2024 carried an exceptionally heavy China weighting - Chinese customers were accelerating purchases ahead of anticipated export control tightening, likely pushing H1 China share above 50%. Q3 remained elevated at 47% as that front-loading continued. Q4 then dropped sharply to 27% as the backlog cleared and new restrictions came into force. The FY average of 41% is therefore consistent with the quarterly data: it is a blend of a front-loaded H1 well above 47%, a still-elevated Q3 at 47%, and a Q4 that had already begun normalizing toward the 20% guided for 2025. These are quarterly snapshots of a trajectory, not contradictory figures from different reporting bases.

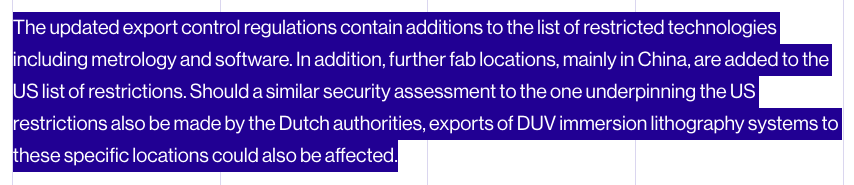

The risk is well-known: further tightening of US, Dutch, or Japanese export controls could reduce China's share even below 20%. The updated export control regulations already contain additions to the list of restricted technologies, including metrology and software. Additional fab locations in China have been added to the US restriction list, and should Dutch authorities make a similar security assessment, DUV immersion lithography exports to specific locations could also be affected.

However, several factors mitigate this risk more than the market appreciates. First, CEO Fouquet has stated that China is 10-15 years behind leading-edge semiconductor capabilities. The chips China can make with ASML's DUV systems (28nm and above) serve automotive, industrial, and legacy applications - not the AI frontier. Restricting these sales would hurt ASML's revenue but would not meaningfully alter the geopolitical balance in advanced computing.

Second, the normalization is already happening organically. Q4 China orders were described by Dassen as "healthy" and "relatively normal" - not an anxious pre-restriction stockpiling. The backlog-clearing dynamic that drove 41% China revenue in 2024 is a one-time phenomenon, not a sustainable baseline.

Third - and this is the structural point - even if China revenue goes to zero (an extreme downside scenario), ASML's EUR 30-35 billion 2025 guidance and EUR 44-60 billion 2030 target are built primarily on the leading-edge roadmaps of TSMC, Samsung, and Intel. The AI CapEx supercycle is being funded by Western and Taiwanese capital. China is a revenue bonus, not the thesis.

The stock sits at approximately $739 as of January 31, 2025. At this price, ASML trades at 29.3x next-twelve-months normalized earnings - virtually identical to its long-term average of 29.4x since July 2012. The five-year average forward P/E is higher, at 35.6x. In mid-2024, the P/E touched nearly 60x before the Q3 booking miss brought it back to earth. Today's valuation is neither cheap in absolute terms nor expensive relative to ASML's own history.

But the earnings trajectory is about to inflect. Consensus estimates project EPS of $24.53 for FY2025 (+23% YoY), $29.66 for FY2026 (+21% YoY), and $34.01 for FY2027 (+15% YoY). The 2024 EPS compression was driven by investment; 2025-2027 is when that investment converts to revenue.

The math toward our target zone is straightforward. At $29.97 consensus EPS for 2026, a 30x multiple yields $899. At the five-year average of 35.6x, it yields $1,067. At $35.92 EPS for 2027, a conservative 28x yields $1,006, while 30x yields $1,078. Our target range of $980-$1,080 implies that ASML trades at 28-32x earnings on 2026-2027 consensus estimates - below its five-year average multiple. This is not a heroic assumption. It is asking the stock to not de-rate while earnings grow 20%+ annually.

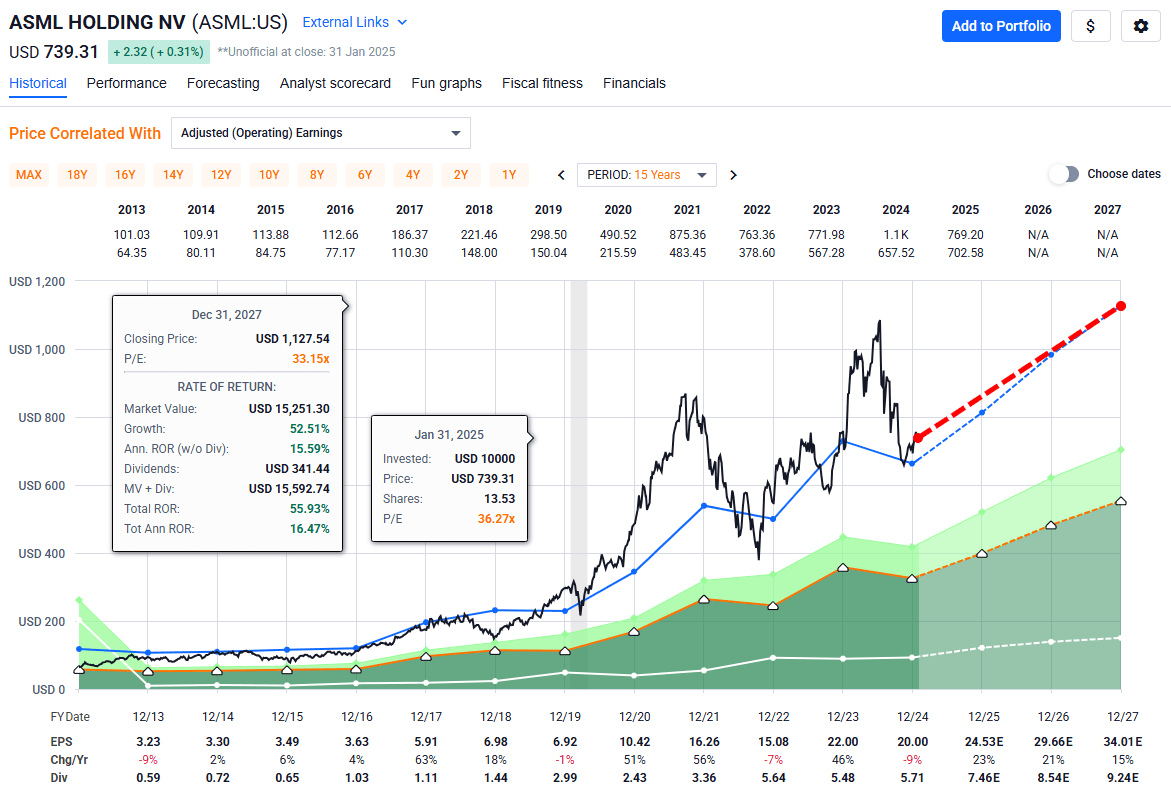

The FAST Graphs analysis supports this framework. From a January 31, 2025 entry at $739.31, the model projects a December 2027 price of $1,127.54 at a 33.15x P/E - representing a total annual return of 16.47% including dividends. On a $10,000 investment, that translates to a market value of $15,251 plus $341 in dividends over the period.

Note on the FAST Graphs assumption: The model's 33.15x P/E sits above ASML's long-term average of 29.4x (since July 2012), which means the $1,127 target incorporates modest multiple expansion alongside earnings growth - it is not a multiple-neutral projection. At the long-term average P/E of 29.4x applied to the 2027 consensus EPS estimate of $35.92, the implied price would be approximately $1,056. That figure still represents over 40% upside from today's entry and remains well within our target range, confirming that the base case does not require any re-rating of the multiple to be constructive. Multiple expansion to 33x, should it occur, is an additional source of return rather than the primary driver of the thesis.

The P/S ratio tells a complementary story. At 9.49x trailing sales, ASML trades below its three-year average (which exceeded 15x in mid-2024). If P/S mean-reverts to the long-term average of 11.7x, that alone implies over 23% upside - before any earnings growth is factored in.

Management's own CMD targets call for EUR 44-60 billion in revenue by 2030 with gross margins of 56-60%. The Street consensus clusters near EUR 57 billion (the high end of the range). If achieved, ASML's operating leverage would produce a significant step-up in profitability: the margin expansion from 51% to 58-60% on a revenue base that roughly doubles represents an earnings power substantially beyond current consensus. The 2030 installed base management target of EUR 11-13 billion alone would be a company-defining revenue stream.

The 2-nanometer node is the next major inflection point for the semiconductor industry, and ASML sits at its center. TSMC's N2 process is scheduled to begin risk production in 2025, with volume ramp extending into 2026 and 2027. This is not a single quarter event - it is a multi-year build-out that will require significant additional EUV capacity.

"The ramp is starting 2025, extending into 2026 and most probably into 2027. Maybe there is an opportunity to ramp a bit faster if the demand remains strong - a mix of 2-nanometer and some subsequent node."

- Roger Dassen & Christophe Fouquet on the 2nm timeline, ASML Q4 2024 Earnings CallThe 2nm node requires more EUV lithography exposures per wafer than previous nodes. Each additional critical layer is an additional pass through an ASML machine, which means more systems needed, more installed base revenue generated, and more upgrade business as customers push for higher throughput. This is the structural dynamic that makes semiconductor scaling an inherent tailwind for ASML: as chips get more complex, they need more lithography.

Intel's Foundry Services remains a wildcard. Intel has been the identified "North American customer" for High-NA EUV, but delays in Intel 18A and broader restructuring questions have created uncertainty. However, the Q4 revelation that the third High-NA shipment went to a customer other than Intel (likely Samsung or TSMC) suggests High-NA demand is broadening beyond Intel - which reduces single-customer risk. Even if Intel Foundry Services is acquired or scaled back, the EUV demand from TSMC and Samsung alone would sustain ASML's growth trajectory.

ASML itself is investing to match this demand. R&D spending reached EUR 4.3 billion in 2024 (15% of sales), and the company continues its pre-build strategy to level-load the factory and offer customers "normal" order lead times rather than the extended 12-18 month backlogs that characterized 2022-2023.

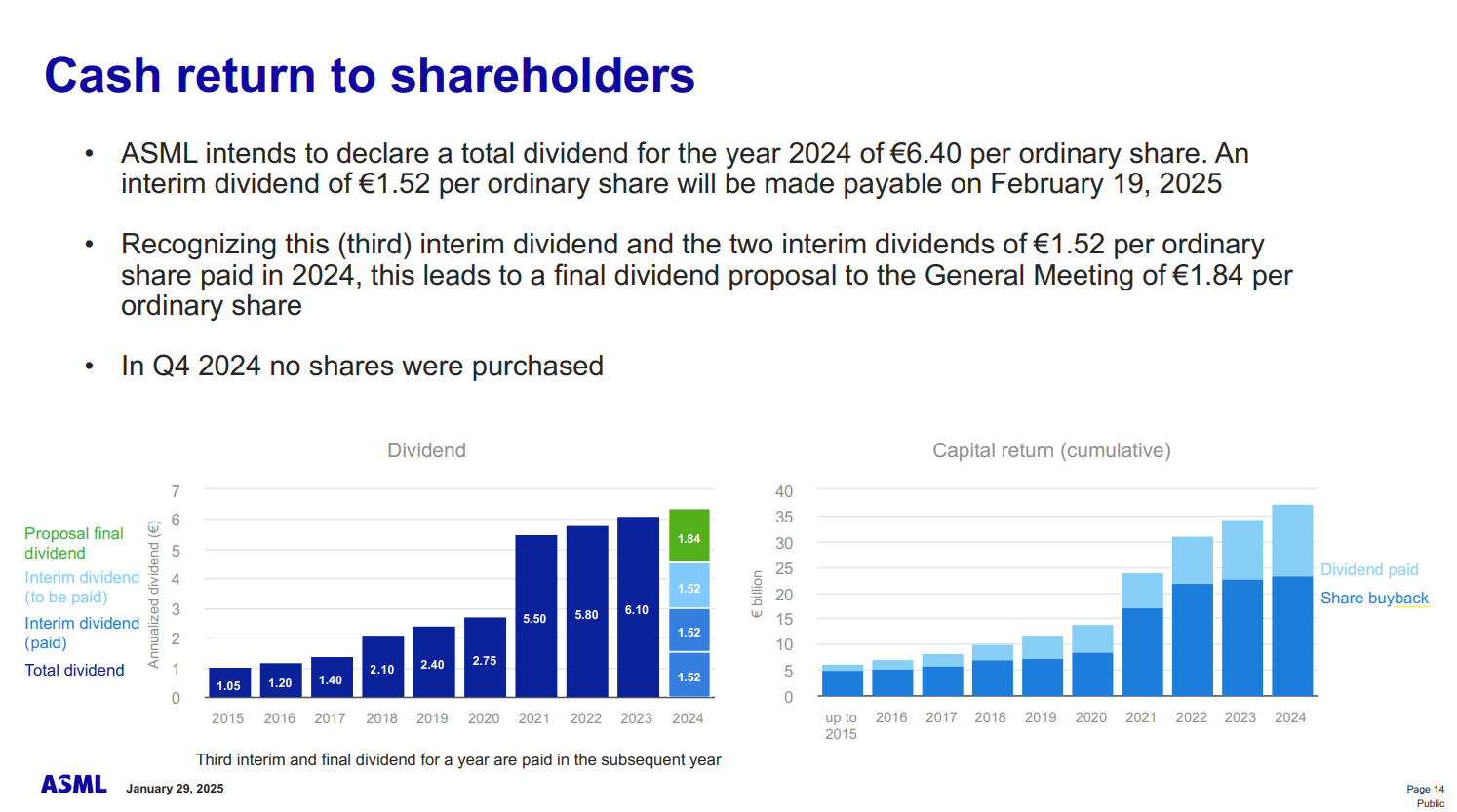

There is one legitimate criticism of ASML's management that deserves acknowledgment. In Q4 2024, as the stock traded near EUR 600 following the Q3 booking miss, the company purchased zero shares. Yet during 2020-2021, when the stock was trading at or near all-time highs, management was actively buying back shares. This is, to put it plainly, capital allocation that is precisely backwards.

European companies have historically been less disciplined about opportunistic share repurchases than their American counterparts, and ASML fits this pattern. The company returned EUR 3 billion to shareholders in 2024 through a combination of dividends and buybacks, declared a total 2024 dividend of EUR 6.40 per share (up from EUR 6.10 in 2023), and ended Q4 with EUR 12.74 billion in cash and short-term investments - up from EUR 7 billion at the end of 2023.

The cash position is robust. Free cash flow of EUR 9.1 billion in 2024 supports both the dividend trajectory and future buyback activity. The dividend has grown from EUR 1.05 in 2015 to EUR 6.40 in 2024 - a more than 6x increase over nine years. Projected dividends of $7.46 (2025), $8.54 (2026), and $9.24 (2027) represent an additional return stream that, while modest in yield terms (~1%), reflects the consistent cash generation of the underlying business.

But the missed buyback opportunity at EUR 600 is a real cost. If management had deployed even EUR 1 billion at the November lows, the per-share value creation would have been meaningful. It is the kind of inefficiency that, frustratingly, does not change the thesis - but it does mean shareholders have to rely on earnings growth rather than capital allocation savvy for returns.

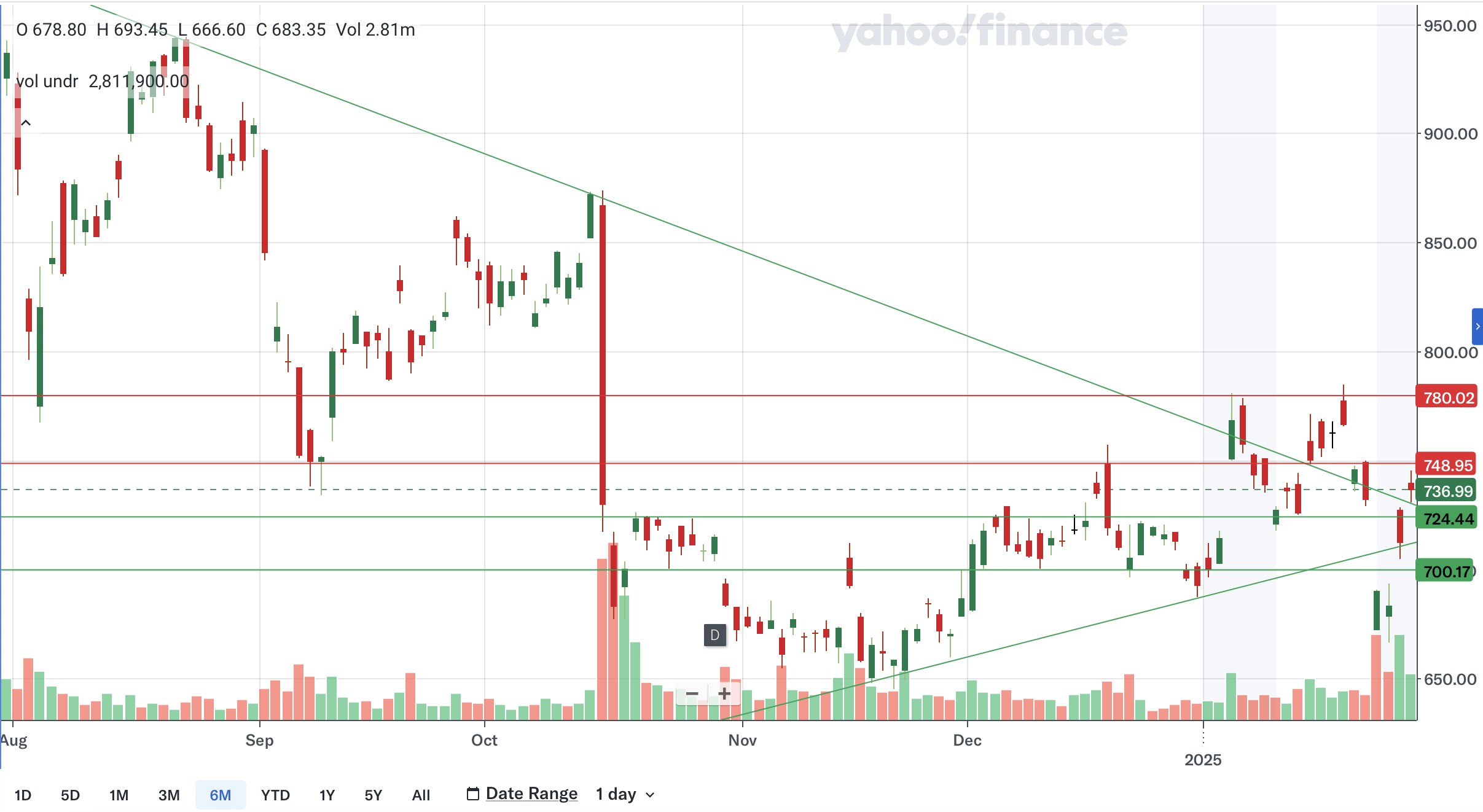

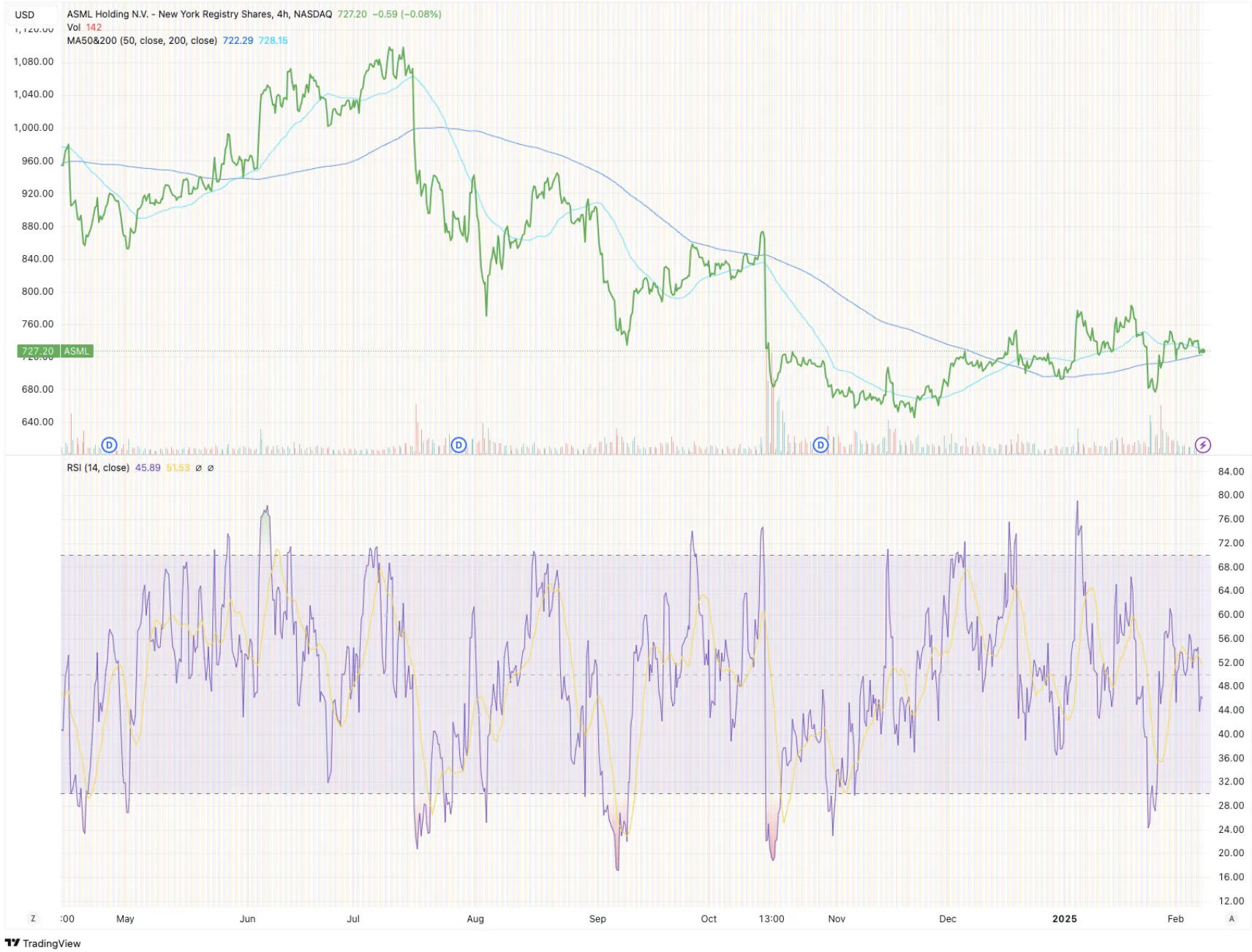

The technical setup, while secondary to the fundamental thesis, provides useful context for entry timing. ASML broke its longer-term downtrend from August 2024 in late December and has established a nearer-term uptrend from November lows. The stock is currently trading in a range bounded by support at approximately $724-$725 and resistance at $748-$780.

The 50-day simple moving average sits at $712.70, now below the stock price - meaning the near-term trend is constructive. The 200-day SMA remains well above at $839.58, creating a death cross configuration from September. However, the gap between the two moving averages is closing, and a resolution of this divergence - particularly if the 50-day begins to curl upward - would represent a significant technical confirmation of the fundamental thesis.

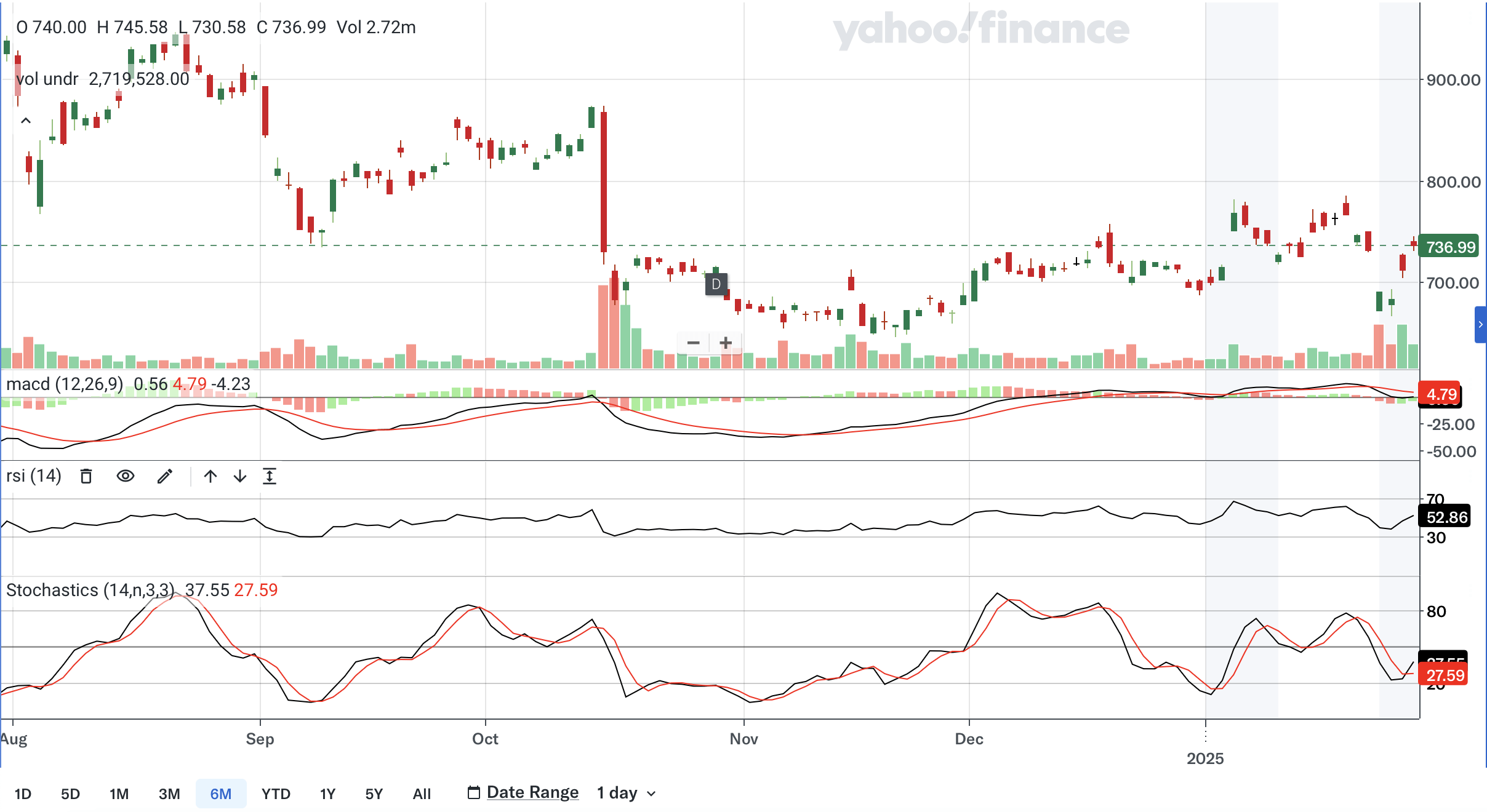

Momentum indicators are cautiously constructive. RSI sits at 52.86, having reclaimed the critical 50 level that separates bullish from bearish momentum. Stochastics show a %K bullish crossover with %D near the oversold 20 zone - a pattern historically associated with early-stage reversals. The MACD remains in bearish crossover territory, but the histogram is compressing, suggesting the bearish momentum is exhausting.

The Bollinger Band midline ($732.24) has been reclaimed, which is a confirmation of range-bound strength. The stock broke above this level after trading near the lower band ($681.48) during the DeepSeek selloff. The upper band at $783 represents the next upside target before the more significant $839 level (200-day SMA) comes into play.

The technical setup here combines four concurrent signals reinforcing the same directional bias: a broken downtrend, RSI reclaiming above 50, a stochastic bullish crossover, and a Bollinger Band midline reclaim. No single signal is decisive in isolation, but their simultaneous alignment - each confirming the others - is the type of configuration that historically precedes sustained moves in large-cap names when fundamental catalysts are present. The Q4 earnings beat and the approaching 2nm ramp provide that fundamental support.

No monopoly is without risk. The question is not whether ASML faces threats, but whether those threats are likely to materially impair the thesis within our 12+ month time horizon.

Further US/Dutch/Japanese restrictions could eliminate China revenue entirely. However, China is already normalizing to ~20% and is concentrated in mature DUV nodes, not leading-edge EUV.

If hyperscaler CapEx plateaus or declines, foundry orders could slow. Mitigant: $315B+ committed for 2025, and foundry capacity takes 2-3 years from order to production. ASML's backlog provides 5+ quarters of visibility.

Intel's foundry struggles could delay High-NA adoption. Mitigant: Third High-NA system shipped to non-Intel customer, broadening the customer base beyond a single risky buyer.

Chiplet architectures and hybrid bonding could reduce the number of EUV layers per product. Counter: advanced packaging still requires leading-edge lithography for each chiplet, and total wafer starts may increase as dies get smaller.

ASML will stop reporting quarterly bookings from 2026, replacing them with annual systems backlog. May increase speculation-driven volatility but does not change the underlying business.

In a severe downturn, P/E could compress to 20-25x. At 20x on 2026 EPS, the stock would trade near $600 - roughly 18% downside. This is the bear floor, not the expected outcome.

We present three paths forward, based on different assumptions about AI CapEx durability, 2nm ramp speed, China revenue trajectory, and multiple assignment.

AI CapEx stalls, 2nm ramp delays, China revenue drops below 15%, P/E compresses to 22-25x. Revenue at low end of 2025 guidance (EUR 30B). EPS ~$22. Downside: -12% to -19%.

AI CapEx grows as guided, 2nm ramps on schedule, China normalizes to 20%, P/E holds 29-32x on 2026-27 EPS ($29.66-$35.92). Revenue tracks midpoint-to-high end of guidance. Upside: +33% to +46%.

AI CapEx accelerates, High-NA adoption broadens rapidly, P/E re-rates to 33-36x on above-consensus EPS growth. Revenue at upper end of 2025 guidance (EUR 35B) with 2026 exceeding expectations. Upside: +56% to +69%.

The base case probability-weighted return is meaningfully positive. At a midpoint entry of $735, the base case target midpoint of $1,030 represents 40% upside over 12-18 months. The bear case floor of $600-$650 represents 12-19% downside. The risk-reward ratio on these parameters is approximately 1:2 to 1:3 - favorable for a monopoly compounder with a multi-year earnings growth trajectory.

Q1 guided at EUR 7.5-8.0B revenue with 52-53% gross margin. First confirmation of 2nm tool ordering patterns and TSMC N2 timeline updates.

CFO Dassen indicated "good order intake" expected in H1 2025 for 2026 EUV and DUV coverage. Strong orders would confirm 2026 as a growth year.

NXE:5200 (volume production tool) entering customer qualification. Successful qualification would trigger initial High-NA volume orders and confirm multi-customer adoption beyond Intel.

TSMC's 2nm node enters volume production. Next-gen AI accelerators (NVIDIA Blackwell successors, AMD MI-series) drive additional EUV demand. Memory HBM4 ramp adds incremental litho layers.

Gross margins begin expanding toward 56-60% CMD target as High-NA reaches volume and pricing power strengthens. Installed base revenue approaches EUR 8-9B, creating a visible recurring floor.

What makes the ASML case compelling is not any single data point but the convergence of independent analytical frameworks arriving at the same conclusion.

The fundamental case begins with the CapEx numbers. When five of the world's largest technology companies independently decide to spend $315 billion on AI infrastructure in a single year - up 40%+ from the prior year - and every dollar of that spending ultimately depends on chips that require ASML's machines, the demand signal is not speculative. It is committed capital.

The valuation case notes that ASML trades at its 13-year average P/E multiple while positioned for 20%+ EPS growth over the next three years. In a world where the S&P 500 trades at 21x and mega-cap tech at 30-40x, asking ASML to maintain a 29-32x multiple while earnings grow from $19.25 to $34+ is not a heroic assumption. The FAST Graphs model projects 16.47% total annual return through 2027 at today's entry price. P/S mean reversion alone implies 23%+ upside.

The technology case observes that ASML has four distinct growth layers - High-NA ramp, Low-NA productivity gains, DUV demand from mature nodes, and installed base revenue scaling - each providing independent revenue support. The EUV productivity-to-price ratio has improved 44% since 2015, strengthening customer ROI and willingness to pay.

The technical case, while least important, notes four concurrent signals simultaneously aligning: a broken downtrend, RSI reclaiming above 50, a stochastic bullish crossover, and a Bollinger Band midline reclaim. These are conditions that precede sustained moves in large-cap names when fundamentals provide support.

The order book case is perhaps the most concrete. EUR 36 billion in systems backlog, EUV already covered for 2025 midpoint, and CFO commentary explicitly pointing to 2026 as a growth year. When a company's own CFO tells you the next two years are growth years and backs it with a EUR 36 billion order book, the disconnect between that visibility and a stock trading at its long-term average multiple is the opportunity.

There are risks. China export controls could tighten further. AI spending could decelerate if the return on inference proves lower than expected. Intel's foundry ambitions could stall, delaying one source of High-NA demand. A severe market downturn could compress multiples to 20-25x, producing 12-19% downside from current levels.

But the asymmetry is what matters. Our downside scenario produces $600-$650 (12-19% loss). Our base case produces $980-$1,080 (33-46% gain). Our bull case produces $1,150-$1,250 (56-69% gain). On probability-weighted expected value, this is a position with a positive expectancy that is rare for a $300 billion market cap company with this level of forward visibility.

ASML does not need AI spending to grow forever. It needs it to remain elevated for 2-3 more years while the 2nm node ramps, High-NA matures, and installed base revenue compounds. The hyperscalers have committed the capital. The foundries have placed the orders. The backlog is visible. The only remaining question is whether the market will reprice the stock to reflect what the order book already says.

We believe it will.

Disclaimer: This analysis reflects the author's independent research opinion as of the publication date and is intended for educational and informational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results. Readers should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. The author may hold positions in the securities discussed. All data sourced from ASML earnings reports, company presentations, TIKR.com, FAST Graphs, Yahoo Finance, and publicly available analyst research. PolyMarkets Investment Strategies is not a registered investment advisor.