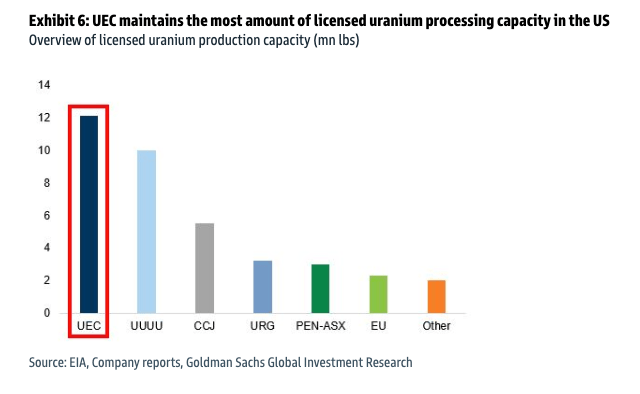

I want to describe this stock in the simplest way possible, because the investment case is actually that clean once you strip away the noise. The United States imports approximately 95% of the uranium it needs to run its nuclear power fleet. That fleet generates 20% of the country's electricity. The White House has issued four separate executive orders directing the country to quadruple domestic nuclear capacity by 2050 and rebuild a home fuel supply chain from scratch - including a directive for NRC to approve construction permits within 18 months, down from 30-42 months historically. And there is exactly one company - one - that has three permitted, ready-to-produce ISR hub operations on US soil with the largest licensed production capacity in the country.

That company is Uranium Energy Corp. And it's sitting at $6-$7 per share with zero debt, $271 million in cash and liquid assets, and 1.36 million pounds of physical uranium already in inventory valued at $96.6 million at book, with an additional 300,000 pounds contracted for delivery in December 2025 at $37.05 per pound. Most miners have to wait until they produce. UEC can pick up the phone today. In fact, it already has: Q2 FY2025 revenue came in at $49.8 million from selling 600,000 pounds at an average realized price of $82.92 per pound, generating $18.2 million in gross profit. This is not a pre-revenue story anymore.

The timing is instructive. As Sprott's Jacob White wrote in his June uranium report: "As other asset classes faltered, uranium held its ground, supported by its structural supply-demand story, inelastic demand and insulation from tariff-related disruptions." Spot uranium surged 9.99% in June alone to $78.56/lb - its best monthly performance of 2025 - while uranium mining equities climbed 18.19% and are up 68% from their April lows. BMO initiated coverage with an Outperform and $7.75 target on June 3rd, citing UEC's near-term production ramp from the recently restarted Irigaray Hub. The entry point at $6-$7 is in the technical "strong buy area" per the TA, and the fundamental case at current uranium spot pricing gives a conservative NAV of $11.50-$13. The asymmetry here is as wide as I've seen it.

Commodity investing is most interesting when demand is structurally non-negotiable and supply is structurally constrained. Uranium in 2025 is one of those rare cases where both conditions apply simultaneously - and neither resolves quickly. Sprott's June 2025 uranium report puts it plainly: "Physical uranium and uranium equities continue to outperform over longer periods... the strong five-year returns relative to broader commodity and equity benchmarks reinforce the metal's role as a differentiated and strategic asset class."

The demand picture is not cyclical. It is structural and accelerating. The World Nuclear Association counts over 70 reactors under construction across 17 countries, with roughly 100 more in advanced planning. China alone plans 150 new reactors by 2035 and recently forecasted it will nearly double its nuclear power capacity by 2040, positioning itself as the world's largest nuclear generator. Japan has restarted 12 reactors and is expanding further. France extended 32 of its 56 operational reactors. The Czech Republic just signed an $18 billion nuclear deal with South Korea for two new reactors. The UK committed an additional 14.2 billion pounds to its Sizewell C nuclear plant. Belgium's parliament dropped its twenty-year-old nuclear phaseout plans entirely. Even the World Bank - which had banned nuclear financing for decades - reversed course in June, opening the door to $117.5 billion in annual lending capacity for nuclear projects and partnering with the IAEA to extend the life of the existing global reactor fleet.

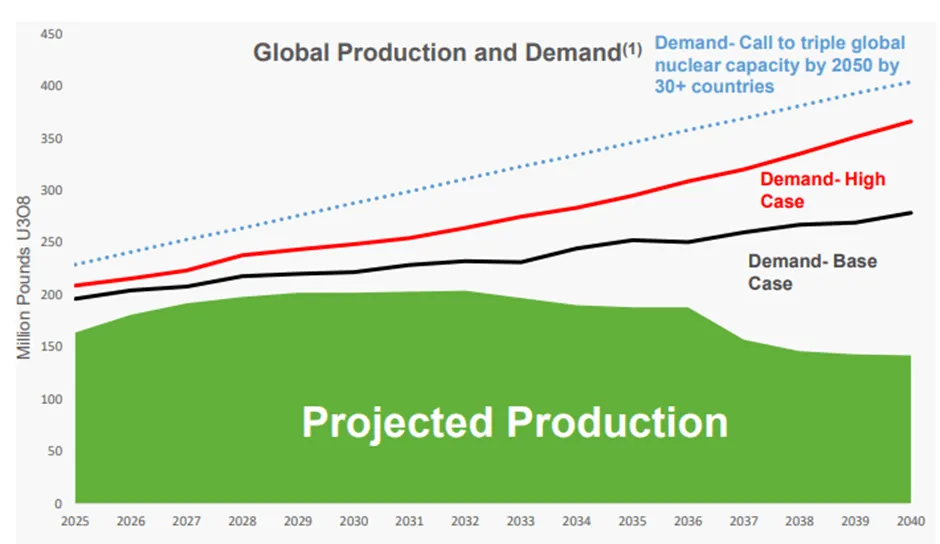

The supply chart tells the other half of the story. Global mine output was roughly 152 million pounds in 2022 against reactor demand of 170 million pounds. That 18 million pound gap was bridged by secondary sources - inventory drawdowns, recycled material, secondary market transactions. Those buffers are finite. UxC forecasts 2025 global mine production at 164 million pounds - still below reactor requirements. By 2040, analysts project a shortfall approaching 130 million pounds annually. Consider the scale of the mismatch: the Trump administration's executive order to quadruple US nuclear capacity alone would add roughly 150 million pounds of annual U3O8 demand - nearly doubling total current world mine production. That's before counting China, the UK, or the Czech Republic.

The term contracting market confirms that utilities sense the pressure. Yet they've been slow to act. Through mid-2025, utilities have signed only 27 million pounds in the term market - less than one-third of the replacement rate needed to maintain coverage. This delay reflects policy uncertainty (will the IRA nuclear credits survive?) and price volatility. But with term contracting lead times now fallen to just 2.6 years, utilities should be growing alarmed about future availability. Sprott describes this as "pent-up demand that must eventually return to the market" - and when it does, it will collide with a supply side that is structurally unable to respond quickly.

The critical point for UEC specifically is that a large chunk of this supply problem is geopolitical, not geological. Kazakhstan and Russia control ~40% of global supply. And the fragility of that supply chain is being tested in real time. In June, Niger announced it will fully nationalize the Somair uranium mine - one of the country's largest uranium assets - tightening state control over a critical link in the Western fuel cycle. Meanwhile, Cameco's Inkai joint venture in Kazakhstan was suspended for three weeks in January on a directive from partner Kazatomprom, with revised 2025 production cut to 8.3 million pounds from earlier targets. No deliveries from Inkai are expected until the second half of the year. Even BHP - the world's largest miner by market cap - reported an 18% year-over-year decline in uranium production at Olympic Dam, and confirmed that its planned copper expansion will add only marginal uranium growth of roughly 1%.

The US has made reducing dependence on that supply chain a national security priority. A Section 232 national security investigation into critical minerals, including uranium, is underway - the same investigation framework used to impose 50% duties on steel and aluminum. That's an explicit political tailwind for the only US company with the licensed capacity to actually do something about it.

It is worth dwelling on the policy environment because it has shifted more in the last six months than in the previous twenty years. This is not generic "government support" language - these are concrete legislative and executive actions with specific numerical targets that directly impact uranium demand.

The Big Beautiful Bill, passed on July 4, 2025, preserved the IRA production tax credit for nuclear energy while significantly scaling back incentives for wind, solar, hydrogen, and EVs. This clarity is consequential. Many utilities had paused long-term uranium procurement to assess whether IRA repeal efforts would impact credit availability. With the legislative outlook now settled, the path is clear for utilities to resume contracting with improved forward visibility.

The four nuclear-focused executive orders signed in May 2025 go further still. The first reforms the Nuclear Regulatory Commission: construction permits and operating licenses must be reviewed within 18 months (previously 30-42 months), NRC cost recovery will be capped (recent reactor designs had incurred $45-70 million in NRC fees alone), and licensing rules will be overhauled entirely. The second directs the reinvigoration of the nuclear industrial base: 5 GW of increased output from existing plants, construction of 10 large reactors by 2030, and a plan to expand US uranium conversion and enrichment capacity. The third deploys advanced nuclear for national security, including a requirement that a military base operate a nuclear reactor by 2028. The fourth creates a pilot program for three new test reactors.

The math on the NRC reform order alone is staggering. Quadrupling US reactor capacity would push annual uranium requirements from roughly 50 million pounds of U3O8 equivalent to nearly 200 million pounds. For context, total global mine production is forecasted at 164 million pounds for 2025. A single country's policy ambition would require more uranium than the entire world currently produces. Even if only half of this materializes, the supply deficit widens from "structural" to "structural and politically mandated."

The AI and data center demand layer compounds this. According to BloombergNEF, US data centers are projected to consume 8.6% of total electricity demand by 2035, up from 3.5% today. In response, there have been 16 US nuclear power announcements tied specifically to data centers and AI, totaling over 28 GW of capacity - nearly 30% of the US's current nuclear fleet. Amazon expanded its partnership with Talen Energy in June: Talen will supply up to 1,920 MW of clean power from its Susquehanna nuclear plant to AWS as part of a $20 billion investment. The Switch-Oklo partnership targets 12 GW of nuclear capacity phased through 2044. Microsoft, Google, Meta, and Oracle have collectively announced deals for 10.7 GW. These are not aspirational press releases - they are binding capacity agreements from companies with the capital to execute.

UEC is already positioning for this. In May 2025, UEC signed a memorandum of understanding with Radiant Industries to supply domestically sourced uranium for Radiant's Kaleidos portable nuclear microreactor, planned for mass production and testing at Idaho National Laboratory. This is the domestic supply chain the executive orders are designed to build - and UEC is the anchor supplier.

There are a dozen uranium stocks. Most are development-stage stories priced on hope and exploration maps. NexGen Energy has C$434.6 million in cash and a spectacular deposit at Rook I - but zero revenue, ongoing net losses (C$50.9 million in Q1 alone), and a production timeline of 2027-2028 at the earliest. Denison Mines targets first production at Phoenix ISR in 2028 pending regulatory approval. UEC is different in three specific ways that are structural, not promotional - and critically, already generating revenue.

UEC's hub-and-spoke model is the core of the physical thesis. ISR satellite wells feed into central processing plants - a structure that is both environmentally superior to conventional mining and operationally flexible. Wells can be turned on and off at relatively low cost as spot prices move. This is especially important in the current environment where Cameco - with 54.55% of Cigar Lake and 70% of McArthur River - is deliberately producing below capacity at 18 million pounds per mine against licensed capacity that could deliver significantly more. The industry is supply-disciplined. UEC's advantage is that it can ramp production into an already-tight market when the economics are optimal.

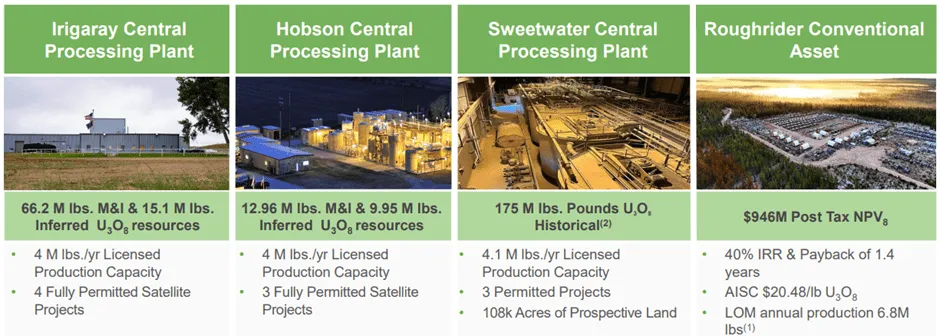

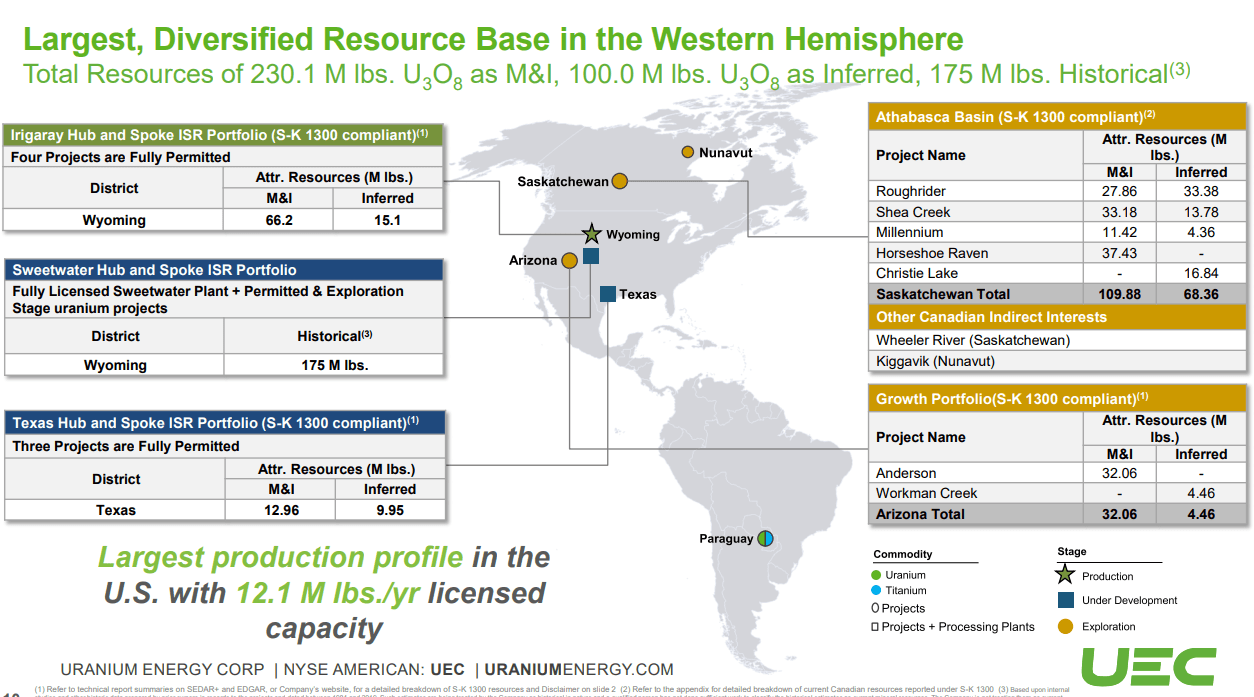

| Hub / Asset | Location | M&I Resources | Licensed Capacity | Status |

|---|---|---|---|---|

| Irigaray Hub & Spoke | Wyoming, USA | 66.2M lbs U₃O₈ | 4M lbs/yr | Production |

| Hobson / Burke Hollow | Texas, USA | 12.96M lbs U₃O₈ | 4M lbs/yr | Construction |

| Sweetwater Hub (ex-Rio Tinto) | Wyoming, USA | 175M lbs (Historical) | 4.1M lbs/yr | TRS Pending |

| Roughrider (Athabasca) | Saskatchewan, Canada | 27.86M lbs M&I | 6.8M lbs/yr (LOM) | Pre-Feasibility |

The Q3 FY2025 progress update confirms that each hub is tracking ahead of expectations. At Christensen Ranch, the first new mine-unit (Header House 10-7) has been commissioned as part of the phased ramp-up of Wyoming's Powder River Basin operations, with additional wellfields on track for production imminently. At Burke Hollow in South Texas, major equipment is installed at the satellite ion exchange plant and disposal well development is in progress. At Sweetwater - acquired from Rio Tinto, establishing UEC's third hub-and-spoke platform - a Technical Report Summary under the new S-K 1300 framework is due by end of fiscal 2025. Key personnel have been added across operations, geology, metallurgy, and supply chain management.

The Roughrider asset in Saskatchewan's Athabasca Basin deserves special mention. It sits in the same geological district as Cameco's McArthur River and NexGen's Arrow deposit. Metallurgical test work is significantly advanced - bulk solvent extraction and yellowcake precipitation have been completed, and a formal S-K 1300 Pre-Feasibility Study has been initiated. The post-tax NPV at $80/lb uranium is $946 million, with a 40% IRR and a 1.4-year payback period. It is not in UEC's base case production guidance, yet it's carried on the balance sheet as a development asset. When the long-term uranium contract market firms above $85/lb - which the policy environment and structural deficit increasingly demand - Roughrider's NPV becomes material and is likely to attract re-rating attention on its own.

The technical picture for UEC in early June 2025 is one of the more attractive setups I've seen on a uranium name. The stock spent much of Q1–Q2 2025 unwinding a tariff-driven overshoot to the downside - down roughly 38% from its January peak to the April trough. What we're looking at now is a recovery off that oversold base, with the chart structure setting up a meaningful re-entry zone.

The Fibonacci analysis maps the $6–$7 zone as the "Strong Buy Area" - the confluence of the 61.8% and 23.6% retracement levels, prior consolidation support, and the 200-day EMA. The $7.24–$9.24 range is the broader "Buy Area" where the stock would still offer asymmetric risk/reward. The Fibonacci extension target at 127.2% gives a price objective of $12.51 - sitting squarely within our $11–$13 target range. RSI is curling out of oversold territory on the weekly, a pattern that in prior cycles has preceded 40–80% moves in uranium equities.

BMO's June 3, 2025 Outperform initiation at $7.75 triggered an 11.6% single-day rally, demonstrating the latent demand for institutional-quality uranium exposure. The stock retraced that move - which is precisely the re-entry opportunity this tip is designed to capture.

The peer comparison is where UEC's positioning becomes most evident. Cameco - the $23.2 billion bellwether at 4.2x-5.8x P/B - reported Q1 consolidated adjusted EBITDA of C$353 million and adjusted net earnings of C$70 million. But Cameco's uranium segment earnings actually declined due to timing of sales at its Inkai joint venture in Kazakhstan, where Kazatomprom suspended operations for three weeks in January and revised the 2025 production target down to 8.3 million pounds. No Inkai deliveries are expected until the second half of 2025. Cameco's supply chain runs through Kazakhstan. UEC's runs through Wyoming and Texas.

NexGen Energy trades at ~4.7x P/B with a $3.18 billion market cap - on the strength of its Rook I deposit alone. But NexGen reported a net loss of C$50.9 million in Q1, holds C$434.6 million in cash that is being drawn down by C$28.1 million per quarter in exploration spending, and has zero production revenue. Denison Mines at $1.33 billion is in a similar position: targeting Phoenix ISR first production in 2027-2028, pending regulatory hearings scheduled for October and December. UEC, by contrast, has already generated $49.8 million in quarterly revenue from actual production and sales. On a simple peer re-rating to sector median (~4.5x P/B), UEC's stock is already ~50% higher. The more relevant framework, though, is NAV-based.

| Company | Geography | P/B Ratio | Licensed Capacity | Debt |

|---|---|---|---|---|

| UEC ▶ | USA (ISR) | ~3.0x | Zero | |

| UUUU (Energy Fuels) | USA | ~2.0x | Low | |

| Cameco (CCJ) | Canada / Kazakhstan | ~4.2x | Moderate | |

| NexGen (NXE) | Canada | ~4.7x | Low | |

| Kazatomprom | Kazakhstan | ~3.8x | Low |

The NAV model is where the real price target comes from. Using UEC's guided production ramp (8M lbs/yr at steady state), an all-in cash cost of $30/lb (management guided; consensus cash cost is $20–$25/lb), and uranium at $85/lb (term contracts are already at $80), the EBITDA calculation reaches approximately $400 million annually. At 12x EV/EBITDA - half the 22-27x multiple that Cameco and Centrus trade at - the implied enterprise value is $4.8 billion. Add $271 million in net liquidity and divide by ~444 million shares: implied per-share value of $11.50-$12.00. Under optimistic assumptions ($25/lb costs, 9-10M lbs production at $90+/lb spot - a scenario the policy and AI demand trajectory makes increasingly plausible), the fair value reaches $13+. Note that Q2's realized selling price of $82.92/lb already exceeds the base case assumption, validating the model's conservatism.

| Metric | Conservative | Base | Bull |

|---|---|---|---|

| Uranium spot (avg realized) | $65/lb | $80–$85/lb | $90–$100/lb |

| Production (steady state) | ~4M lbs/yr | ~8M lbs/yr | ~10M lbs/yr |

| All-in cash cost assumed (per lb) | $35/lb | $30/lb | $25/lb |

| Est. EBITDA at steady state | ~$120M | ~$400M | ~$650M+ |

| EV/EBITDA applied | 10× | 12× | 14–15× |

| Implied Price Target | ~$11 | ~$12 | ~$13+ |

Even in a conservative scenario with lower uranium prices and reduced production ramp, the implied value at approximately $11 per share represents a substantial gain from the $6–$7 entry zone - underscoring the asymmetric risk profile available at current prices. There is no scenario in this model where a patient, well-sized entry loses money at steady-state production; the question is only how much the thesis delivers and on what timeline.

Being honest about risks is the only way to size this position correctly. UEC is not a low-volatility income stock. It is high-torque commodity exposure with specific structural advantages. Here is how I think about the key risks and why the balance sheet is built to absorb most of them.

The following scenarios reflect the author’s personal analysis and are not investment recommendations. See our full disclaimer.

There's a version of every uranium story that gets told during a bull market, and it goes something like: "demand is rising, supply can't keep up, every producer goes up." That version is fine but it's not differentiated. What I find genuinely interesting about UEC is that the asymmetry works even before the cycle fully turns, because of the balance sheet - and the evidence for that is no longer theoretical.

Consider what the data actually shows when you layer the sources together. The Sprott mid-year report confirms the macro: uranium miners are up 68% from April lows, spot has surged to $78.56/lb, and five-year returns for uranium equities have meaningfully outpaced both the S&P 500 and broad commodities. But Sprott also flags a critical vulnerability: utilities have contracted for only 27 million pounds in 2025, less than one-third of the replacement rate, with lead times now compressed to 2.6 years. When that pent-up demand returns to the market - and the Big Beautiful Bill's preservation of nuclear tax credits just removed the last excuse for delay - it will collide with a supply side where BHP's Olympic Dam is declining 18% year-over-year, Kazatomprom is restricting Cameco's Inkai output through unilateral suspensions, and Niger is nationalizing uranium assets.

Against that backdrop, UEC's Q3 FY2025 quarterly report confirms that the company is not waiting for the cycle to turn. Christensen Ranch's first mine-unit is online. Uranium is being processed, dried, drummed, and shipped to ConverDyn. Burke Hollow construction is advancing. The Sweetwater platform acquired from Rio Tinto adds 4.1 million lbs/yr of licensed capacity. The Radiant Industries MOU positions UEC in the microreactor supply chain the executive orders are designed to build. Q2 revenue of $49.8 million at $82.92/lb average proves the business model works at current prices - before the policy demand tsunami even begins to materialize.

The peer context makes the valuation case. Cameco trades at $23.2 billion with supply chain exposure to Kazakhstan. NexGen trades at $3.18 billion with zero revenue and production years away. UEC trades at $2.36 billion with the largest US licensed capacity, actual revenue generation, zero debt, 1.36 million pounds of sellable inventory, and explicit political support from both the White House and Congress. The $6-$7 entry is technical and fundamental in equal measure. The target of $11-$13 is derived from a peer-comp NAV model that is, if anything, conservative given the multiples the market already assigns to peers with longer timelines and greater geopolitical risk.

Disclaimer: This market tip represents the author's personal research and opinion as of June 12, 2025. It does not constitute financial advice. UEC is an early-production stage uranium company; uranium prices are inherently volatile and sentiment-driven. Always conduct your own due diligence and size positions according to your individual risk tolerance.