There is a particular kind of setup that I have learned to pay attention to over the years - the kind where the numbers look terrible, the headlines are hostile, and the analyst community is split right down the middle. That is where Tesla sits as I write this in early May 2024.

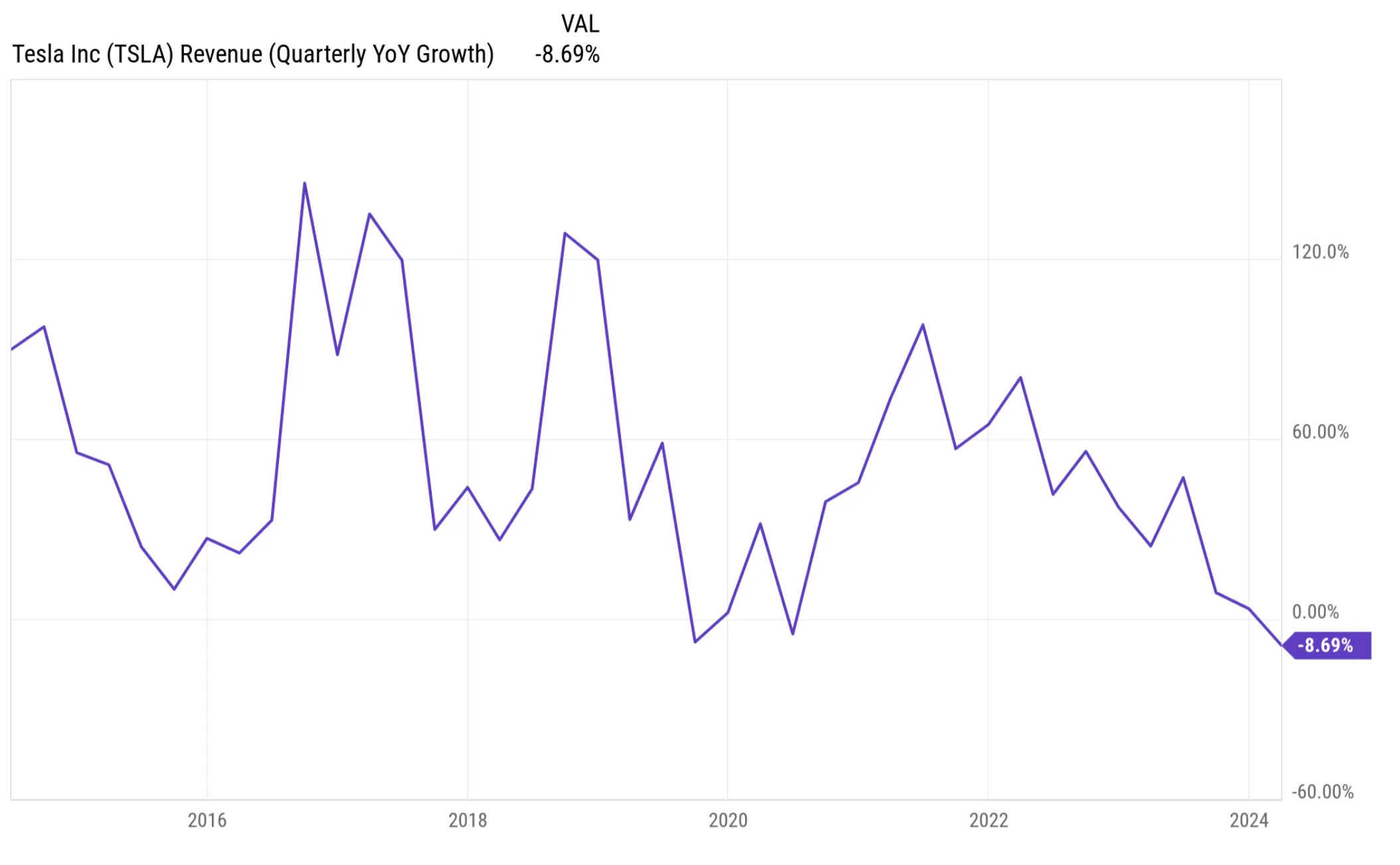

Q1 was objectively bad. Revenue declined 8.7% year-over-year - the first drop since the pandemic. Deliveries fell 8.5%. Free cash flow went negative for the steepest quarter in company history. The stock had shed 41% from its late-2023 highs before a sharp bounce on China FSD headlines and the August 8th Robotaxi unveil announcement. The bears are writing obituaries for the EV growth story.

And yet. When I read seven independent analyst frameworks back-to-back, listened to the full Q1 earnings call, and mapped the catalyst calendar for the next twelve months, what I found was not a company in decline. What I found was a structural inflection point hiding behind a cyclical trough. The question is not whether Tesla is having a bad quarter. It obviously is. The question is whether this bad quarter is the final chapter of a deteriorating narrative - or the darkest hour before a multi-catalyst recovery that the market has not yet priced.

I believe it is the latter. Here is why.

Business is non-linear. No company on earth grows revenue at a steady 15% or 25% in perpetuity - especially not one generating nearly $100 billion in annual sales. Tesla is undoubtedly going through a period of non-linearity right now, as most clearly communicated by its 8.5% decline in overall revenue, which followed a year of steadily decelerating growth. EV sales dropped from $18 billion to $16 billion in Q1 - a 13% decline in automotive dollar sales - and for the first time outside the pandemic, Tesla delivered fewer vehicles year-over-year in an absolute sense. In the U.S. alone, Tesla sold 21,443 fewer vehicles than Q1 2023. Free cash flow swung to negative $2.5 billion - the steepest negative quarter in company history and the first time cash flow turned red since Q2 2021.

In late 2020 and 2021, the common refrain from Tesla bulls was that 50% annualized revenue growth should be expected. The law of large numbers always made that unlikely once Tesla reached the scale it had achieved. Layer on the fastest rate-hiking cycle in 40 years - which made vehicle financing dramatically more expensive - and you have the context for this deceleration. This is not a Tesla-specific problem. It is an industry-wide compression. Nearly 80% of new car purchases in the U.S. are financed with debt, and JPMorgan’s Jamie Dimon has warned that rates could climb even higher. When the cost of a 60-month auto loan rises by 200+ basis points, it does not matter whether you are selling a Model Y or a RAV4 - demand gets pulled forward, then collapses.

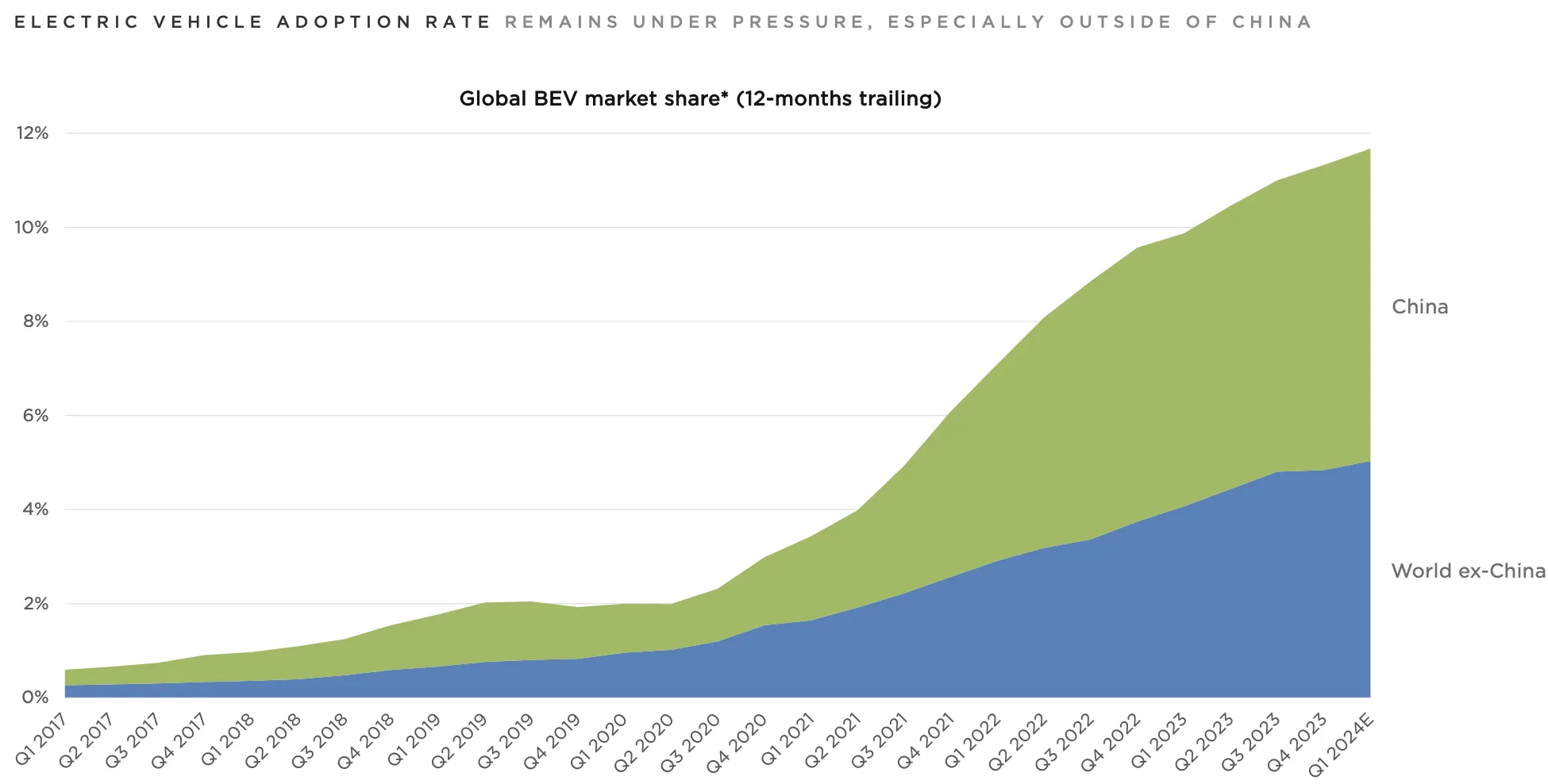

Ford’s EV sales growth has collapsed. BYD’s sales declined year-over-year. Even Toyota and Volkswagen are seeing deceleration. But here is the number that reveals this is cyclical, not structural: while Tesla lost those 21,443 units in the U.S., BMW, Hyundai, Ford, Rivian, and Mercedes-Benz added a combined 35,656 EV units in the same period. The pie is not shrinking - it is being redistributed during a temporary demand compression. The underlying trend - EVs moving from 12% of global car sales toward eventual dominance - has not changed. The pace has temporarily slowed because money became expensive.

What separates Tesla from its competitors in this downturn is how it is responding. While other automakers retreat - pulling back EV investment, cancelling models, reverting to plug-in hybrids - Tesla is investing through the cycle. The company announced a 10% headcount reduction (roughly 14,000 jobs) that will generate well over $1 billion in annualized savings, even as it accelerates spending on AI training compute, FSD development, and Megapack capacity. It sits on $27 billion in cash with virtually no debt. That is not the balance sheet of a company in distress. That is a war chest for a company playing offense while the rest of the industry plays defense.

“The EV adoption rate globally is under pressure and a lot of other auto manufacturers are pulling back on EVs and pursuing plug-in hybrids instead. We believe this is not the right strategy and electric vehicles will ultimately dominate the market.”

- Elon Musk, CEO, Q1 2024 Tesla Earnings Call

What matters to my thesis is that the non-linearity cuts both ways. If the decline was driven primarily by rates - and the evidence strongly suggests it was - then the re-acceleration, when it comes, could be equally non-linear. Companies that invest through cyclical troughs while competitors retreat tend to emerge with wider moats and faster growth on the other side. That is exactly what Tesla is doing right now.

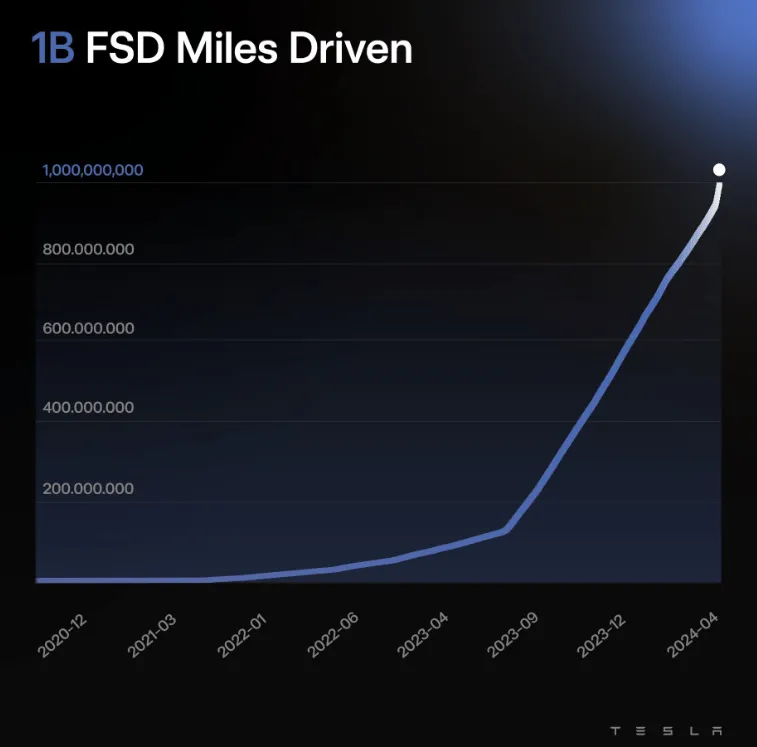

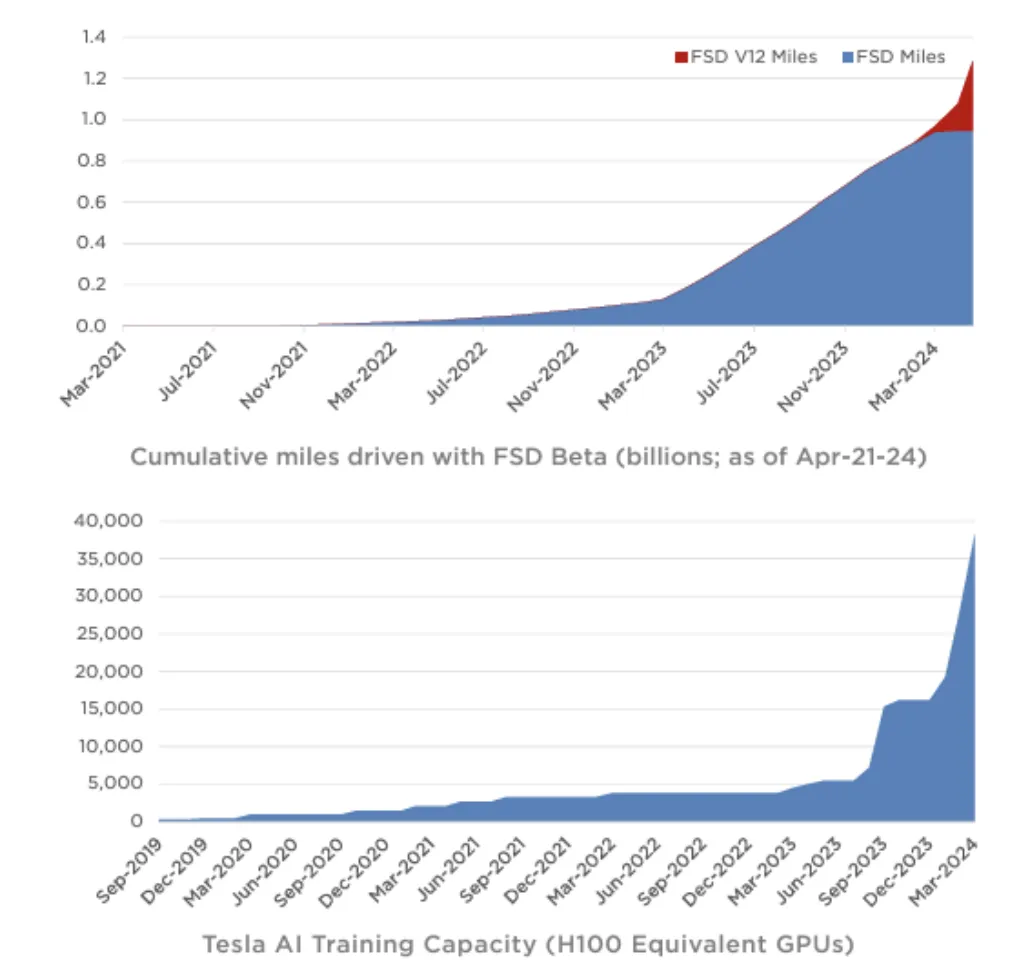

If there is one chart that captures the core of the Tesla bull thesis, it is this one. FSD cumulative miles driven have gone parabolic - surpassing 1 billion miles - and AI training compute has scaled from near-zero to 35,000 Nvidia H100 GPU equivalents, with plans to reach 85,000 by year-end.

FSD V12 represents a paradigm shift in approach. Tesla eliminated 300,000 lines of hand-coded safety rules and moved to an end-to-end neural network architecture - a system that learns entirely from real-world driving data rather than following pre-programmed instructions. As Ashok Elluswamy, Tesla’s Director of Autopilot Software, explained on the Q1 earnings call: the new architecture “is automatically improving without requiring much engineering interventions - it’s mostly learning on its own based on data.” The more miles driven, the more training data feeds the flywheel. This is the same kind of compounding network effect that makes Google Search nearly impossible to compete with: every query makes it smarter.

The deployment numbers underscore the scale advantage. FSD V12 has been pushed out to approximately 1.8 million vehicles, with roughly half actively using it - a percentage that increases every week. Tesla has reduced the FSD subscription price to $99 per month to drive adoption, prioritizing data collection over near-term monetization. Meanwhile, AI training compute has more than doubled sequentially in Q1, and the team has identified scaling laws - model size, data volume, compute, and architecture - that allow them to predict future performance. This is not speculative. It is systematic.

“As our fleet grows - 7 million, 9 million, eventually tens of millions of cars worldwide - with a constant feedback loop, every time something goes wrong, that gets added to the training data. You get this training flywheel in the same way that Google Search has a flywheel. It’s very difficult to compete with Google because people are constantly doing searches and clicking, and Google is getting that feedback loop.”

- Elon Musk, CEO, Q1 2024 Tesla Earnings CallThe bears rightfully point out that FSD remains at Level 2 on the driver assistance scale - requiring constant human supervision. V12 has had documented near-misses on video. The shift to a pure neural network, while elegant, means those 300,000 lines of safety code are gone - replaced by learned behavior that regulators may view with justified scepticism. There was a 2-million-vehicle recall for Autopilot safety concerns. These are legitimate issues. But they miss the structural picture: no other automaker on earth has over 1 million vehicles on the road collecting real-time driving data for AI training. Waymo operates a few thousand vehicles in geofenced cities with a vastly different hardware approach - a sensor array bristling with LiDAR, radar, HD mapping systems, and layers of redundant safety code. It is a brilliant system, but it is inherently difficult to scale. Waymo was valued at $30 billion in its Series E round. Tesla trades at roughly $500 billion. The market is telling you something about the difference between a geofenced taxi service and a platform that could enable autonomy for tens of millions of vehicles worldwide.

Musk made this explicit on the earnings call: “If somebody doesn’t believe Tesla is going to solve autonomy, I think they should not be an investor in the company.” He went further with an analogy that I found compelling: “In my view, this will be much like elevators. Elevators used to be operated by a guy with a relay switch. We just get in an elevator and press a button - we don’t think about it.” The implication is that autonomous driving will become so routine, so invisible, that the idea of manually controlling a two-ton vehicle at highway speed will seem as archaic as hiring a person to operate a lift. And here is the platform play that most investors miss: Tesla is already in licensing conversations with at least one major automaker for FSD technology. As Musk put it, borrowing from the Nokia playbook: “All cars will need to be smart cars, or you will not sell. License it or nobody will buy your car.” If FSD becomes the Android of autonomous driving - licensed across manufacturers - the revenue model transcends Tesla’s own vehicle sales entirely.

The unit economics of FSD success are staggering. At just 50 million subscribers at $1,200/year by 2035 - a fraction of the global vehicle fleet - FSD alone would generate $60 billion in high-margin recurring revenue. At 35% free cash flow margins and a 25x multiple, that is a standalone $735 billion business. And that is before licensing. FSD is not a nice-to-have. It is the thesis.

On April 28th, Elon Musk met with China’s No. 2 official in Beijing. Within days, China’s Association of Automotive Manufacturers confirmed that Tesla’s Model 3 and Model Y had passed local data security requirements. Tesla reached an agreement with Baidu for navigation and mapping data. The path to FSD rollout in the world’s largest EV market - which accounts for nearly 60% of global EV sales - is now open.

This matters enormously for three reasons. First, Tesla has over 2 million cars already operating in China. That is 2 million potential FSD subscribers and 2 million vehicles that can feed training data into Tesla’s neural network. If even a fraction subscribe at $100/month, the revenue impact is measured in billions.

Second, China FSD data would dramatically accelerate AI training. Chinese driving conditions - dense urban environments, aggressive traffic patterns, mixed-use roads - represent a data goldmine that would make FSD measurably better everywhere, not just in China. One of the most underappreciated features of FSD V12’s end-to-end neural network is its portability: because the system learns to drive like a human, it adapts to local conditions without market-specific reengineering. The analogy Musk used on the earnings call was a human driver landing in a foreign country - the rules may differ, but the fundamental skill transfers. The only local adjustments needed are regulatory specifics, such as China’s strict prohibition on crossing solid lane lines (a heavy fine, versus a mere recommendation in the U.S.). Tesla has been preparing for this since 2021, when it established a dedicated local data center in Shanghai to comply with China’s data sovereignty requirements - a move that now positions it ahead of every Western competitor on regulatory readiness.

Third, regulatory approval opens the door to FSD licensing to local manufacturers. With at least 10 major domestic EV makers competing in China - BYD, XPeng, Li Auto, Huawei, Xiaomi, and others, all investing aggressively in autonomous driving - Tesla could become the autonomous driving operating system of the Chinese EV market. That is a platform play, not a hardware play. Canalys forecasts the global EV market will grow 27.1% in 2024, reaching 17.5 million units. China represents nearly 60% of that total. Being the platform standard in a market of that scale changes the revenue model fundamentally.

The stock surged 15% on the China news alone, and the rally continued through subsequent sessions. The market is telling us this catalyst matters. The question is whether the full revenue potential - FSD subscriptions from a growing Chinese customer base, accelerated AI training, licensing optionality, and billions of miles of the most complex driving data on the planet - is properly reflected in the current price. My view is that it is not. Giga Shanghai delivered 947,000 vehicles in 2023 alone, and if even a modest fraction of the 2M+ installed base subscribes to FSD at $100/month, the annualized revenue impact is $2.4 billion - from a single geography, with near-100% gross margins.

The Reuters report that Tesla had scrapped the mass-market Model 2 sent the stock tumbling. Musk promptly responded on X: “Reuters is lying.” The truth, as it often does with Tesla, likely sits in between - and the nuance is actually bullish.

The original Model 2 concept was a $25,000 entry-level EV. In a 2016 world where the average new car cost $34,077, that made strategic sense. But the automotive market has shifted dramatically. In 2024, the average new car in America sells for $48,000 - a 41% cumulative increase, outpacing the 30% general inflation over the same period. A $25,000 EV would destroy margins without delivering meaningfully greater market penetration than a ~$30,000 version. What appears to be happening is a re-scoped Model 2: a stripped-down variant of the Model 3, priced just below $30,000, built on the existing platform using Tesla’s new “unboxed manufacturing” approach - building all major components separately before assembling in one final step, rather than the traditional sequential assembly line. Tesla’s own Investor Day projections suggest next-generation vehicle COGS could decline by 50% versus the current Model 3/Y - implying roughly $20,000 of production cost, with about one-third of the savings coming from unboxed manufacturing alone.

This is smarter for shareholders than a clean-sheet $25K platform. It avoids billions in new platform development costs, preserves margin structure, and still obliterates the competition on price. Consider what a consumer shopping for a ~$30,000 EV actually encounters today: the Polestar 2 starts at $51,000 - only $1,000 less than a Model 3 Performance. The Rivian R2 starts at $45,000 - nearly $7,000 more than a base Model 3. The Hyundai Ioniq 5 commands a significant premium over comparable Tesla models. And every legacy ICE competitor in the mass-market sweet spot - Honda HR-V, Honda Accord, Toyota Camry, Toyota RAV4, Hyundai Elantra, Chevrolet Bolt, VW Taos - suddenly faces an EV alternative from the most recognized brand in electric mobility. As one analyst in our research set put it bluntly: “Most consumers in the market for an EV today simply have no alternative to buying a Tesla.” A $30,000 Model 2 does not just widen Tesla’s addressable market. It practically eliminates the remaining excuses for not switching to electric. I would not be surprised to see two variants - a sedan and a small SUV or crossover - mirroring the Model 3/Y strategy that has proven so effective.

What the bears dismiss as “just another car” is actually category strategy. Tesla has category vision - a trait shared by Apple, Amazon, and Procter & Gamble. Instead of optimizing for quarterly margins, Tesla uses pricing to grow the entire EV category, knowing that as the market leader with 50%+ U.S. share, it disproportionately benefits from category expansion. When P&G launched laundry pods in 2011, the laundry detergent category grew 4x and P&G grew 5x - faster than the market it created. Apple did not compete in the smartphone market; it created it. The tablet market was negligible before the iPad. Tesla is running the same playbook: price aggressively, grow the category, and let your dominant market share compound the returns.

The Amazon parallel is particularly instructive. In the early 2010s, Amazon was pilloried by analysts for its razor-thin margins and apparent indifference to profitability. A widely cited Seeking Alpha article from 2013 questioned whether Amazon could ever justify its valuation. The answer, of course, was that Amazon was not optimizing for quarterly earnings - it was investing to own the e-commerce category, knowing that scale and infrastructure advantages would eventually produce extraordinary returns. Tesla is making the same bet. The price cuts that alarm short-term investors are not desperate inventory clearance - they are the strategic equivalent of Amazon’s free shipping: a category-expanding investment that looks like a cost today and an insurmountable moat tomorrow. The plan, as with Amazon, is to shift focus to margins once the EV category reaches the “late majority” phase of adoption.

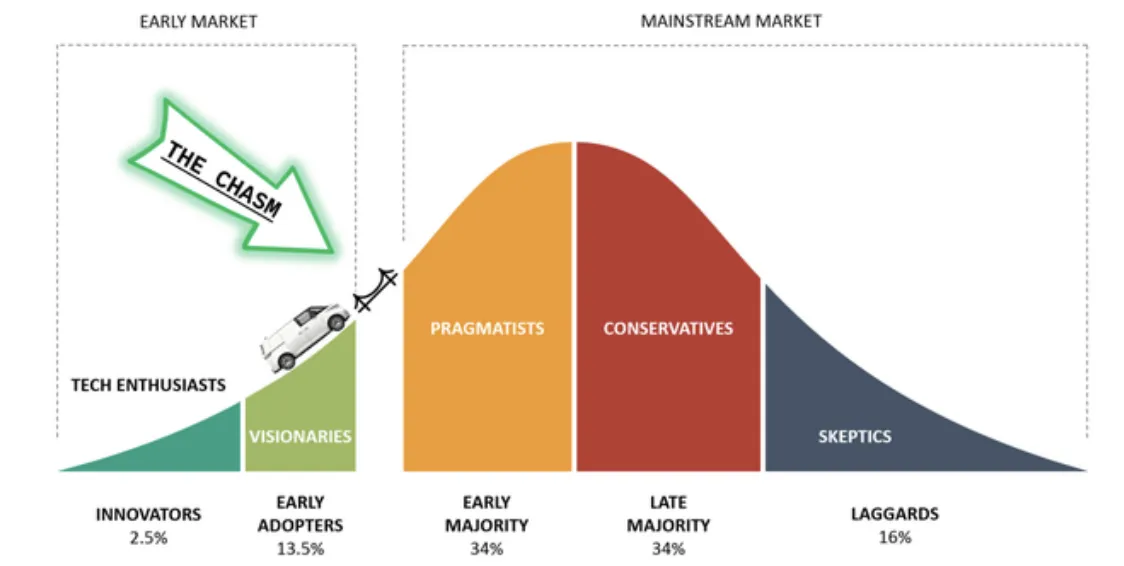

The Model 2, in whatever form it takes, is the vehicle that pushes EVs from “early adopters” across the chasm to “early majority.” That transition - from ~12% to 35%+ of new car sales - is where the hockey-stick growth lives. Tesla is positioning to own that transition, and the August 8th event should provide the first concrete details. A $299/month Model 3 lease is already available. A $30,000 Model 2 purchase changes the math entirely for the median American household.

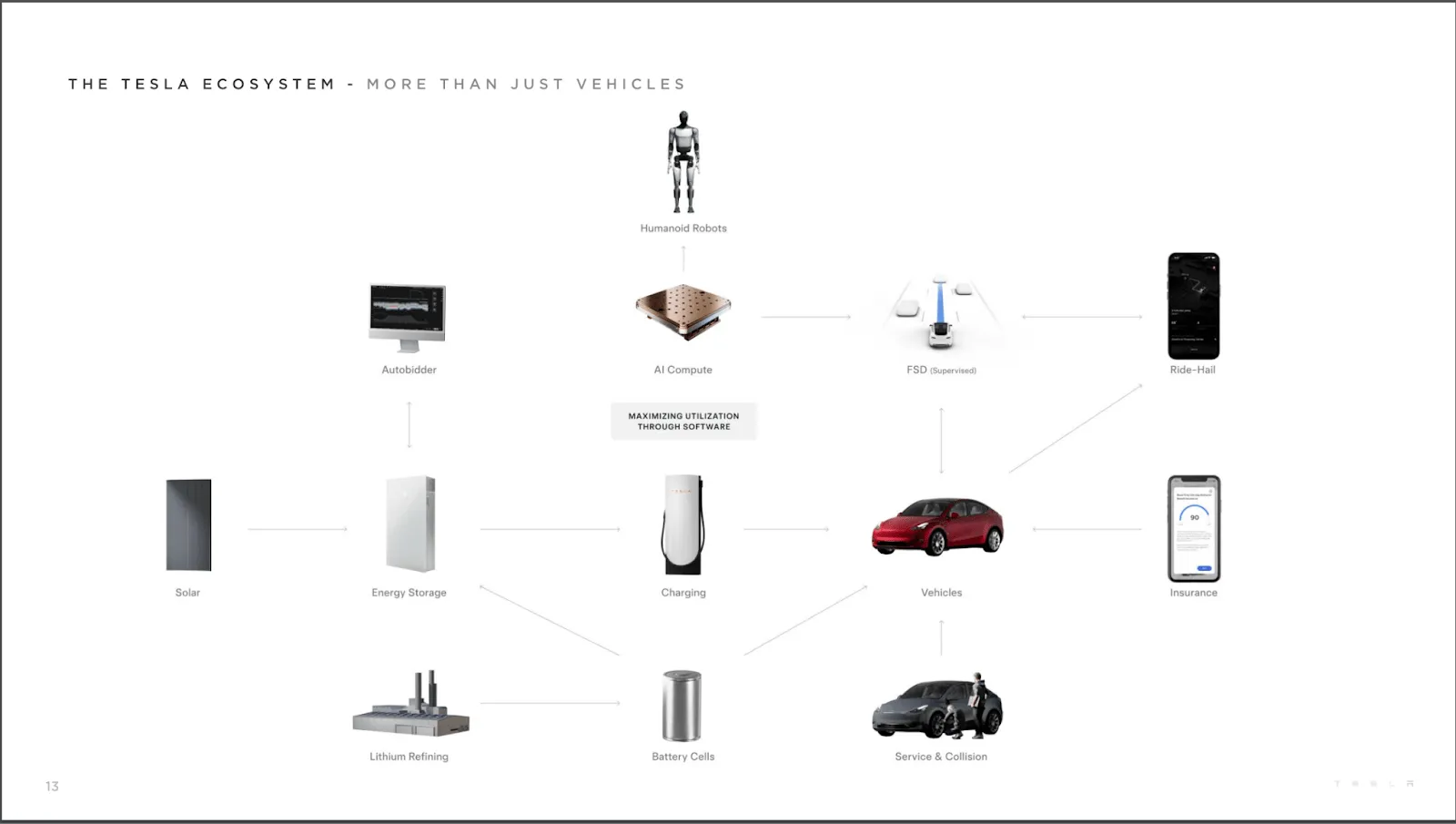

The market prices Tesla primarily as an automaker. That framing misses at least three businesses that could each independently justify significant enterprise value.

Tesla Energy

FSD Subscriptions

Supercharger Network

Tesla Energy is the most under-appreciated business inside Tesla. As EV adoption climbs toward 100%, demand for electricity through the residential grid will surge, creating massive need for stationary storage. Goldman Sachs forecasts China alone will need 520GW of energy storage by 2030 - a 70-fold increase from 2021, with up to 410GW coming from batteries. Tesla’s Megapack business is not just promising - it is already executing. Energy storage deployments hit an all-time high in Q1, driving the segment to record margins of 24.6%. Tesla has commissioned a second general assembly line at its Lathrop facility, doubling the exit rate from 20 GWh/year to 40 GWh/year by year-end. Order visibility stretches 12–24 months ahead. CFO Vaibhav Taneja expects energy deployments to grow at least 75% from 2023 levels this year. As one analyst in our research set framed it: “Tesla’s AWS is its Megapack business” - a comparison to how Amazon Web Services started as an internal infrastructure tool and became the most profitable division of the company.

At scale - 1,500 GWh/year of deployments at current unit economics ($550/kWh) - that is $825 billion in ~25% gross margin revenue. (Note: this $825B figure is a long-range illustrative scenario - not a 5- or 10-year forecast. It assumes Tesla Energy deploys 1,500 GWh annually, which is approximately 37x the current exit run-rate of roughly 40 GWh. At the current trajectory doubling every 1-2 years, reaching 1,500 GWh would take roughly 10-15 years of sustained execution. We include it to show what the optionality is worth at scale - not as a near-term revenue line. The near-term Energy thesis rests on the 20-40 GWh trajectory at 24-25% gross margins, which is already a compelling standalone business.) Using 15% FCF margins and a 25x multiple, Tesla Energy alone could trade at ~$2.5 trillion in market cap by the 2030s. The bears push back hard on this number. The most bearish sum-of-parts analysis in our research set values Tesla Energy at just $12 billion, using comparable P/S multiples from the solar/storage peer group: Sunrun at 1.14x, SunPower at 0.28x, Enphase at 8.5x, Generac at 2x, SolarEdge at 2.3x, and Sunnova at 0.8x sales. Against Tesla Energy’s $6.1 billion in revenue, those multiples yield a range of $1.7B to $52B depending on which peer you choose. The $12 billion midpoint is a legitimate bear-case figure. But it fundamentally misunderstands the business: Tesla Energy is a vertically integrated manufacturing + deployment operation growing at 75%+ per year with record margins, while most of those comparables are contracting or stagnating. Applying a peer multiple from SunPower - a company in terminal decline - to the fastest-growing utility-scale storage business on earth is analytically lazy.

Beyond Energy, the ecosystem includes several other businesses that the market barely acknowledges. The Supercharger Network is the only EV charging infrastructure at global scale, and the adoption of Tesla’s NACS connector as the North American standard means even competitors’ vehicles will funnel revenue to Tesla’s network. Optimus, Tesla’s humanoid robot, is early-stage but drew an extraordinary claim from Musk on the Q1 call: “I think Optimus will be more valuable than everything else combined. Because if you’ve got a sentient humanoid robot that is able to navigate reality and do tasks at request, there is no meaningful limit to the size of the economy.” Tesla expects limited Optimus production in its own factories before year-end, with external sales potentially beginning in late 2025. Cybertruck has ramped to 1,000 units per week within just four to five months of starting production - an impressive trajectory for a vehicle as mechanically complex as any Tesla has built. Pickup trucks have been America’s bestselling vehicle segment for over four decades; Tesla now has a foothold. The Tesla Semi has broken ground on a factory in Reno, with first vehicles planned for late 2025 and external customer deliveries in 2026.

And then there is the most speculative - but potentially transformative - layer of the ecosystem: distributed inference compute. On the earnings call, Musk described a vision where millions of Tesla vehicles, each equipped with a kilowatt of onboard compute, could run distributed AI workloads when parked - turning an idle fleet into a massive neural network. “If you get to 100 million vehicles with a kilowatt of useable compute, you could have on the order of 100 gigawatts of useful compute - which might be more than any company.” The vehicles already have built-in liquid cooling for their inference chips, and the power infrastructure exists in every garage. It is audacious, it is years away, and it may never happen. But if it does, it makes every Tesla sold a node in the world’s largest distributed computing network.

Combined, just FSD and Energy could create a $3 trillion business by the 2030s. Tesla currently trades at approximately $500 billion in enterprise value. Even if you assign a 50% probability to these scenarios materializing at half the projected scale, the implied upside from current levels is significant. The current price essentially gives you the auto business at a discount and the rest of the ecosystem for free.

I have read the strongest version of the bear case carefully. It deserves honest engagement. A sum-of-parts DCF from the most bearish analyst in our research set arrives at a fair value of $85 per share - roughly $272 billion total: $230 billion for the auto business (assuming $43,500 ASP, 500,000 units/year growth, and a 15% discount rate), $30 billion for FSD licensing (benchmarked to Waymo’s Series E valuation), and just $12 billion for the entire Energy segment. The bull cases range from $243 to $260 in 12-month targets, with the most optimistic framework pointing to $3 trillion in long-term enterprise value from FSD and Energy alone. The gap between $85 and $3,000+ per implied share is extraordinary - and understanding both sides is essential to sizing the position correctly.

The Prosecution

- EV market is smaller than hyped - US BEV sales nearly flat YoY in 2023; Tesla lost 21,443 units while five competitors added 35,656; market may be approaching a ceiling, not a floor

- DCF says overvalued at any reasonable discount rate - Even with generous 500K unit/yr growth and $43,500 ASP held flat, fair value is $230B; forward P/E of ~70x is the most expensive Magnificent Seven name while 80% of revenue is auto sales

- FSD is stuck at Level 2 with rising regulatory risk - V12 eliminated 300K lines of safety code in favor of a pure neural network; documented near-misses on video; 2M-vehicle Autopilot recall; no clear path to Level 3 certification

- Optimus lags every robotics competitor - Gen-2 demos show egg-handling and color-sorting; Boston Dynamics (acquired for $1.1B) has decades of physical prowess; da Vinci surgical robots perform actual operations; OpenAI ($80B) and Figure ($2.6B, backed by Bezos) have genuine AI brains; Musk is building Tesla’s AI brain at xAI, not at Tesla

- Musk attention risk and xAI conflict - CEO of Tesla, SpaceX, and X simultaneously; compensation voided by Delaware court; demands 25% voting control before fully committing to AI at Tesla; developing Grok/xAI separately creates potential conflict of interest

- Battery tech is not a moat - 4680 cells at 272–296 Wh/kg have disappointed; BMW Gen6 promises 30% better range, charging, and cost; Tesla still outsources solar panels (Q Cells) and batteries (Panasonic, LG, CATL, BYD)

The Defense

- Cyclical, not secular - Rate hikes suppressed all auto demand; 80% of car purchases are financed; EVs still only 12% of global sales with massive runway to 100%; competitors gaining share proves the category is growing, not dying

- DCF misses the entire optionality stack - Sum-of-parts ignoring FSD/Energy/Supercharger/Optimus/Compute = pricing Tesla as a 2019 automaker; FSD alone at 50M subscribers = $735B standalone business; Energy at scale = $2.5T

- 1B+ miles is an unassailable data moat - Waymo’s $30B valuation with thousands of geofenced vehicles vs. Tesla’s 1M+ FSD-equipped fleet; parabolic curve accelerating; already in licensing talks with a major automaker; Nokia analogy: license it or nobody buys your car. The Nokia parallel cuts both ways - Nokia was the disrupted, not the disruptor. Tesla’s role in this analogy depends entirely on whether it is building the platform that others integrate into, or whether it becomes one of many hardware manufacturers running a dominant third-party OS. The bull case rests on FSD as the iPhone - the proprietary software stack that defines the category. The bear case, frankly, is that BYD or a Chinese-derived autonomy stack becomes the Android of autonomous driving, leaving Tesla as a premium hardware maker without platform economics. This risk is real and worth naming - which is precisely why FSD’s technical leadership and the data moat described above are so critical to monitor.

- Category vision, not quarterly thinking - Amazon was “unprofitable” for a decade and analysts mocked the valuation; P&G grew 5x when its category grew 4x; Tesla’s price cuts are the EV equivalent of Amazon’s free shipping - a cost today, a moat tomorrow

- Musk is “betting the house” on FSD - Redirecting company focus to AI/robotics; spending hours weekly designing Austin assembly line; Walter Isaacson documented the obsessive hands-on approach; Robotaxi/Cybercab Airbnb+Uber model could 5x vehicle utilization

- Lowest valuation in 5 years with $27B cash - Near-lowest P/E in half a decade; virtually no debt; $1B+ in annual cost savings from restructuring; buying the most promising tech platform of the decade at near-record discount

My assessment: the bear case accurately describes the present. The bull case accurately describes the trajectory. Both sides agree on certain uncomfortable truths: the forward P/E is extreme, robotaxis are not a near-term catalyst, and FSD remains Level 2. But the key disagreement is whether Tesla’s price cuts represent desperation (bears see unsold inventory in a dying market) or strategy (bulls see category expansion from a 50%+ market share leader). The same data, interpreted through different time horizons, produces opposite conclusions.

If you are a quarters-focused investor, Tesla looks terrible. If you have a 12–24 month horizon and can tolerate the volatility, the asymmetry between what the market is pricing (a struggling automaker at ~$500B) and what Tesla is becoming (an AI/Energy/Autonomy platform with a credible path to $3T+) creates genuine opportunity. Musk’s vision for the Robotaxi platform - “some combination of Airbnb and Uber, where there will be cars that Tesla owns and operates in the fleet, and cars owned by the end user” - would transform a vehicle with 10 hours of weekly use into one with 50% utilization at the same cost. That is a 5x productivity gain on the most expensive consumer asset most people own. This is fundamentally a bet on FSD execution, with Energy as a powerful secondary catalyst and a category-leading auto business as the floor.

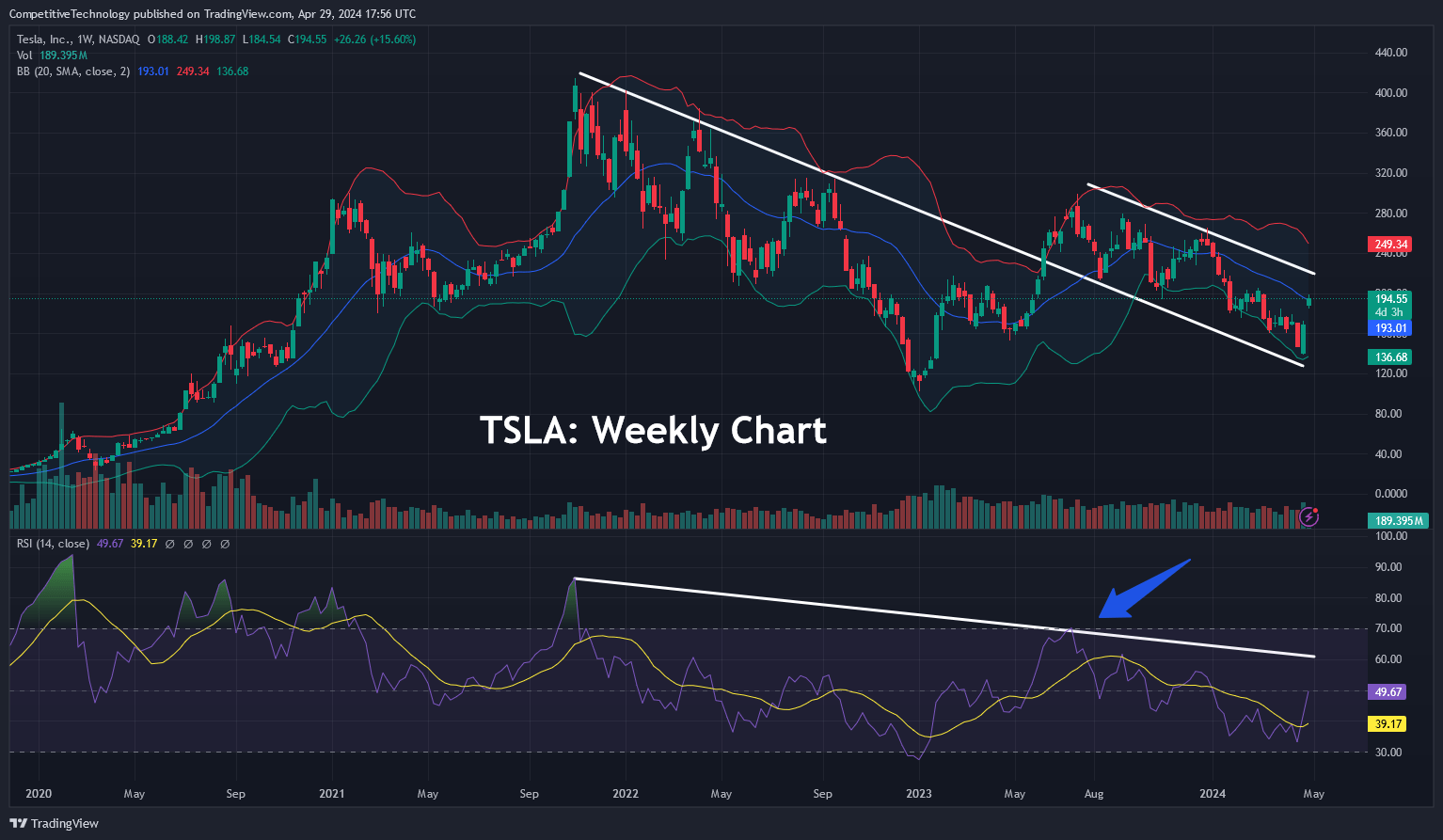

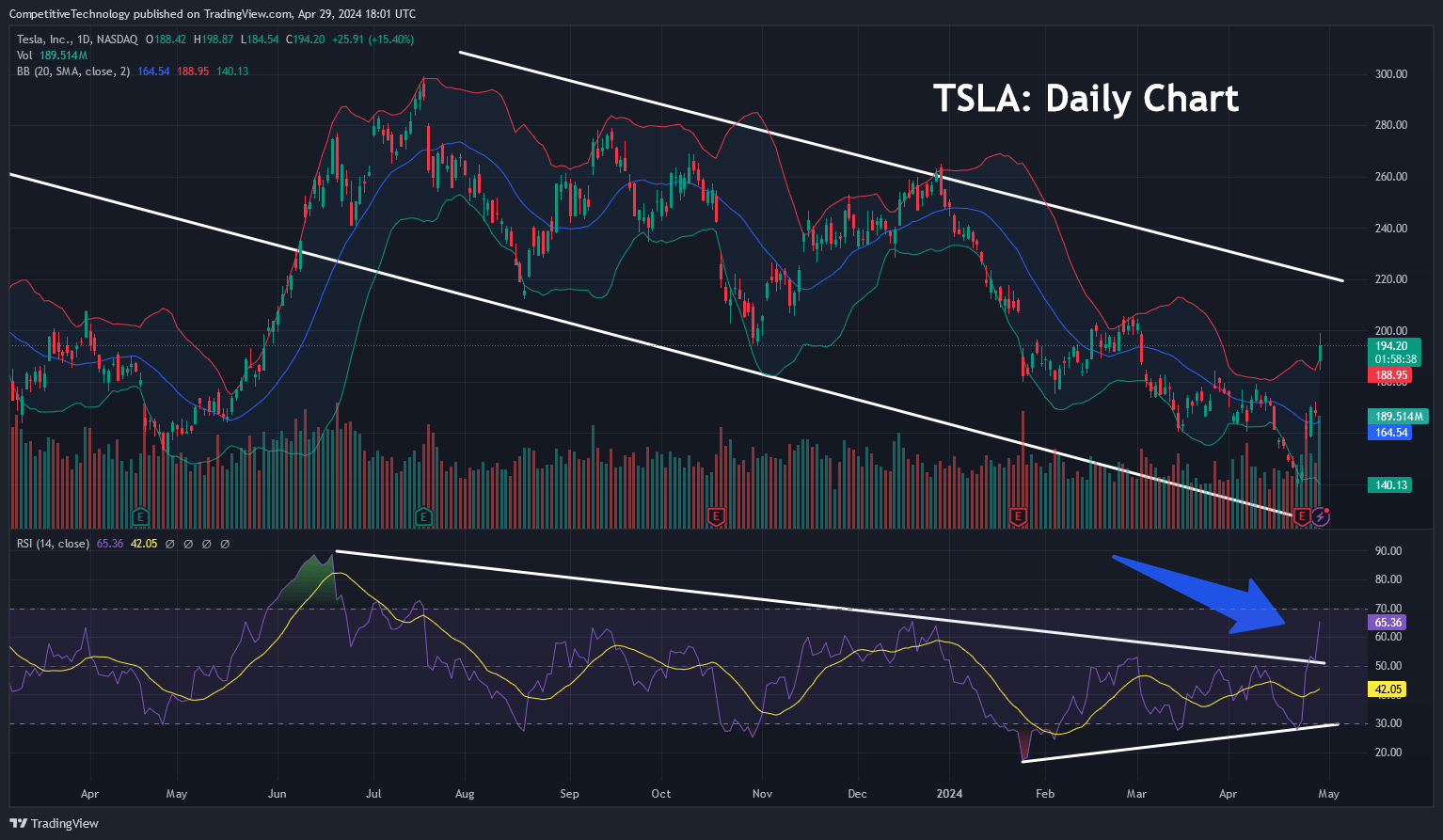

The technical picture aligns with the fundamental thesis. TSLA has been in a downtrend since the November 2021 all-time high of $414.50, but the dominant downtrend line was already broken in June 2023. What followed was a secondary, higher-level downtrend channel - and recent price action is now testing the upper boundary of that channel.

On the weekly timeframe, RSI is turning forcefully higher from deeply oversold readings - still below the midpoint, meaning significant room to run before becoming overbought. The daily chart already shows a bullish RSI breakout. These are the kinds of multi-timeframe momentum confirmations that tend to precede sustained moves.

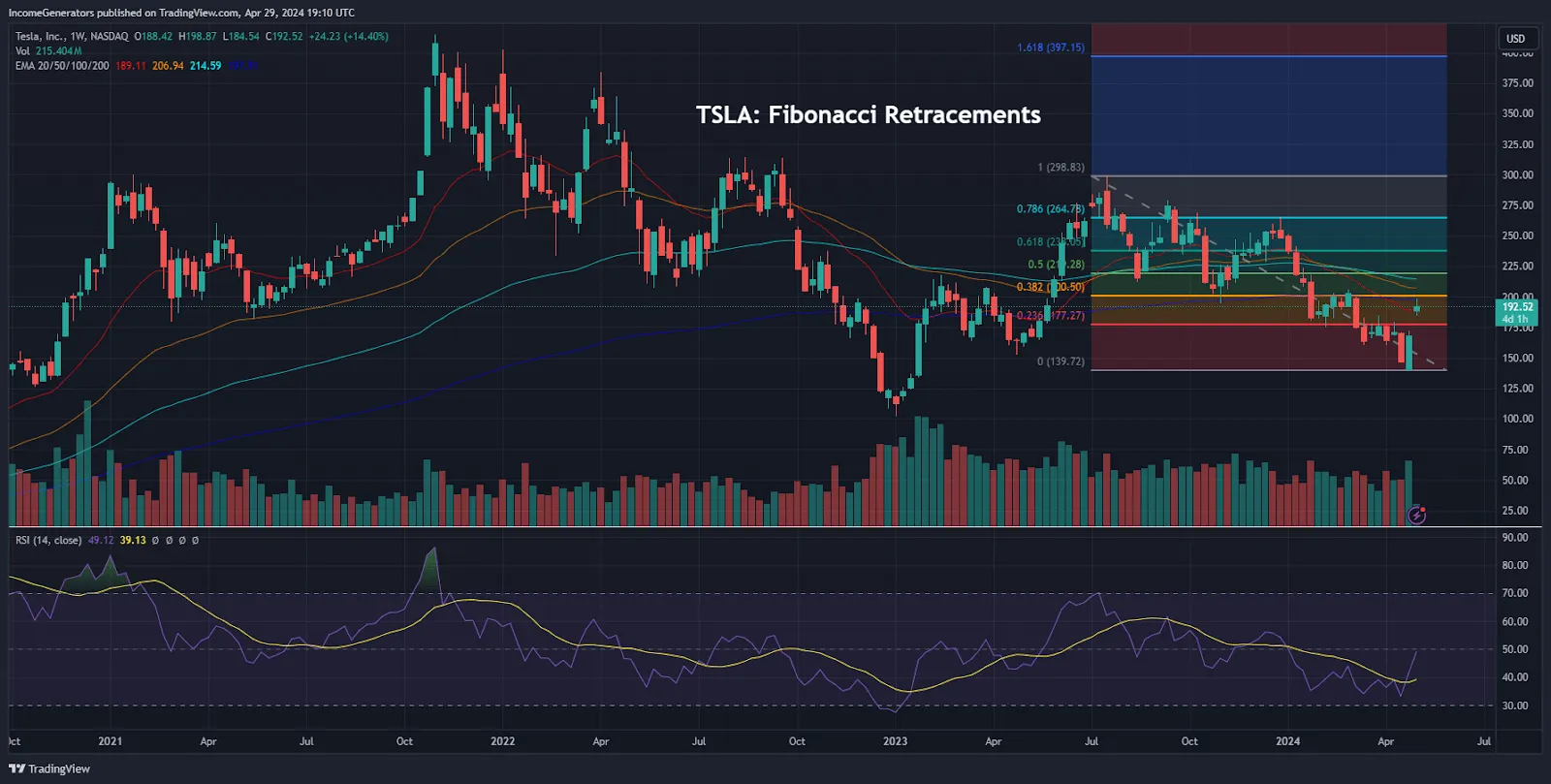

The Fibonacci retracement zones from the $299 to $140 decline map our roadmap: 38.2% retracement at $200, 50% at $218, 61.8% at $238, and the 78.6% retracement at $265 - which aligns almost exactly with the December 2023 rejection high of $265.13. Most weekly moving averages sit below the 50% retracement, so a clean break above $218 would likely propel prices to the upper Fibonacci targets relatively quickly. Support holds at $158 (scenario entry zone floor), with the critical stop-loss level below $140.

◆ Bear Case

◆ Base Case

◆ Bull Case

I am positioning for the base-to-bull range. The scenario entry zone of $155–$165 provides a margin of safety relative to the base case and significant upside to the bull case. The risk/reward from mid-entry ($160) to the target zone ($270–$290) is approximately 1:6 (risk of $20 to the $140 stop-loss, against $120 of upside to the $280 midpoint of the target zone), with the stop-loss at ~$140 limiting downside to roughly 12–15%.

Tesla is not a low-risk position. The beta is 1.6–1.9, making it one of the most volatile large-cap names in existence. The thesis depends on execution across multiple fronts simultaneously. I size accordingly. What follows is an honest accounting of what could break the thesis.

The following scenarios reflect the author’s personal analysis and are not investment recommendations. See our full disclaimer.

The hardest positions to take are always the ones where the headlines are worst but the setup is best. I have been doing this long enough to recognize the pattern: consensus bearishness, cyclical headwinds masking structural improvement, a catalyst calendar loaded with binary events, and a valuation at multi-year lows. That is the Tesla I see in May 2024.

This is not a comfortable position. Tesla’s beta guarantees volatility. The August 8th event is a genuine coin-flip between thesis validation and a painful drawdown. FSD could stagnate. Rates could stay elevated. China could disappoint. The Optimus timeline could slip. Musk’s attention could fracture further between Tesla, SpaceX, X, and xAI. I am sizing the position to survive all of those outcomes while capturing the asymmetric upside if even two or three catalysts deliver.

What gives me conviction is the convergence. I have read seven independent analyst frameworks - spanning the full spectrum from a bearish sum-of-parts at $85 to a bull case projecting $3 trillion in enterprise value - and the one consistent thread across all of them is that Tesla at current levels does not adequately reflect the optionality embedded in this company. The bear analysts value the auto business at $230 billion using generous assumptions and dismiss FSD, Energy, Optimus, and the Supercharger network as speculative noise. The bull analysts see a company that is not just an automaker but a vertically integrated AI, energy, and transportation platform with a data moat that no competitor can replicate, sitting on $27 billion in cash with virtually no debt, cutting costs by over $1 billion annually, growing its Energy business at 75%+ with record margins, deployed to 1.8 million FSD vehicles, in licensing conversations with major automakers, and trading at its lowest valuation in five years. The distance between these two narratives is where the opportunity lives.

“Really, the way to think of Tesla is almost entirely in terms of solving autonomy and being able to turn on that autonomy for a gigantic fleet. And I think it might be the biggest asset value appreciation in history when that day happens.”

- Elon Musk, CEO, Q1 2024 Tesla Earnings CallHere is how I synthesize the seven frameworks into a single thesis. The non-linearity framework (Article 5) tells us the business cycle is temporary and Tesla is at its most compelling in five years. The FSD framework (Articles 2, 6) tells us the billion-mile data moat and parabolic mileage curve are real, measurable, and accelerating. The China framework (Articles 4, 7) tells us the world’s largest EV market just opened its doors to FSD, with 2 million cars ready to collect data and subscribe. The category vision framework (Article 3) tells us the price cuts are not desperation but strategy - the same playbook that made Amazon and P&G category kings. The bear framework (Article 1) tells us what the floor looks like: $85 per share, $272 billion, if everything beyond the auto business fails to materialize. And the earnings call tells us, in Musk’s own words, that he is betting the company on autonomy and believes it will produce “the biggest asset value appreciation in history.”

Musk offered another line on the Q1 call that stayed with me: “In the future, gasoline cars that are not autonomous will be like riding a horse and using a flip phone.” It is the kind of statement that sounds absurd in the context of a quarter where revenue declined 8.7% and free cash flow went negative. But zoom out. In 2007, Nokia sold more phones than anyone on earth and the iPhone was dismissed as a toy. By 2012, Nokia was effectively dead. The transition from “dominant incumbent” to “irrelevant” happened in five years, and it happened because a new platform - one that combined hardware, software, and an ecosystem - made the old one obsolete. Tesla is building that platform for transportation. The auto business is the hardware. FSD is the software. Energy, Superchargers, and the fleet compute network are the ecosystem. The question for investors is not whether the transition will happen - it is whether it will happen on Tesla’s timeline.

I believe the balance of evidence favors the upside. The next twelve months will tell us whether this is the bottom of the non-linearity curve - or the beginning of the next parabolic phase.

In marketing, the adoption curve displayed above is a tool used to understand the stage of maturity of a product or a category. I, like many others, believe that EVs are currently sitting between Early Adopters and Early Majority - in the first half of the curve. This is similar to where iPhones and smartphones were around the year 2010, in my view. Tesla is using its pricing strategy to accelerate the mass adoption of EVs, which is referred to as “the chasm” in marketing theory. As Tesla is the market leader in this category, it is the company that stands the most to gain from this transition.

Research Desk, PolyMarkets Investment Strategies

Disclaimer: This market tip represents the author's personal research and analysis as of May 9, 2024. It does not constitute financial advice or an investment recommendation. Tesla is an inherently high-volatility, high-beta stock with material execution risk across FSD, competitive positioning, and macro sensitivity. Always conduct your own due diligence and invest only what you can afford to lose. Past performance is not indicative of future results.